European stock markets have moved broadly higher overlooking the February composite PMI readings for the Eurozone and the UK which looked robust. However, the first signs of supply chain disruptions were already evident in February even in Europe. Whether demand will be impacted short term, or more lastingly dented, a supply crisis could actually drive up prices, rather than depress them. Eurozone and German retail sales also recovered in January, while December numbers were revised higher.

Hopes that the ECB and the BoE will follow the Fed’s 50 bp emergency rate cut yesterday are keeping bonds underpinned despite the economic data outcomes, although stocks are struggling as the Fed’s surprise cut also sparked concerns that the economic situation is worse than feared. US futures are posting gains in the region of 1.9%-2.1%, although that seems to be less of a reaction to the Fed’s rate cut, and more due to the Super Tuesday election results in the US. Market narratives have ascribed the rally in overnight US equity futures to the success of former vice president Joe Biden in the Democratic Party’s “Super Tuesday” primary elections, which has made him the odds-on favourite to be the Democrats nomination for president, overtaking Bernie Saunders, who is evidently deemed to be less market friendly than the moderate Biden.

The ECB meeting next week will clearly see intense discussions, although as of yesterday it seemed that officials want to focus on alternative measures, including another targeted loan program to address, what will likely turn into a supply crisis.

Hence as stock markets rallied and data releases were largely overlooked, we have seen GER30 struggling to break through the 23.6% Fibonacci resistance level from February’s plummet.

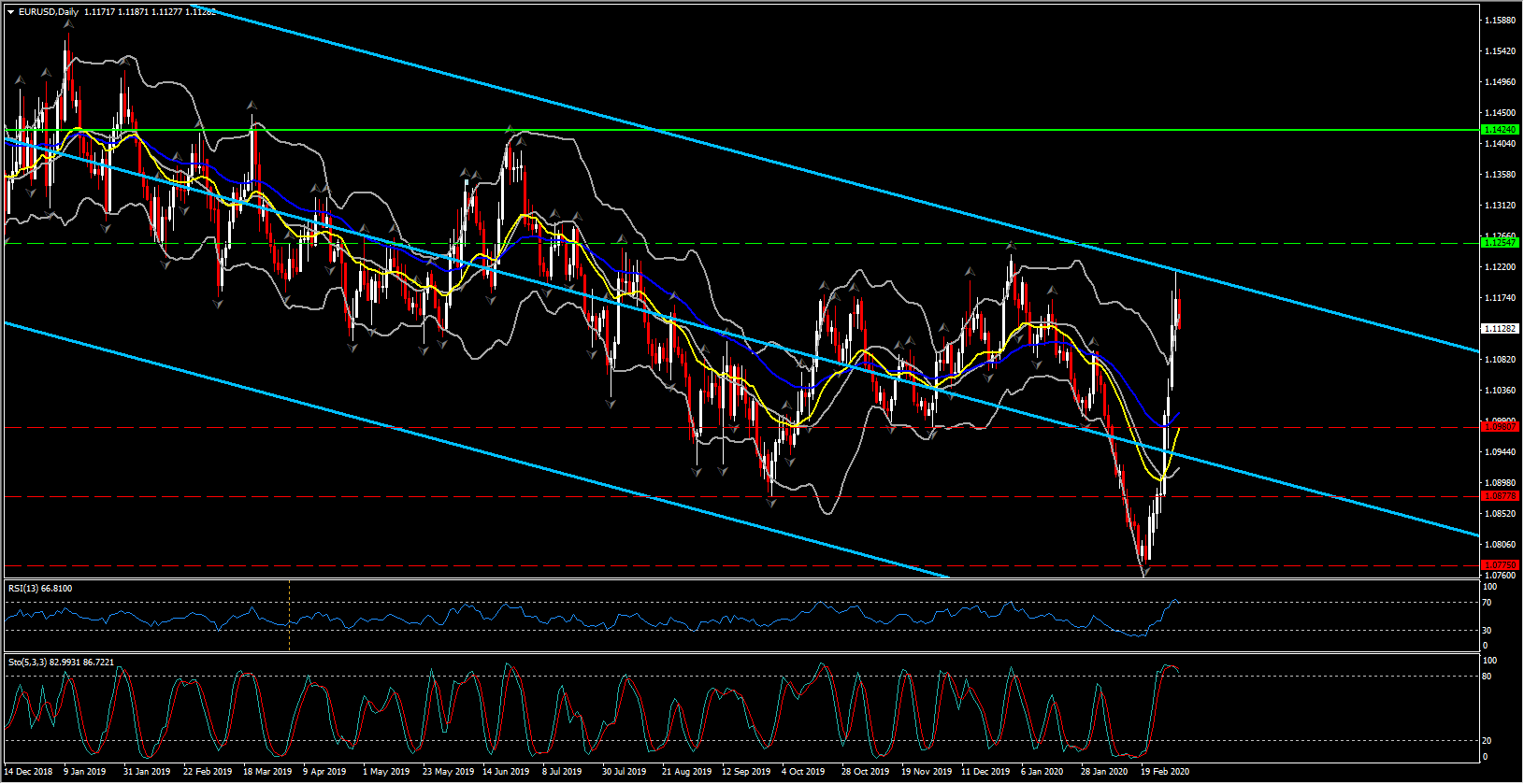

Meanwhile, EURUSD fell back to the 1.1150 area after printing a 2-month peak at 1.1213. The Dollar, after sliding for much of the last 2 weeks, a primary beneficiary of which has been the Euro, looks to have found a toehold after dipping to fresh lows in the immediate wake of the Fed’s 50 bp emergency rate cut yesterday. Such a move had been fully discounted in the Fed funds futures market, but at the March-18th FOMC rather than yesterday’s between-meetings move.

The narrow trade-weighted USDIndex posted a post-Fed two-month low at 96.98 before lifting to around 97.35 in what is shaping up to be the first up-day the dollar index has seen since February 20th. The 10-year US T-note yield advantage over the 10-year Bund has dropped from around 200 bp to around 160 bp in little more than two weeks. This has driven the shift higher in EURUSD, which had in February been trading at 34-month lows.

EURUSD gains are not expected to be a one-way street. Recent gains are being viewed as a rotation higher rather than a trend following move given the negative yields and apparent exposure to the coronavirus in the Eurozone (Italy ranking as the number 2 country with the most reported cases of COVID-19 outside of China), coming at a time when German growth sputtering as demand for its exports dives.

As the same time, the US Treasury market remains a top safe haven for global capital (being liquid, safe and positively yielding). Markets will continue to monitor the relative impact of the coronavirus, and efforts to contain it, between the US and Eurozone.

From the technical perspective meanwhile, we can identify a few prime signs of an exhaustion since the 20 February incline. Momentum indicators near term and medium term provide similar signs of a potential pullback. In the daily chart, the RSI has turned below 40 and Stochastics holds above 80, however it has formed a rounding top as it slopes lower. On the contrary, MACD is mixed with lines above neutral but signal line configurating into the negative area.

These signs cannot yet imply a switch of the positive outlook for EURUSD, unless the asset hit the 50-day EMA at the round 1.1000 level .

Click here to access the HotForex Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.