FOMC Preview

No policy changes or surprises are expected with today’s announcement (19:00 GMT) and Chair Powell’s press conference 30 minutes later. It will be interesting to see if, as expected, the voting is unanimous this time round. The FOMC members have expressed significant differences of opinion during 2019 as three rate cuts were implemented. The apparent paradox of low unemployment and low inflation, the new “norm”.

The two-digit unemployment rate (U-3) in November edged down to 3.53% from 3.56% in October, and a 3.52% cycle-low in September, all below the 3.58% prior cycle-low in April and a 4.00% rate at the beginning of the year. Current readings remain much lower than the 4.2% long-run unemployment rate projection noted in the September SEP, it is expected that this estimate will be trimmed today.

Headline CPI rose 0.4% in October while the core index rose by 0.2%, for respective y/y gains of 1.8% and 2.3%, versus September figures of 1.7% and 2.4%. Today the November headline is expected to fall again to 0.2% and the core remains flat at 0.2% too. The Fed’s favoured inflation gauge, the PCE chain price measure, rose 1.3% y/y in October and expectations are for an uptick to 1.4% in November. The core PCE chain price measure rose 1.6% y/y in November, versus 1.7% in September, and expectations are for the pace to hold at 1.6% in November. The FOMC’s latest median estimates for 2019 inflation are 1.5% for the headline and 1.8% for the core.

Hence, the focus will be on the Fed’s new quarterly forecasts, with expectations raised and likely to be mostly bullish results with a bump up in the median growth projection and a drop in the median dot to reflect a steady stance through 2020. However, the individual dots are likely to show both, forecasts for cuts and hikes. Chair Powell is expected to reiterate the US economy and policy are in a “good place,” (a phrase he has used a number of times lately) and could sound a little more upbeat after the strong jobs report. But, he will continue to warn of downside risks. The FOMC isn’t likely to announce any new measures on reserve management operations (QE?) or a repo facility. All steady into 2020 and beyond.

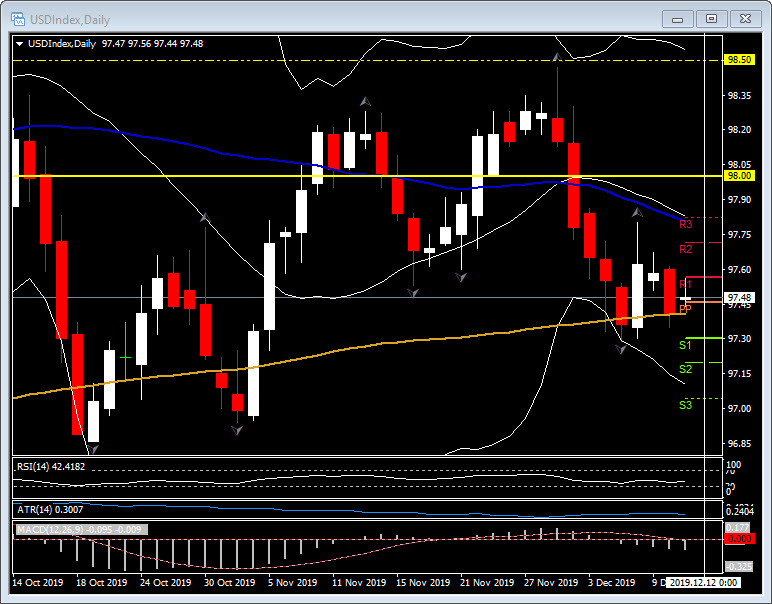

USDIndex remains biased to the down side but has support around 97.40 and the 200-day moving average. A breach of this key support zone brings in 97.00 and the October low of 96.85. A break over 97.80 (the confluence of the 20 and 50-day moving averages) and 98.00 would be required before a re-test of the recent high at 98.50 could be considered.

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.