The outlook isn’t good for either the UK or Europe given the surge in new Covid cases. New restrictions, from travel limitations to pub closures to local lockdowns, are being introduced almost daily in the UK, and this will have a negative impact on economic activity. The government’s furlough scheme is being withdrawn this month, and being replaced by a narrower, more targeted wage protection scheme, though the Chancellor has announced there will be a new scheme to support those affected by local lockdowns. Dovish signalling has come from the BoE governor this week, similar to policymakers at other central banks.

Attention remains fixated however……

Attention remains fixated on the final phase of talks between the EU and UK, with less than one week to go until the EU’s summit. Despite the public brinkmanship, there have been reports from behind the scenes of motion toward finding a compromise on key issues from both UK and EU sources. Any news of a deal would likely boost Sterling over the near term.

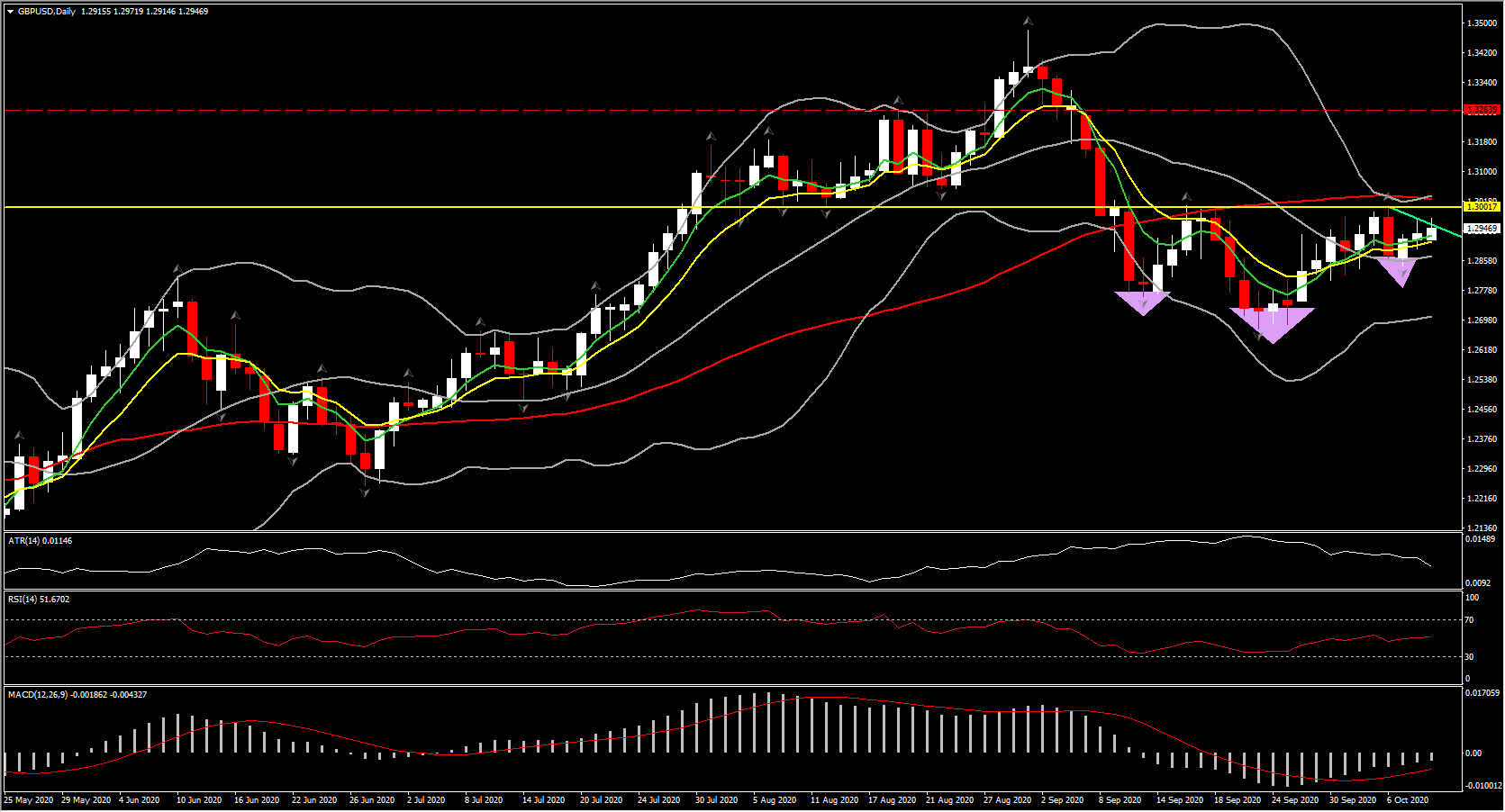

But even with a deal, and even with UK progress in signing continuity agreements with non-EU trading partners, the UK will see its terms of trade position deteriorate. It has also become increasingly clear that London’s European dominance in financial services will erode, deal or not. The technical picture of Cable is overall neutral after Tuesday’s bearish engulfing candlestick pattern at the 1.3000 area. However the asset reversed again to the upside retesting that area once again. Interestingly an inverse head and shoulders looks ready to be formed, however how the market will respond and whether or not it will confirm the formation depends on next week’s summit. A decisive move above 1.3000 and the 50-DMA could indicate a boost to August highs, while a pullback to 1.2700 lows would increase the negative momentum.

Next week’s Summit

The October 15 EU summit that was originally seen as the deadline for Brexit talks, and which Boris Johnson still flags as the point where the UK will walk away even if there is no deal, is just a week away and the chances that there will be an agreement at that point is almost non-existent, despite latest comments from officials. EU Commission President Von der Leyen and UK Prime Minister Johnson may have agreed to extend official talks during a recent phone conversation, but the fact that these seem to still be regular talks, rather than “tunnel” discussions based on agreed “landing points” on key issues, highlights that differences remain too large to get a deal done quickly.

Listening to the UK side, the question of how to deal with fisheries and future access to UK borders is the key point, but while that clearly is important as a signaling factor for the UK public and important for some EU member states, the more pressing issues for the EU are level playing field rules, the governance of any agreement and the future cooperation on data sharing on security and crime fighting. Indeed, level playing field rules and governance could be the key to any agreement.

