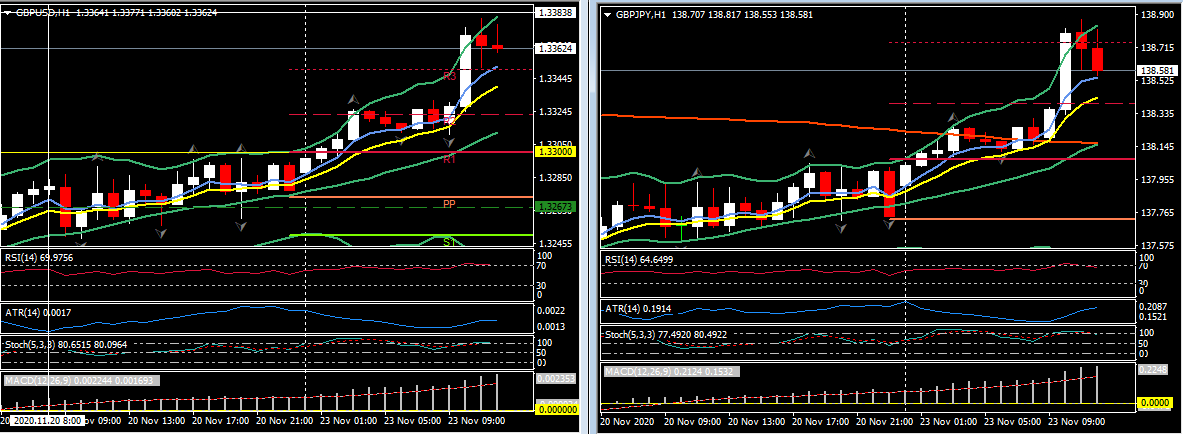

The Pound’s rally has accelerated in London trading. Both Cable and GBPJPY are showing gains of just over 0.7% at prevailing levels. Cable has posted a 12-week high at 1.3380. EURGBP, meanwhile, has declined to an 11-day low at 0.8874, drawing in on the 12-week low seen earlier in November, at 0.8858. Brexit news has been positive. There are widespread reports of a trade deal being struck by mid this week, with the BBC’s European correspondent Katya Adler, for instance, reporting that “the general expectation is that a deal will be done in the next few days,” while a source cited by Sky reported that a deal is “95% agreed.” It has also become clear that officials are determined not to let the fishing rights issue, which is the principal obstacle (much more so than level playing field rules and governance issues), prevent a deal from being reached. A fudge is reportedly in the works, which would allow the fishing issue to be reviewed in the future. We have been anticipating that win-win will prevail rather than lose-lose, and that an accord will be reached.

The Pound is likely to see further upside, especially on any concrete news that a deal has been reached, and with the UK reportedly close to giving the Pfizer vaccine (of which the UK pre-ordered 40 mln shots) regulatory approval as soon as this week, with a rollout starting as soon as December 1. Also, AstraZeneca says¹ its vaccine has a combined efficacy of 70.4% and a double dose regime raises this to 90%. Although not the headline grabbing 95% from Pfizer & Moderna, the AstraZeneca solution is significantly cheaper and has many global pre-orders.

The UK saw a bigger peak-to-trough GDP contraction than any other G20 nation in 2020 as a consequence of the national and global countermeasures taken to table Covid-19 (the essential reason being the UK’s dependence on foreign capital inflows to fund its gaping current account deficit, and the shortfall in capital inflows as a consequence of the pandemic). The logic is that the UK should be a big economic benefactor in the vaccine-assisted return-to-normalcy scenario. The caveat here is how broad, or perhaps how narrow, a deal the EU and UK strike. A narrow deal would mostly benefit manufacturing while leaving the dominant service sector vulnerable.

However, the UK’s preliminary November composite PMI dropped much less than expected, coming in at 47.4 in the headline reading, down from 52.1 in October and a six-month low, but still comfortably above the median forecast for 42.5. The decline was driven by services, which overwhelmed an unexpected increase in the manufacturing PMI. The difference in performance between the service and manufacturing sectors was at the widest in almost 25 years of collection, reflecting the asymmetrical impact that Covid-related restrictions are having on the economy, which have been heavily centered on the hospitality and retail sectors.

The services PMI headline dropped to 45.8 from 51.4 in the month prior, but was still better than the median forecast for 42.5. The manufacturing PMI surprised by rising to a 55.2 headline reading, up from 53.7 in October. The median forecast had been for a decline to 50.5. The overall much better than expected readings are testament to the adaptation by businesses, which has evidently been greater than economists had judged. Anecdotally, the UK economy has been turning over with surprising vigour, with the major exceptions of high street retail and hospitality, along with gyms, live entertainment and certain other areas. The lockdown restrictions are much less severe than they were during the first national and global lockdowns seen earlier in the year, which drove the UK composite PMI headline to a 12.9 reading — over 34 points below today’s level — at its nadir in April. With regard to the stellar performance of the manufacturing sector, there are caveats. Intense, but temporary, stock building ahead of the UK’s year-end exit from the EU’s common market and custom union has been afoot. There was also a sharp lengthening in supplier delivery times due to severe delays at UK ports.

Across the English Channel the Eurozone composite PMI was weaker than expected, as it moves back into recession. The preliminary reading for November fell back to 45.1 from 50.0 in the previous month, which confirms that the return of lockdowns has led to a renewed contraction in overall economic activity. Data confirmed that the services sector has been hit hard by virus developments, but also confirmed the very uneven picture across sectors and countries, with German manufacturing actually holding up pretty well and coming in higher than expected at 57.9 in November, while the French manufacturing reading dropped to 49.1 from 51.3. That left the Eurozone number at 53.6 – down from 54.8 in October, but still indicating solid expansion, while the services reading dropped to just 41.3 from 46.9. Not an easy situation for the ECB, although even with positive vaccine developments, the central bank remains on course to at least extend the PEPP program at the December meeting.

¹https://www.bbc.com/news/health-55040635

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.