2020 – Central Banks On Hold

ECB signals steady hand for prolonged period. Lagarde stressed in the introductory statement that a highly accommodative policy is still needed and that the ECB remains ready to adjust all its instruments, but at the same time, she also noted signs of improvement in data, which point to a stabilisation in growth. The next projections lifted the forecast for this year to 1.2% from 1.1%, but lowered the forecast for next year to 1.1%, while the 2020 projection was left steady at 1.4%. The risks remain tilted to the downside, but have become somewhat less pronounced. So pretty much confirming the view that in the central scenario the ECB will remain on hold through next year, which is also what Fed and SNB signalled. So markets can’t hope for further stimulus in the baseline scenario, but at least any type of tightening clearly is still a very far way off, which should help to prevent taper tantrums if there is a U.S.-China trade deal and the Brexit deal goes through. Inflation forecasts still show an average 1.2% this year, while the forecast for next year was lifted slightly to 1.1% from 1.0% and the forecast for next year cut back to 1.4%. With the 2022 forecast coming in at 1.6%, even that would still be slightly below the inflation target, which currently is close to, but below 2%.

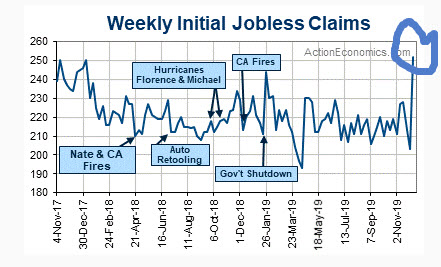

US data today again continued its volatile route, swinging back to the negative following the bullish jobs picture on Friday and the weak PMI’s last week. US initial jobless claims surged 49k to 252K in the week ended December 7 after dropping 10k to 203k in the last week of November. The pop higher leaves claims at a two year high, but the sharp increase was likely driven by seasonal volatility around the Thanksgiving holiday. The 4-week moving average climbed to 224.0k versus 217.75k. Continuing claims fell -31k to 1,667k in the November 30 week following the 56k jump to 1,698k previously (revised from 1,693k). Claims have shown their typical holiday gyrations over the last several weeks, and will remain volatile through January. Another disappointment was the PPI data.

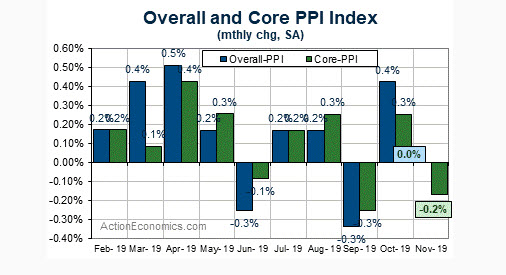

US November PPI was flat, while the core rate fell -0.2%. There were no revisions to the respective October gains of 0.4% and 0.3%. The 12-month headline rate was steady at the 1.1% y/y from October, the ex-food and energy rate slowed to 1.3% y/y compared to 1.6% y/y previously. Goods prices were up after rebounding 0.7% previously. That included a 1.1% increase in food costs versus the prior 1.3% rise. Energy prices rose 0.6% from 2.8% previously. Services costs dropped -0.3% from 0.3% in October. The data is weaker than expected.

The Dollar moved lower after the cold PPI readings, and much higher than expected jobless claims print. EURUSD headed to fresh one-month highs of 1.1150 from 1.1135, as USDJPY fell to four-session lows of 108.56 from over 108.60.

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.