Not that EU states are in any mood to give ground on fishing at the moment and indeed, while it seems at first sight that the UK has every right to exclude the EU’s fleet from its own waters, most of the fish found in UK waters is actually sold and eaten in the EU. The fishing issue, which is a big part of the UK government’s narrative at home (more so than the right to subsidise companies) clearly is a bargaining chip that national heads of state don’t want to give up as long as talks remain at negotiator level.

Next week’s summit will bring an opportunity to take stock and maybe pave the way for “landing zones” that would allow the move towards “tunnel talks” later in the month.

That would push the timing of the likely showdown into early November. Given that any agreement still has to go through a legislative process on both sides of the Channel and that there is a clear risk that the EU parliament will reject any deal if the UK’s Internal Market Bill is not scrapped or modified by then and that Johnson may face defeat if he makes too-big concessions on fisheries, there are still pitfalls ahead.

Ultimately both sides want a deal and it is widely hoped that there is very likely going to be one, although it is also likely to be limited in scope. For the Brexiteers the opportunities that await outside of the EU and its regulations make up for that. The recent agreement with Japan was a case in point, with the UK barely able to match the agreement the EU has with Japan. At the current juncture, the best the UK can hope for is to replicate the deals the EU already has.

Even with a tariff free, quota free deal, the UK’s loss of unfettered access to the single market and customs union would lead to trade destruction.

UK exporters would face cost-increasing non-tariff barriers, such as customs formalities and regulatory barriers. The same would be the case for EU exporters to the UK, though the impact would be much magnified on the UK side of the Channel. Productivity would also be impacted, given reduced competition and reduced scope for businesses to benefit from economies of scale.

Financial services — a golden goose that accounts for 22% of government tax receipts — is a particular concern. A Bloomberg article highlighted the steady stream of financial services resources that are being moved out of the UK to the Eurozone, and the fact that even with an EU trade deal in place, London will likely continue to lose business to Eurozone financial centres as the “equivalence” regime on rules would leave firms with long-term uncertainty.

Hence with or without this year’s pandemic, the transition would have been difficult. The UK is likely to also face a huge rise in structural unemployment, as Brexit will cut off access to the cheap workforce in Eastern Europe, while a large part of those losing their livelihoods now – first and foremost those in services sector – won’t be able to just retrain as builders and benefit from the building boom the government is trying to generate.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.