Commodity currencies have seen moderate losses against the Dollar and other main currencies against a backdrop of sputtering low-volume stock market trading and a turn lower in Oil prices.

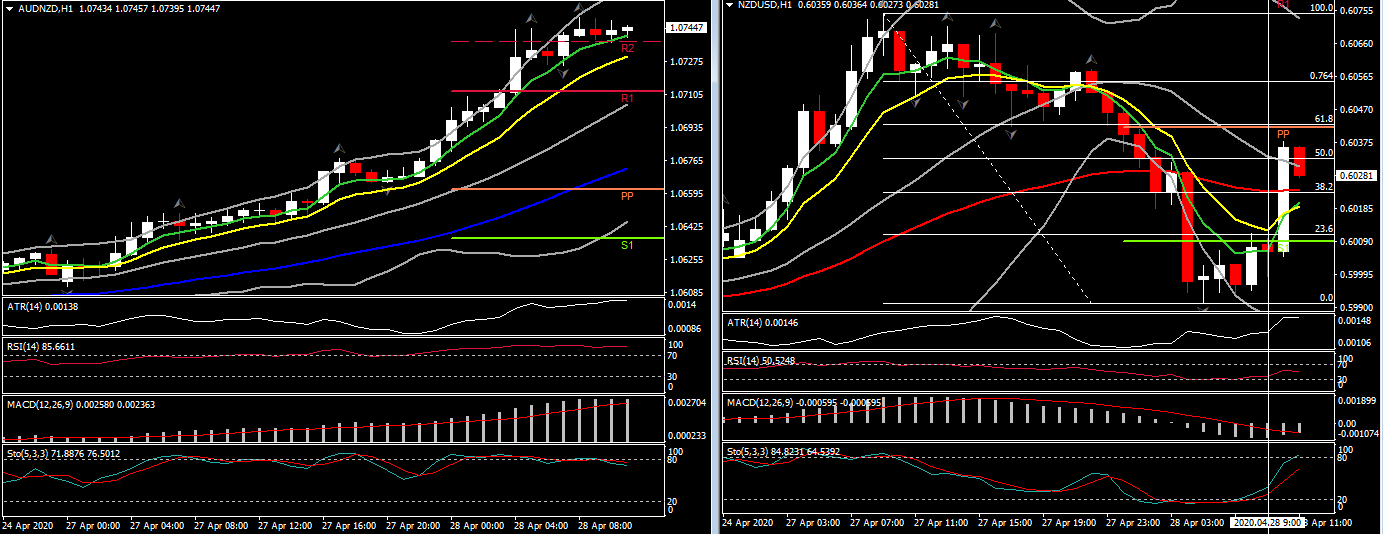

The NZD led the way lower for the commodity group after a research note from Westpac hit a bearish chord by forecasting that the RBNZ will take the cash rate to -0.5% in November this year. RBNZ Governor Orr last week said he would not rule out negative rates, and that he was “open minded” on direct monetisation of government debt. NZDUSD dropped over 0.6% in printing a 4-day low at 0.5992.

With the RBA having recently been ruling out going negative with interest rates, AUDNZD rallied to a fresh 6-month high, at 1.0754. The antipodean cross has now risen by nearly 7% since mid March. Note that weekly consumer confidence out of Australia, not normally a market shaker, posted a fourth straight week of improvement from the record low that was seen in March, although the headline is still overall pessimistic at a sub-100 reading of 85.0.

Among the Dollar majors there has been little movement. EURUSD has seen little more than a 20 pip range in the lower 108.00s, holding above yesterday´s 108.08 low. USDJPY has seen a sub-20 pip range in the lower 107.00s, holding above yesterday’s 13-day low at 106.99. The BoJ boosted its JGB purchases as scheduled operation, but to little impact on the Yen.

