EU summit goes into fourth day amid signs of a compromise on the recovery fund. That this wouldn’t be an easy summit was clear, but there had been hoped that the week would start with a compromise on the table. Instead officials are set to resume official discussions at 14:00 GMT today.

The split between loans and grants in the EUR 750 bln recovery fund has been the main sticking point with the Austria and Netherlands turning out to be the real hardliners arguing against too generous no-strings, cash handouts. There are now reports though that a compromise has been found, although the details are still hazy, with some reporting a 450/300 split between grants and loans, others that the hardliners will accept just EUR 390 bln in grants, with the rest available as loans, likely with some sort of reporting requirement.

The initial proposal had focused on EUR 500 bln of grants, which would avoid the stigma that was associated with the bailout funds handed out in the aftermath of the financial crisis and required budget oversight through the European Commission. Whatever the final agreement is the portion of grants will be lower than in the original draft, which could leave some investors disappointed and give Eurosceptic something to argue with. Ultimately though, any sizeable agreement that include grants should be good for markets – at least in the short term. In the medium to long term, it continues to kick Italy’s problems in particular down the line, without providing an incentive for real reform.

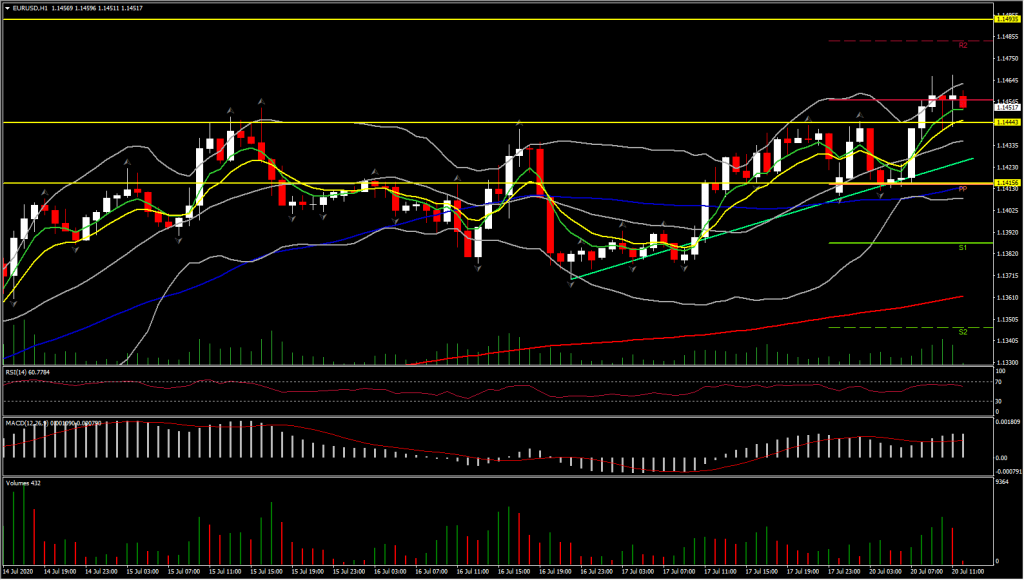

The euro has been in the outperforming lane amid signs that EU leaders are heading for a compromise on the EU recovery fund. EURUSD pegged a fresh four-and-a-half-month high at 1.1467, drawing nearer to the early March peak at 1.1494, which is the loftiest level seen since January 2019. EURJPY lifted by over 0.5% on route to a 6-week high at 122.98, and EURGBP lifted to a 3-week high at 0.9140.

In the long term meanwhile, Euro expected to remain under pressure with or without a compromise today. Critics have long highlighted the Eurozone’s very large current account surplus and demanded a more balanced policy that focuses more on domestic investment than exports, so these trends are not necessarily a negative for the Eurozone going forward – at least if companies and economies – in particular Germany – manage to adjust.

Earlier , ECB’s de Guindos suggested taht Q2 GDP wasn’t as bad as feared. The initial estimate had been for a contraction of around 13% in the second quarter, and even if things were not quite as bad as feared, the Eurozone will likely be left with a sizeable contraction and a sharp decline over the quarter. It will take a while for economic activity to come back and that will also depend on whether and to what extend there will be further lockdowns once the regular flu season starts. That in turn will not just depend on whether there will be a vaccine, but also whether acceptance of less restrictive measures – such as the wearing of masks – rises across Europe.

The all-case mortality curve in Europe is now below the long term trend. Regardless of the not-anywhere-near-as-bad-as-initially-feared data on the coronavirus, the impact of lockdowns and persisting shifts in consumer behaviour will restrict potential for economies to recover to pre-pandemic activity levels.

Click here to access the Economic Calendar