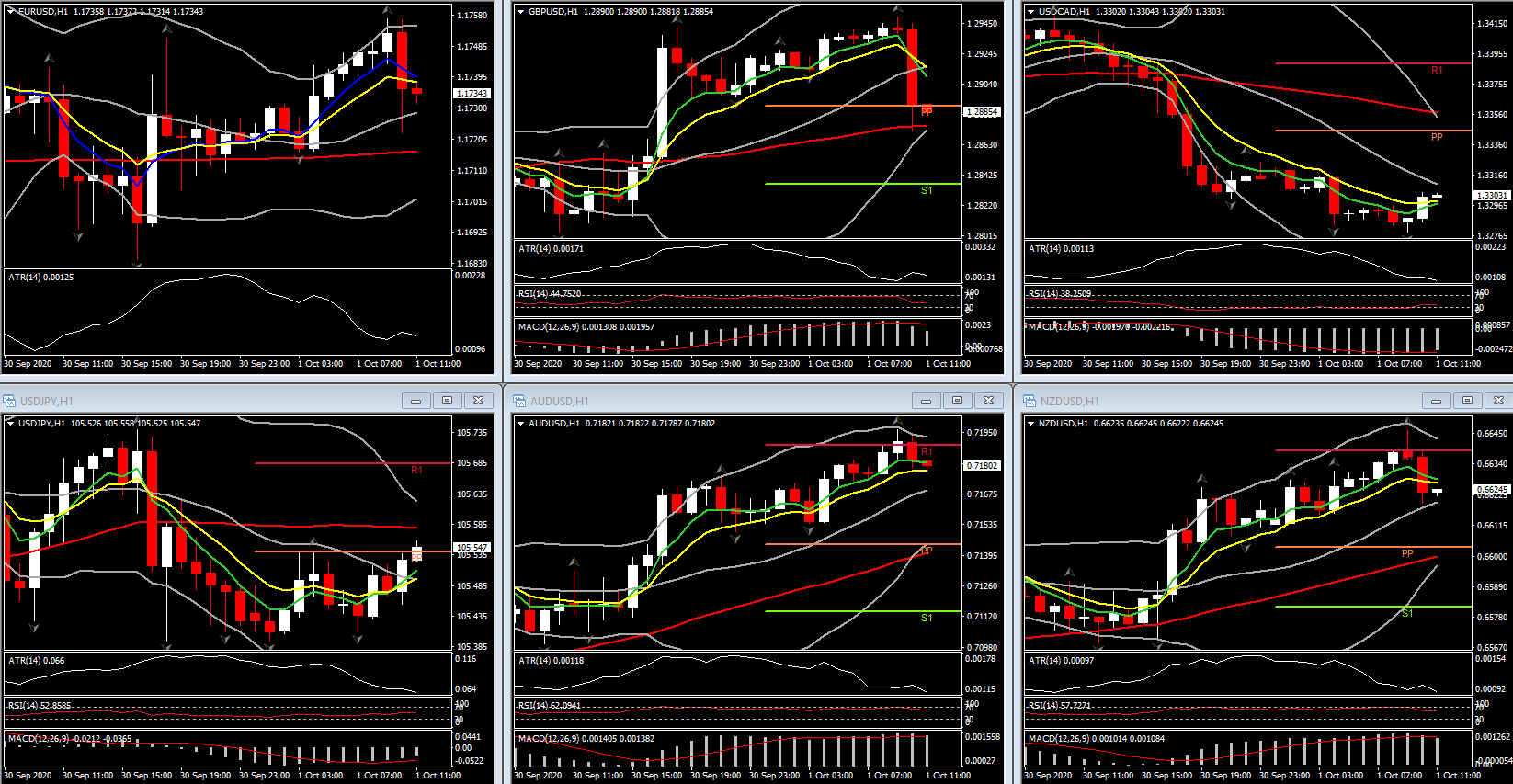

The US Dollar and Yen are back in the underperforming lane, with both currencies once again correlating inversely with global stock market direction. The USDIndex is down for a fourth consecutive day in posting a 9-day low at 93.64, while EURUSD has lifted to a high so far at 1.1754, which is 2 pips shy of yesterday’s 9-day peak.

The commodity-correlating Dollar bloc currencies, and many developing world currencies have also risen against the Dollar and Yen. AUDUSD, for instance, posted a nine-day high at 0.7197. USDJPY plied a narrow range around 105.50, while EURJPY lifted above 124.00 and AUDJPY rallied by over 0.5% in printing a 10-day high at 75.94. The Pound traded mixed, rising moderately against the Dollar, and holding steady versus the Yen while losing ground to the Australian Dollar, among other currencies.

USDCAD ebbed to a 10-day low at 1.3277, extending the correction from yesterday’s two-month high at 1.3421. An outbreak in risk appetite, which has boosted global stock markets and commodity prices, has both seen the Dollar weaken while supporting the Canadian Dollar. Oil prices retraced most of the near 5% plummet that was seen on Tuesday, with gains coming after the solid round of US data, including the better ADP jobs report, stronger Chicago PMI, the slightly improved Q2 GDP revision, and the better than forecast pending home sales print. Key for oil prices will be the closing level, with a sub-$40 finish likely to keep pressure on prices, while a close above the level is set to shift sentiment toward the upside. New Covid outbreaks around the globe will be watched closely as a barometer on oil demand going forward.

Market participants are waiting on developments from what is the final week of formal future relationship negotiations between the EU and UK. A variety of factors helped support equities, including hopes for a last-ditch effort for fiscal stimulus in the US, stronger than expected US data yesterday, and positive news on a vaccine. Those helped offset jangled nerves after the raucous US presidential debate Tuesday night added to anxieties about a contested election. Data out of Asia today focused on the Japan manufacturing PMI and Tankan surveys, which both suggested an improvement in sentiment, although the PMI headline, at 47.7, shows that the manufacturing sector remains in contraction. Note that Chinese and South Korean markets were closed, while a systems glitch on the Tokyo Stock Exchange disrupted regional equity trading.

Ahead today are final September manufacturing PMI readings out of Europe, along with the US ISM manufacturing survey and weekly jobless claims.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.