The UK currency took a sharp rotation lower on Brexit related developments. Weighing were reports that the EU and UK are struggling on key issues in trade negotiations, and with the European Commission president von de Leyen announcing that the EU has taken the first step in a legal infringement procedure against the UK in relation to the controversial Internal Market Bill. However later on an FT report cited UK officials with inside knowledge saying that the EU and UK have reached a compromise on the state aid issue, contrary to an earlier Reuters article, which had cited EU sources. Fishing rights remains a sticking point, apparently.

The EU recovery fund is likely to be delayed just as nearly all European countries are ratcheting up Covid restrictions. And this comes amid the ECB campaign of verbal intervention to keep a lid on the Euro. Similar messaging from other central banks, including the BoE and RBA, has also contributed to an overall weakening in the strongly bearish Dollar bias that forex market participants had until recently. The rhetorical interjections countervail the impact of the Fed’s regime shift to a lower-for-longer stance on interest rates.

In Europe, positive Covid test results have continued to soar in most countries. Covid hospitalisations and mortality, while bumping higher over the last week in many countries, still remain at basement levels relative to the March/April peak. The ratio between Covid-caused death and flu- and pneumonia-caused death also remains low, again contrasting markedly to the March/April situation. Nonetheless, the trend in most countries in Europe is for tighter restrictions and more localized lockdowns, which should limit the upside scope of the Euro.

EURUSD earlier posted a 9-day high at 1.1769. EURJPY gained, too, with both the Dollar and Yen having softened amid a backdrop of mostly higher global stock markets. EURGBP dove about 90 pips in returning to levels around 0.9065-75. Heads of state will bring the issue to a resolution at the October 15th-16th EU summit. The odds for a deal being struck now appear much greater, though how extensive any deal will be remains uncertain, and there is a risk that the UK will see a downward jolt in its terms of trade when it leaves the EU’s single market on January 1.

European stock markets have pared early gains. The UK100 outperformed as the Pound sold off and the UK Gilt future is currently down by 0.2%, while the GER30 underperformed and lost most of its early gains amid the rise in local virus case numbers and with Bayer AG under pressure after a profit warning. This comes in contrast to the European final manufacturing PMIs, which confirmed the improvement in sentiment.

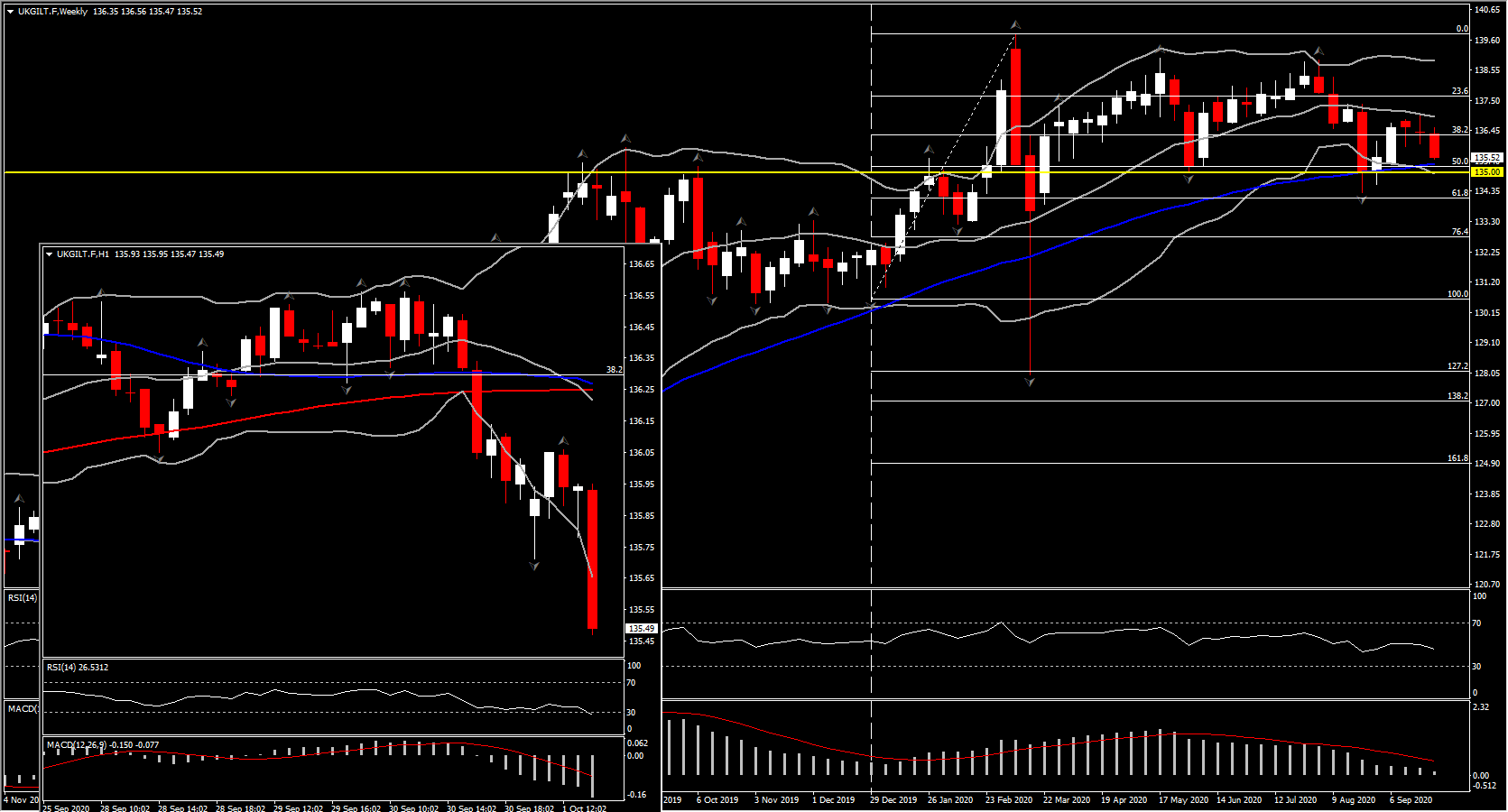

The UKGilt has had a key downside move that is potentially outlook changing, breaking the 200-Day MA and resuming the 2-month downtrend. The UKGilt is heading towards the support band 135.30/135.00. The rebound from 134.20 to 136.98 last week is now the medium term resistance area. Given the deterioration in momentum we have seen, with RSI into the 40s and MACD lines sustaining a move into negative area, the outlook is becoming increasingly worrying for the bulls. If this 200-Day MA at 136 continues to be seen as a sell zone, the downside pressure will grow. Initial Support, at 50% Retracement level on year’s rally and 50-week SMA, is a key level. If this is breached on a closing basis it would open 132.80-132.00 which is the year’s low area, however a strong obstacle will be the 61.8% fib level at 134.00. How the market reacts around 134.00 would then be the key as to whether this is a near term upswing or something far more bearish.

Generally though investor sentiment was boosted by headlines suggesting progress on the next US stimulus package, and US futures are up 0.8 to 1.3%, with the USA100 outperforming. The vote on the Democratic proposal was delayed to give negotiators more time to come up with a compromise deal as Fed officials warn against delaying a new aid deal until next year.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.