GBPUSD, H1

The Pound and Euro posted respective two- and three-day lows against the Dollar as anxieties about Brexit took hold, although magnitude of movement has been limited so far. Both currencies posted 10-day lows versus the Yen, though fared better against the dollar bloc currencies with global stock markets and commodity markets seeing cautious trading after recent strong gains. The Pound itself underperformed relative to the Euro, which saw EURGBP lift to a 0.8958 high, which reversed most of the decline seen yesterday. Neither the UK or EU has blinked as trade negotiations go right down to the wire, while there are reports that Brussels bureaucrats are fretting there won’t be sufficient time to ratify a deal before the January-1 deadline and news that the EU is drawing up emergency no-deal plans today. An EU diplomatic source cited by the Sun tabloid said that the two sides are “nowhere near” an agreement over fishing rights and said that they had “gone backwards” on agreeing common standards, adding that talks can only continue to mid next week before “time will get the better of us.” While the drama is imparting downside bias on the Pound and Euro, both currencies, and especially Sterling, would be considerably lower if markets were committed to pricing in a no deal scenario. Bigger picture market participants are preferring to wait on concrete developments, though near-term speculators are starting to prod the Pound lower now. Expectations are that win-win will prevail rather than lose-lose, and that an accord will be reached. Will it be this weekend, will it be next week? – no one truly knows but it is in both parties’ interests to get to the “handshake”.

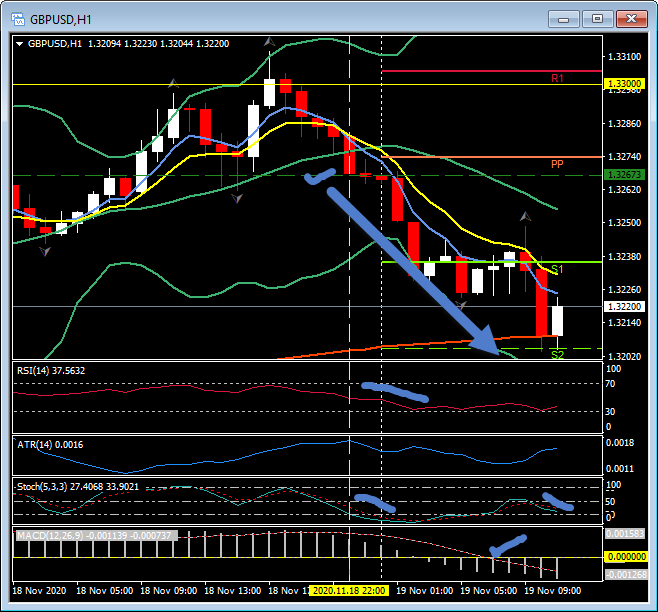

Cable continues to find support at 1.3200 and struggle at 1.3300, with the last move triggering lower under the 20-hour moving average yesterday at 1.3267. It has continued to move lower today below S2 before finding support at the 200-hour moving average at 1.3207, so far today. The MACD Signal line breached the 0 line earlier and the fast moving averages are aligned lower, RSI is 38 and weak and the Stochastics are still moving lower and not yet into the OS zone. The 60-pip move lower represents 3.5 times the H1 ATR. The Daily ATR is currently 117 pips.

Cable continues to find support at 1.3200 and struggle at 1.3300, with the last move triggering lower under the 20-hour moving average yesterday at 1.3267. It has continued to move lower today below S2 before finding support at the 200-hour moving average at 1.3207, so far today. The MACD Signal line breached the 0 line earlier and the fast moving averages are aligned lower, RSI is 38 and weak and the Stochastics are still moving lower and not yet into the OS zone. The 60-pip move lower represents 3.5 times the H1 ATR. The Daily ATR is currently 117 pips.

US Initial Claims Preview:

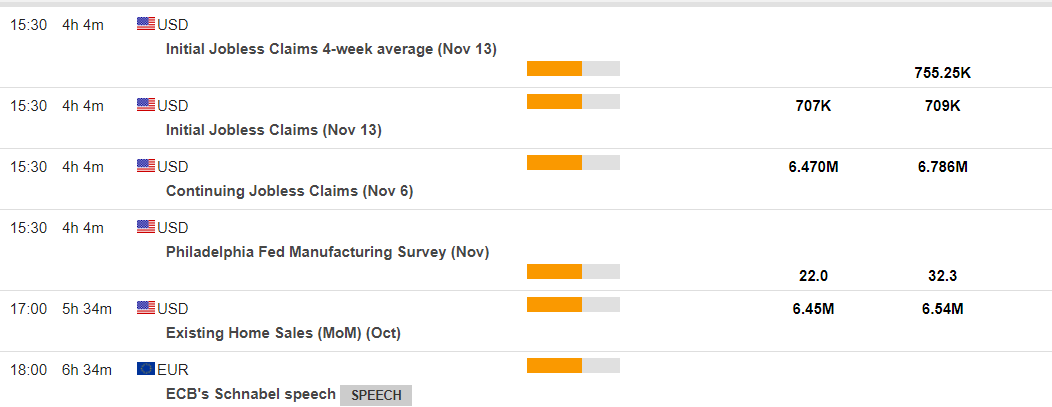

Consensus forecasts are for a -2,000 slide in initial claims to a 707,000 pace in the week ended November 14 after the -48,000 drop to 709,000 in the prior week. Note that the current figure will take on extra importance since it coincides with the BLS survey week. Claims are expected to average 684,000 in November, after averages of 786,000 in October, 855,000 in September and 992,000 in August. The 797,000 October BLS survey week reading undershot recent BLS survey week readings of 866,000 in September and 1.104 million in August. Assumptions are currently for a 750,000 November payroll rise, after gains of 638,000 in October, 672,000 in September, and 1.494 million in August.

Join me LIVE on our Facebook Groups for Live comment and analysis of the US Initial and Continuing Jobless Claims data, the Philly Fed Index and the Canadian ADP Non-Farm Employment Change. All due at 13:30 GMT.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.