")

Investors breathed a sigh of relief after Wall Street bounced on Friday, despite it closing off the day’s highs and recouping only about one-third of Thursday’s steep losses. The USA30 rallied 1.9%, with the USA500 up 1.3%, while the USA100 climbed another 1%, and continues to pace the upside in June, up 1.0%.

With FOMO (fear of missing out) still in play, Thursday’s plunge presented a bullish sign. Treasuries, meanwhile, eroded on the bounce in risk appetite. The long end led the slide in a bear steepener with the curve widening back to 50 bps from 46.6 bps Thursday, though it was as wide as 64.7 bps last Monday.

However today, the US stocks started the week broadly lower, but off their worst levels. Worries over a second wave of virus after Beijing reported a new spike of cases, originating from a wholesale food market, forcing the city to enact lockdown measures.The massive amount of liquidity in the system, and talk of another government package, could provide a ground for US futures, however for the timing being the fear of a second wave of coronavirus infections remains front and centre. Beijing reported dozens of new cases in recent days, all stemming from a wholesale food market. In response, the city has gone into lockdown. Also, the r-rate has been creeping back above 1, indicating an exponential spread, in several states in the US and some areas in Europe.

Hence, safe haven positioning in global markets has caused a sharp decline in stocks on the bad news from the virus front. However the declines for US futures started after the rather pessimistic outlook from the Fed, which was the spark to catalyse a correction in the asset markets. There is a lot of criticism around the Fed’s stance, however the Fed has not done anything wrong other than to point out what we already knew – that the US/global economy is in a bad place.

The Fed has strongly used its tools and will continue to do whatever it takes to promote maximum employment and price stability goals. He noted the improvement in the May jobs report in part by some returning to work and with support from the government’s PPP. The Fed cautioned that the unemployment rate remains historically high, however, and repeated in the last statement that a full recovery is not likely until people feel safe in getting back to their daily lives. Hence with or without optimistic signs from the US labour /housing/ auto markets, it is unlikely to see a fast recovery.

The Fed Committee continued to discuss the different tools it might use including yield curve control and explicit forward guidance, but they are still open for discussion, as the Fed wants to learn more about the economy’s path before really deciding. So what else could be done if not negative rates? What could the yield control offer? What could the equity markets anticipate?

Therefore, the factors causing US stocks to decline by more than 9% in June are fear of 2nd wave as a vaccine and/or effective treatment remain elusive (Alaska, Arizona, Arkansas, California, Florida, North Carolina, Oklahoma and South Carolina all had record numbers of new cases in the past three days.), mixed US economic data and, as mentioned, the Fed’s unflattering economic outlook.

Nonetheless, there is also the Overbought scenario, meaning that there is always the possibility that Stocks have drifted so much simply because they have gone up too much, causing profit -taking actions. Hence it could be a combo of things.

