GBPUSD, H4

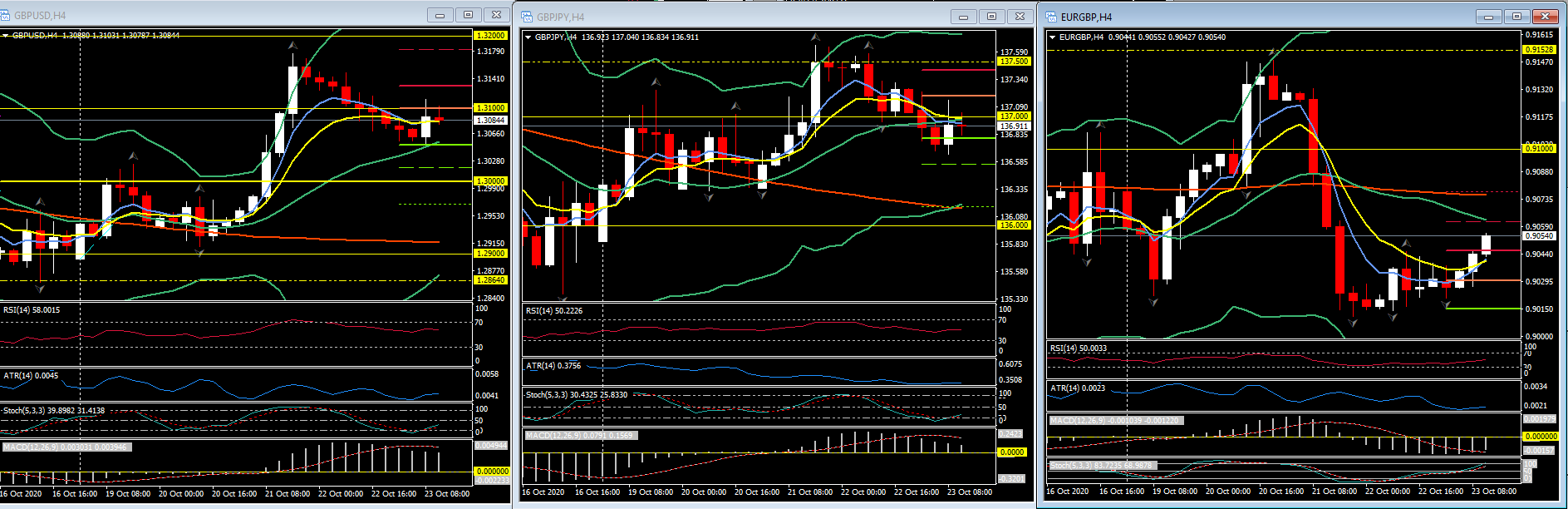

The Pound is trading neutrally, rebounding from a two-day low at 1.3051 in the case against the Dollar but struggling with 1.3100. While seeing limited and mixed changes versus other currencies, GBPJPY pivots under 137.00 and EURGBP runs to 0.9050.

The UK currency remains comfortably up on week-ago and month-ago levels against the Dollar and Euro, and others. The currency market is anticipating a limited trade deal between the EU and UK. The UK and Japan also signed, today (October 23), the trade deal that was agreed in principle a month ago. The northern coastal EU nations have been demanding unchanged fishing access to British waters, and this has been the principal sticking point. EU negotiator Barnier was this week reported by the BBC to have been “frustrated” with leaders of coastal EU nations for not (yet) allowing him to proceed on tackling inevitable compromises on fishing rights. Perhaps he arrived in London yesterday with authorization to open up this front. For the coastal 8, it’s a choice between no fishing rights in UK waters under a no deal scenario versus reduced quotas with an agreement. With a limited trade deal, and taking into consideration the UK’s progress in signing continuity agreements with non-EU trading partners, the UK economy and the Pound would look vulnerable over the medium term. Swapping unfettered access to the EU’s single market and customs union in place of a narrow free trade deal will see trading friction and costs rise.

Uncertainty about the UK’s outlook will likely remain well into 2021, as the relationship between the UK and the EU will be an evolving one. This backdrop, along with the direction of travel in the Covid situation and associated restrictions, should be viewed as potential negatives for the Pound, given the risk of lower foreign capital inflows, which are needed to offset structural outflows generated by the UK’s large current account deficit. This said, it should also be acknowledged that the EU and UK might conceivably amaze everyone with a much more comprehensive deal than is being expected. The Covid situation may be a motivation for this, and it should be remembered that the two sides are starting from perfect equivalence, so a broad agreement is entirely possible. Even Brexit ideologues in the UK might be persuaded that maintaining close alignment with EU rules — for now — may be the more pragmatic way forward given the Covid stresses.

The UK’s preliminary October PMI fell to a four-month low of 52.9 in the headline reading. The outcome missed the median forecast for 54.0 and contracted from the 56.5 reading that was seen in September. The private sector economy is split between weakness in the dominant service sector and relative strength in the manufacturing sector. The preliminary October services PMI dove to a reading of 52.3 from 56.1 in the month prior, while the decline in the manufacturing headline was less pronounced, falling to 53.3 from 54.1. A drop in new orders was reported in the service sector, while a rise in new orders was seen in manufacturing. Overall, the economy remains in expansion, though the steepness of the decline from the six-year high seen in August at 59.1 is worrisome, with the outlook looking grim due to rising Covid cases, with Wales entering a full-strength two-week lockdown, and ever more stringent restrictions being imposed across large areas elsewhere in the United Kingdom, including Northern Ireland and Scotland, along with much of northern England and London. Export demand is also weakening due tightening Covid restrictions across much of Europe. This backdrop is clobbering the hospitality sector in particular, along with the travel and high street retail sectors.

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.