EURUSD, H1 / Weekly

Germany’s economy stagnated in Q4 last year, in line with a number of forecasts and a tad below consensus expectations, which had predicted a slight expansion of 0.1% q/q. Compared to negative quarterly prints in France and Italy, Germany is already the outperformer among the three big Eurozone countries and Q3 numbers for Germany were revised up to 0.2% from 0.1% reported initially. This left the working day adjusted annual rate 0.4% y/y a tad higher than anticipated, but down from 1.1% y/y in Q3. There is no full breakdown yet, but the stats office reported that private as well as public consumption slowed in the last quarter of 2019, while investment was mixed with construction investment, expanding again. Exports contracted, while imports picked up according to first estimate. Looking ahead, exports are likely to continue to suffer and orders numbers are predicting another weak quarter for manufacturing, which leaves the risk that the labour market will start to suffer. The balance of risks clearly is tilted to the downside not just for Germany’s economy.

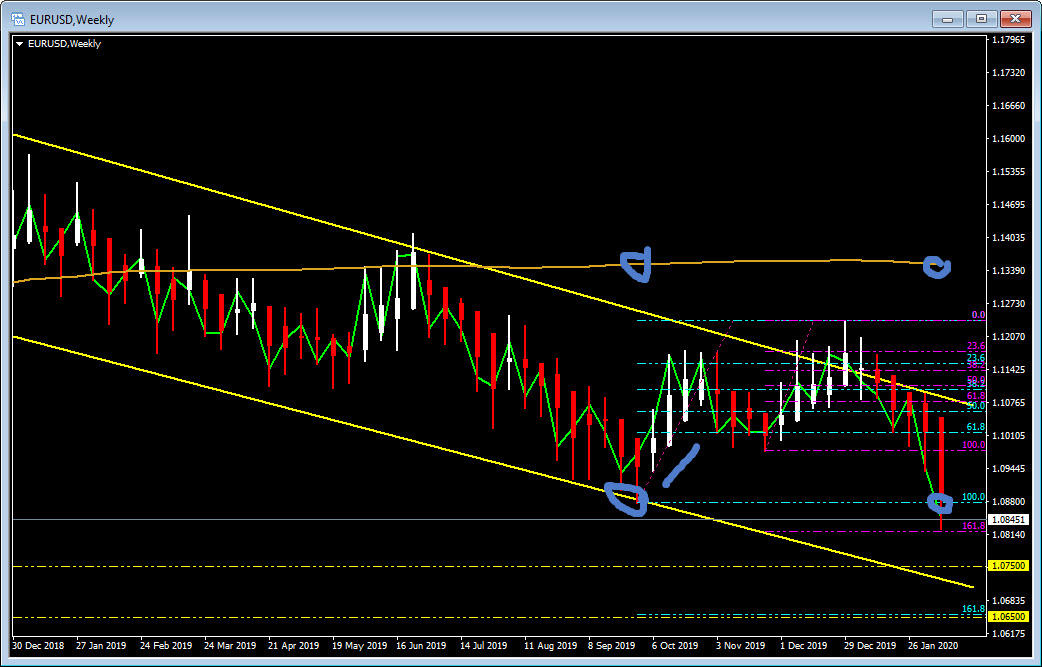

The Euro posted fresh lows against the Dollar and other currencies, while both the safe haven Yen and Swiss franc lost yesterday’s bid as the daily increment of new coronavirus cases in China fell back alongside narratives that are downplaying yesterday’s jump in total reported cases in Hubei province as being just a reclassification. EURUSD posted a fresh 34-month low at 1.08265, and is set for its biggest two-week loss since July 2019. Today, the German GDP helped lift it to 1.0840 with the broader GDP data for the wider Eurozone yet to come. EURJPY printed a four-month low, at 118.86, and EURCHF a near-five-year-low, at 1.0609. EURGBP yesterday saw a two-month low below at 0.8295.

Elsewhere, USDJPY settled in the upper 109.00s, above the four-day low seen yesterday at 109.61. Cable consolidated gains seen yesterday, holding just shy of the nine-day high at 1.3069.

The EURUSD low earlier tested the S2 and 161.8 Fibonacci extension low of the December rally at 1.0820, below there is the daily lower channel at 1.0750. In the the longer term the 161.8 Fibonacci extension level from the Q419 rally is at 1.0650 and then the psychological 1.0500. The Q419, against the trend, re-trace rally came from this over extension from the 200-day moving average which is where we are now, so some retrace to possibly the 1.1050-75 zone could be expected.

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.