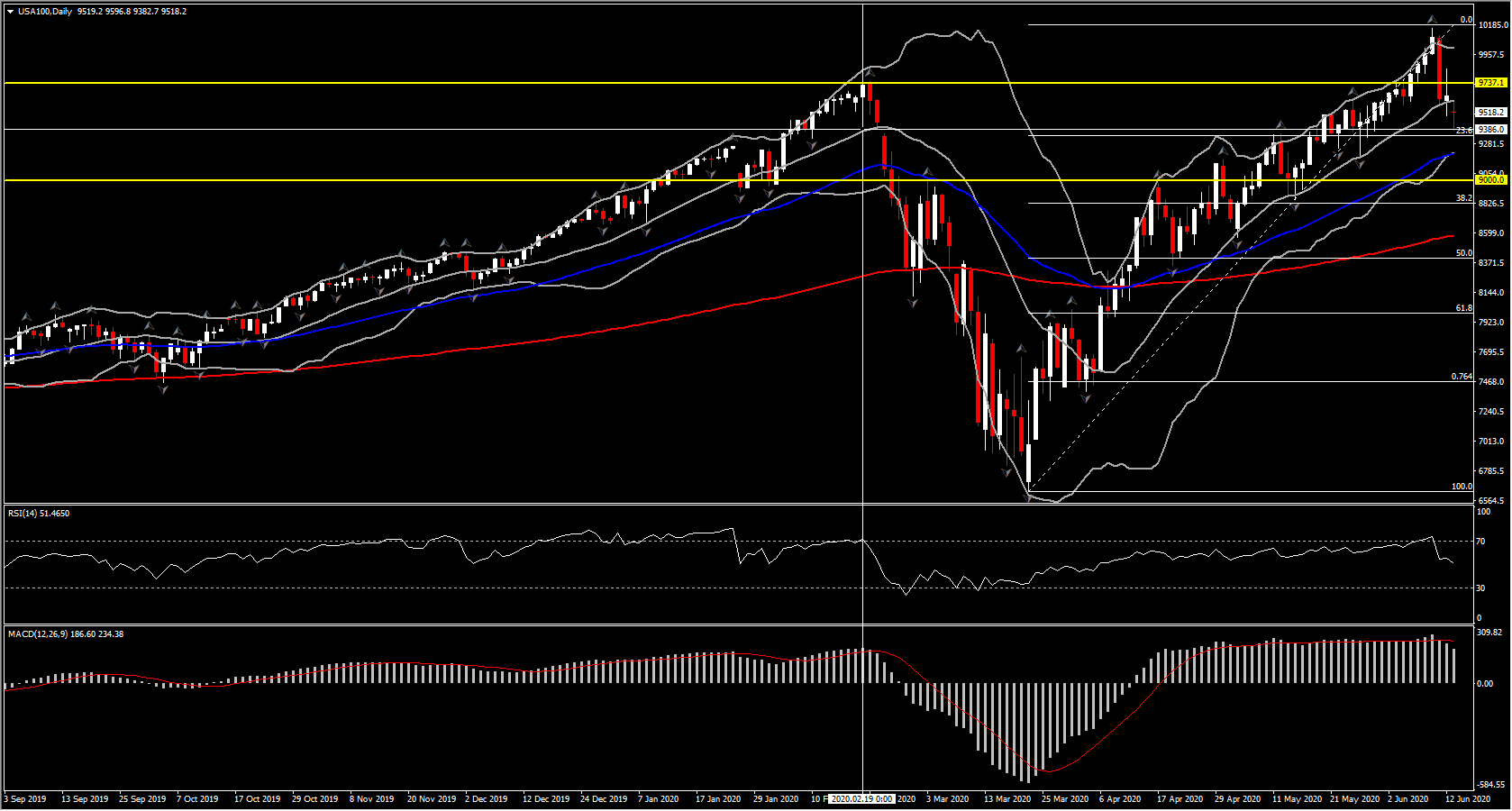

The USA100, despite the reversal of nearly 23.6% of the gains seen since mid March, sustains the picture of a technical correction in an OB rally. The asset holds a move above the 9,000 barrier, and the 50- and 200-day EMA since April 8. The breakout on Thursday of the previous record high at 9,740 left an extremely strong Support level, which questions now whether the decline could switch the overall positive outlook for USA100. That brought into our attention the next significant band at 9,100 (50-day EMA) and the 9,000 (round number and of Resistance March and April). Daily Momentum indicators have been impacted slightly by the selling pressure, with RSI rejecting the 75 high and turning at neutral zone while MACD lines fell below signal line, sustaining through a move well above 0. Hence only a break of the Support area mentioned above, along with a turn of the daily indicators below neutral zone could suggest that the market is turning from a correction into a potential reversal move of the 3-month rally.

From the fundamental perspective, attention will be turned now to Fed Chair Powell, who will go before Congress (Tuesday, Wednesday) to deliver his semi-annual Monetary Policy Report. The prepared testimony largely reflected last week’s FOMC policy statement, noting how the pandemic and subsequent safety measures taken have caused “tremendous human and economic hardship,” and how the Fed remains committed to using its full range of tools to support the economy.

However, the Q&A offers the chance for him to nuance his tone after a relatively gloomy outlook in the FOMC’s projections, and especially the 0% to 0.25% rate stance through 2022 and whether he will suggest more of a “V” recovery is possible.

Click here to access the HotForex Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.