Energy

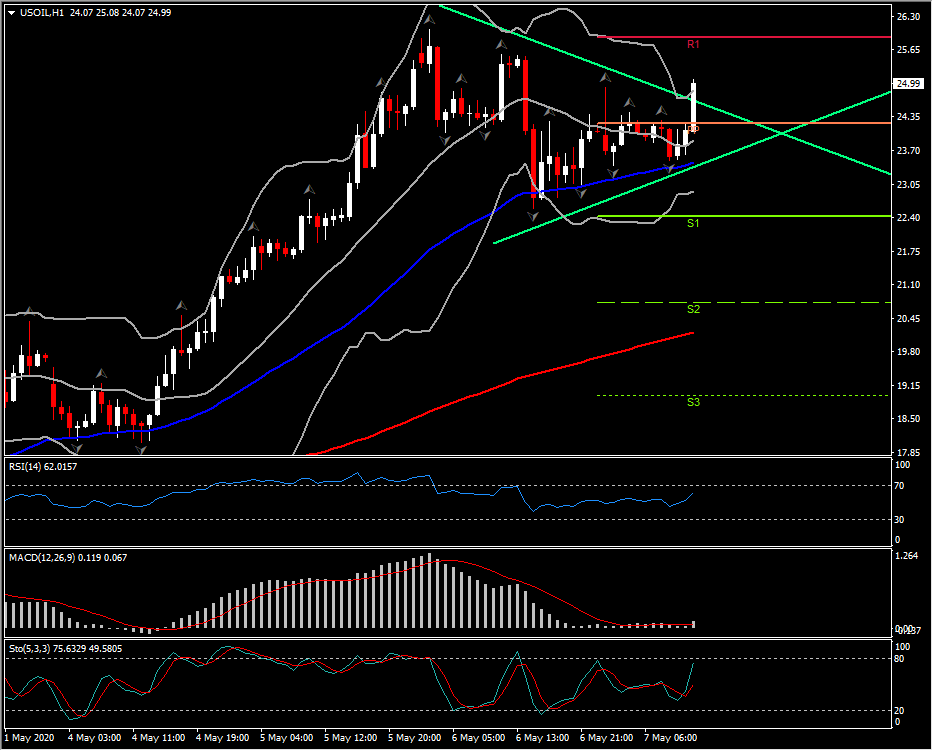

Oil Action: USOIL has steadied on either side of the $23.00 level, though remains down nearly 6% on the day, after printing 3-week highs over $26 overnight. The weekly EIA inventory report yesterday revealed a much smaller than expected rise in crude stocks, but also a larger than expected build in distillate supplies, which offset the mildly bullish crude number. The EIA reported that US production slipped to 11.9 mln bpd in the latest reporting week from 12.1 mln bpd the previous week. March production levels were near 13.1 mln bpd.

Meanwhile, earlier today, the unexpectedly good trade report out of China, which reported an 8.2% y/y rise in exports, contrary to the median forecast for a 14.1% contraction, catalysed a risk appetite, which also lifted the commodities and commodity currencies. Currently the crude prices remain up by over 230% from the low seen near $10 on April 28th, though prices still remain down by over 74% from the highs seen in January, as the oil market is not out of the woods yet, as production cuts have so far been insufficient to offset the huge virus related crash in demand.

Hence, on the products side, EIA data shows that refinery utilisation continues to improve, while from trade side, China’s data shows that economies reopening globally could support the Oil price in the near term .

That said, going forward, focus is on economies that are reopening from virus-containing lockdowns, and how successful, extensive and durable this proves to be. This should rekindle demand for oil and other commodities, which should in turn put in an underpinning for Canada’s currency.

