Crises are often a transformative force. While some developments turn out to be temporary, others persist long after the crisis has ended. The Covid-19 crisis will have long-term consequences.

Over the past 20 years, China has increased its competitiveness from producing about 5% of industrial output worldwide to 30%, while the US share has fallen from 25% to 18%. The West has promised to increase local export capacity and manufacturing jobs, but doing this on a scale that could cause a rapid rebound in the US or European market share of global production is highly unlikely in the short term. Trade barriers and friction that have increased since 2016 are likely to remain going forward and a trade deal between the US and the EU is in progress, while tensions over technology and investment are likely to remain or may get worse. In response, China is currently making significant investments in the semiconductor industry to reduce its reliance on other less friendly trading partners. This could lead to duplication of the supply chain.

Protectionist tendencies could also increase in the field of medicine, with lobby groups trying to suggest that the Covid-19 crisis proves the need to produce strategic supplies nationwide. A far better approach is to ensure, through multilateral or bilateral agreements, that a diversified global supply is available in a future health crisis.

China is at the forefront of recovery from the pandemic compared to other countries. It was the first country to enforce a lockdown and the first to lift it. At present, China’s industrial production has recovered most of the decline, and China will be the only major economy to post a positive growth rate for 2020, with China’s real GDP expected to grow by 2.2%. The course of the recovery from now on will depend more on restoring jobs, which continue to face challenges (tourism and entertainment are still far from recovery).

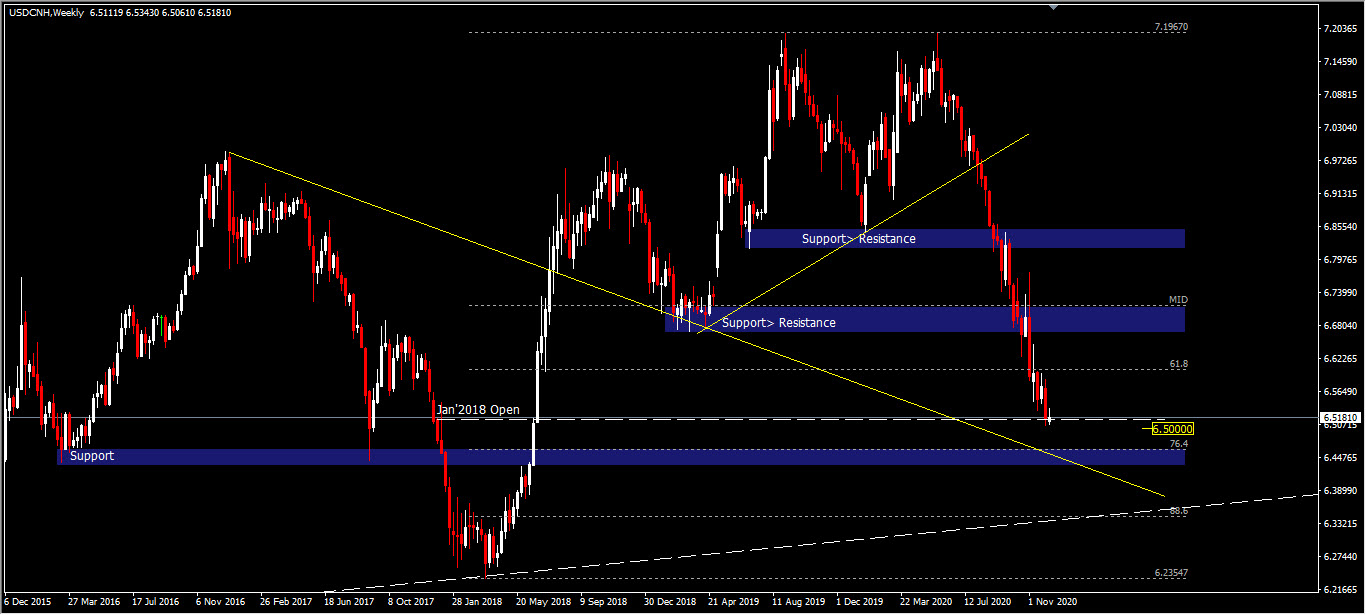

USDCNH has been trading weaker since last May. CNH strengthened against the US Dollar from a peak of 7.1950 down to 6.5150. The price bias still shows the dominant seller amid the broad weakening of the USD. The next area to be watched is in the Support zone in the range of 6.4700 with a note that prices have surpassed the January 2018 opening. On the upside, as long as the Support level of 6.4700 persists, there is a possibility for a correction from a decline of 7.1950 to around 6.6699 a Support level that becomes Resistance.

Click here to access the HotForex Economic Calendar

Ady Phangestu

Analyst – HF Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.