EURUSD, H1

Eurozone Q1 GDP was revised up to -3.6% q/q from the -3.8% q/q reported initially. A modest upward revision that still left the annual rate at -3.1% y/y and doesn’t change the fact that with Q2 GDP certainly going to be worse, the Eurozone is effectively in recession now. Lockdowns, which started to come into effect in the latter part of the first quarter across many European countries, wiped out any improvement that was seen at the start of the year. The breakdown, which was released for the first time, showed private consumption falling -4.7% q/q, investment down -4.3% q/q and government spending down -0.4% q/q. Exports fell -4.2% q/q, imports -3.6% q/q, meanwhile net exports detracted around 0.4% points from the quarterly growth rate. The overall GDP number was actually propped up somewhat by stock building, so the real impact of lockdowns on activity was actually slightly worse than official GDP numbers suggest. Again Q2 is likely to be even worse and while survey findings suggest that economic activity bottomed in April, the May numbers suggest a slowdown in the pace of contraction, but not a real recovery.

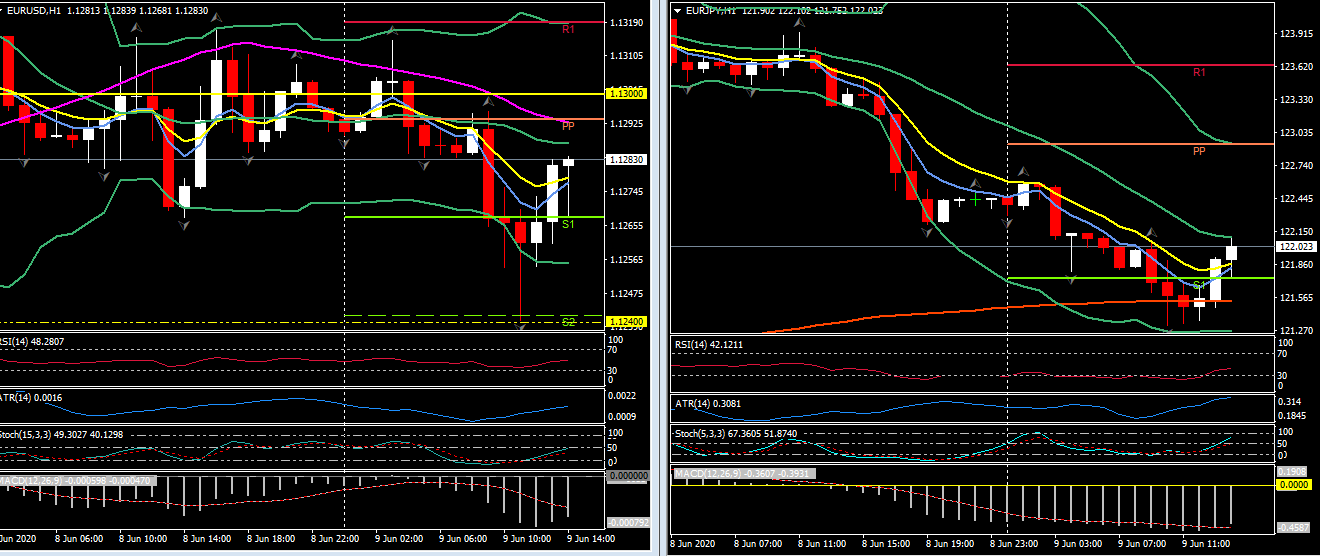

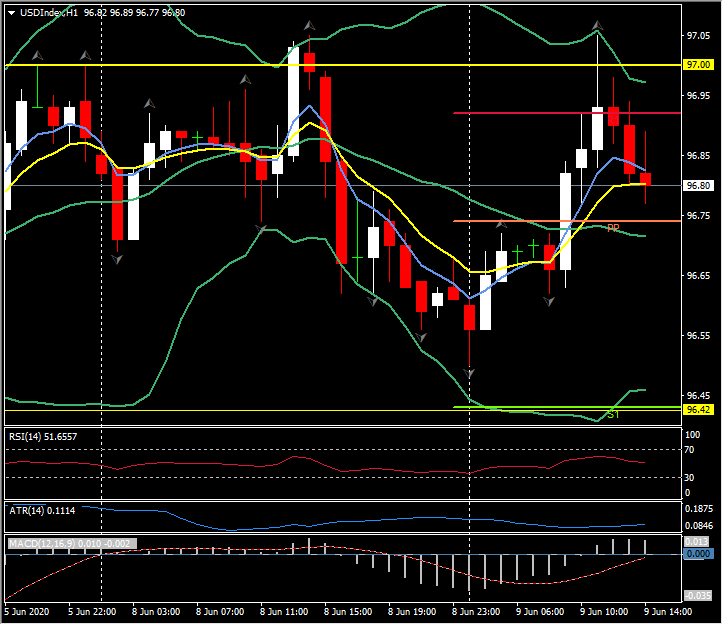

EURUSD has drifted moderately lower, weighed on by a general softening in the Dollar and a fairly steep, 0.6%-plus, decline in EURJPY. Both the Dollar and Yen have been picking up safe haven demand as stock markets correct across European bourses, with US equity index futures following suit. Lofty prices and a 24% dive in German April exports catalysed the sentiment shift. The narrow trade-weighted USDIndex lifted to a high of 97.06, which is 1 pip shy of yesterday’s high, while EURUSD concomitantly ebbed to a five-day low at 1.1242.

The Fed is widely expected to leave policy unchanged at its meeting this week (announcing tomorrow – Wednesday June 10 – at 18:00, with the Press Conference 30 minutes later). Consensus opinion holds that further rate cuts into negative territory are off the table for now, given substantial internal and public opposition. This could help the Dollar find its legs, especially if the stock market correction persists. The bigger focus remains on economic re-openings on both sides of the Atlantic, and globally. There are risks ahead, which have the potential to return the Dollar’s role as a safe haven. One is the simple fact that economies aren’t likely to fully recover under virus-containing social distancing rules together with the threat of there being renewed lockdowns, which means that asset markets, many of which are trading back at levels seen before the pandemic took a grip, could now be ripe for setbacks. Also, there is a risk that bankruptcies will soar once government business and pay support schemes fall away in the coming months, and risks associated from US (and wider West)-China tensions.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.