Metals

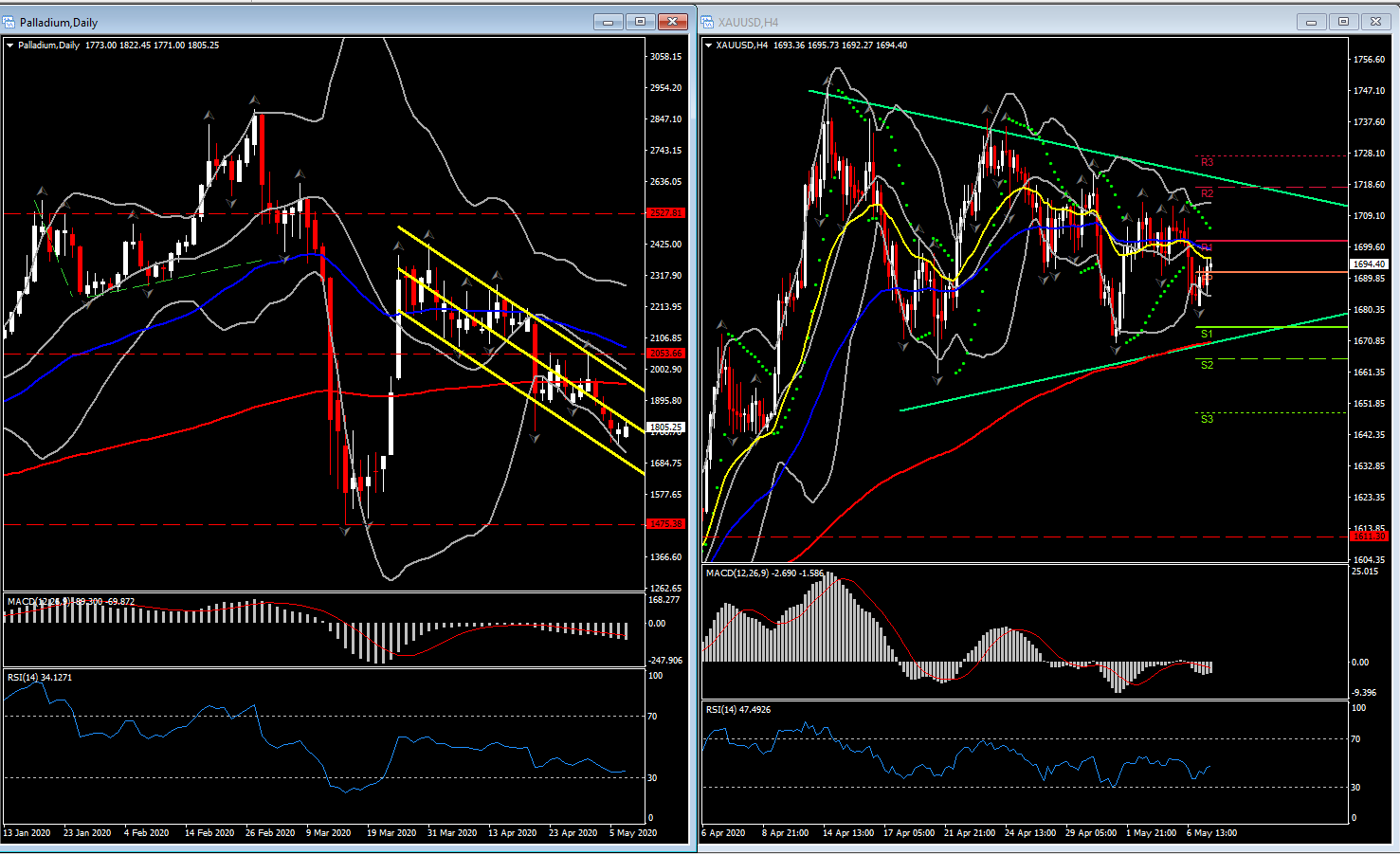

Metals meanwhile are trading mixed with gold, copper, silver and platinum trading back from their highs, but at the same time holding well above the year’s plunge, suggesting that there are some signs of a stabilisation in sentiment. Palladium is the exception to this, since it has been trading in a negative territory since the end of March. Chinese data helped in the short term timeframe to partially dispel worries of a negative impact on metals demand via exports, although the detailed data are still unavailable. Nevertheless, the mining disruptions remain and should remain in the near future largely responsible for the tight market in metals since for the time being there is demand only from smelters.

Click here to access the HotForex Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.