BAC Q4 Earning review

Bank of America is in line to publish its earnings report tomorrow, January 19, for Q4 2020, before the market opens. As it was a wandering year from the very beginning, last quarter earnings have so far amazed the markets with the first banking reports of last week, from JPMorgan, Morgan Stanley, and Citigroup all publishing better than expected EPS, however, lower revenue and not very good outlook for next quarter especially hurt their stock prices.

All the unexpected market movements in 2020 saw the first and last quarter of the year at exactly two opposite sides, with sharp slides in the first quarter and a sharp rise in last quarter, however, as we saw that the results of the first quarter were not as bad as share price performance, for this quarter, we can also expect a similar opposite effect on share price and real revenue.

What mainly affects the bank’s net income is taking a part in FED stimulus packages like loans, direct check payments, and Bond Purchase Schedules. Based on that, the important points that will come from the report are:

- The Bank’s individual loans

- Mortgage loans (which have been raised after lower rates)

- The Bank’s net income and next quarter outlook

- Percentage and amount of bad loans (many individuals and businesses were not able to pay back their owed credits)

Any positive/negative data and information about the above topics move the market up or down fundamentally. However, that is not all. As a new administration comes to the White House and President-elect Biden comes up with new stimulus package, it is also very important to watch the market reaction should it get approval from both House and Senate, not just in the short term but in the mid-term.

Market Expectations

“The Zacks Consensus Estimate for fourth-quarter earnings is pegged at 56 cents, which suggests a decline of 24.3% from the year-ago reported number. The consensus estimate for sales of $20.40 billion indicates an 8.7% decline from the year-ago quarter’s reported number.”

In the past 8 quarters, BAC has beaten EPS estimates by more than 80%, which reassures its investors as well.

Technical review

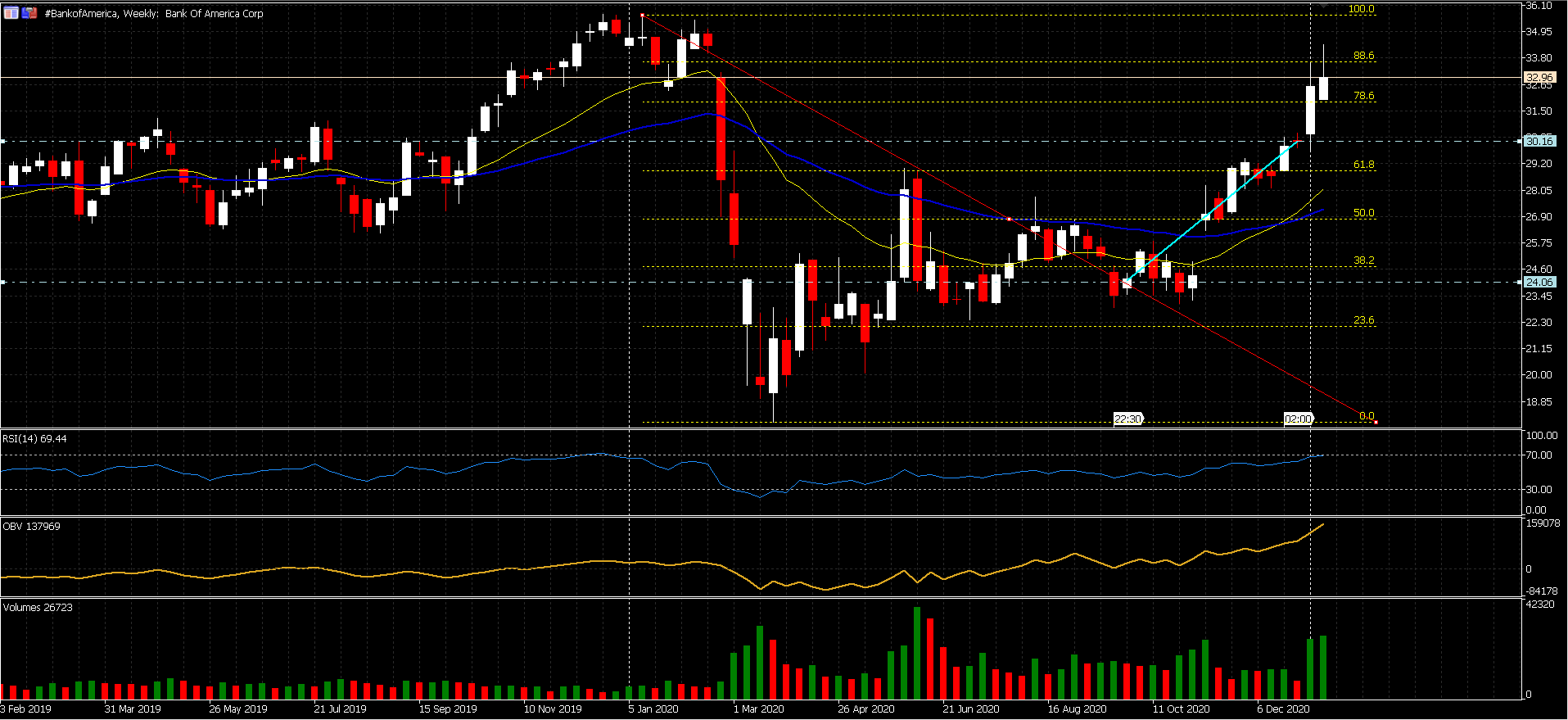

With 25% growth in the fourth quarter and continuing at 15% in the first two weeks of 2021, the share price could reach the pre-pandemic January 2020 price seen before last Friday’s free fall, after the first banking reports. The current price is way above the key level of 61.8% Fibonacci, above 78.6%, which keeps a positive tone alive, as long as it is trading above $29. Negative results and market reaction can move prices lower, however, $49 is still key support, while above the current level, $34.45 (2021 high), and then $35.75 (all time high, seen in December 2019 and January 2020) will be in the spotlight.

Click here to access the HotForex Economic Calendar

Ahura Chalki

Analyst – Regional Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.