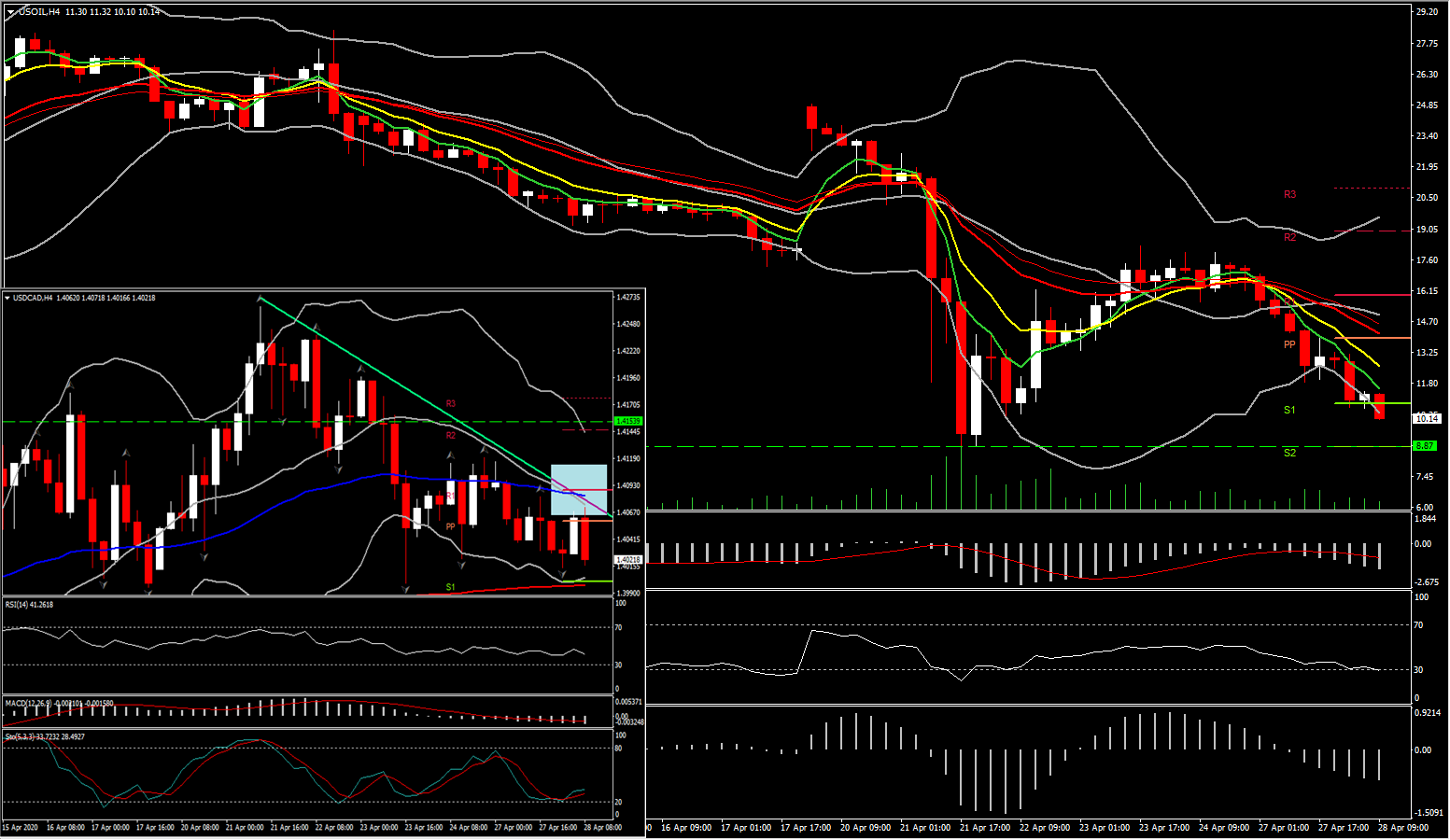

As for Oil, the hefty declines in oil prices have weighed on the Canadian Dollar, along with other oil-correlating currencies, lifting USDCAD out of a 5-day low at 1.4017 to levels above 1.4070. June WTI futures were showing a drop of 16%, at $10.66, as of early in the London session. This follows news that the United States Oil Fund LP, the largest US oil ETF, said it would sell all its front-month crude contracts to avoid further losses amid collapsing prices.

Goldman Sachs research concluded last week that global oil storage capacity would be reached within three or four weeks, which, once realized, would force a 20% cut in production. Such a cut would be tantamount to 18-20 mln barrels per day, which would be on top of the 9.7 mln barrels per day cut by OPEC++ nations, which will take effect on May 1st. GS estimated it would take between four and eight weeks for crude to base, noting that the production cuts won’t be easy to reverse, which in turn would risk there being a supply deficit.

USDCAD eased from overnight highs of 1.4075, basing at 1.4014 in London morning trade. Risk-on conditions have weighed on the USD generally, though another 16% drop in WTI crude could limit USDCAD’s downside potential. On a positive note, the Western Canadian Select grade of crude is reportedly trading over $6/bbl, a vast improvement from the negative numbers seen for a couple of days last week. In the big picture, oil prices will continue to drive USDCAD direction.

Click here to access the HotForex Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.