GBPUSD, H1

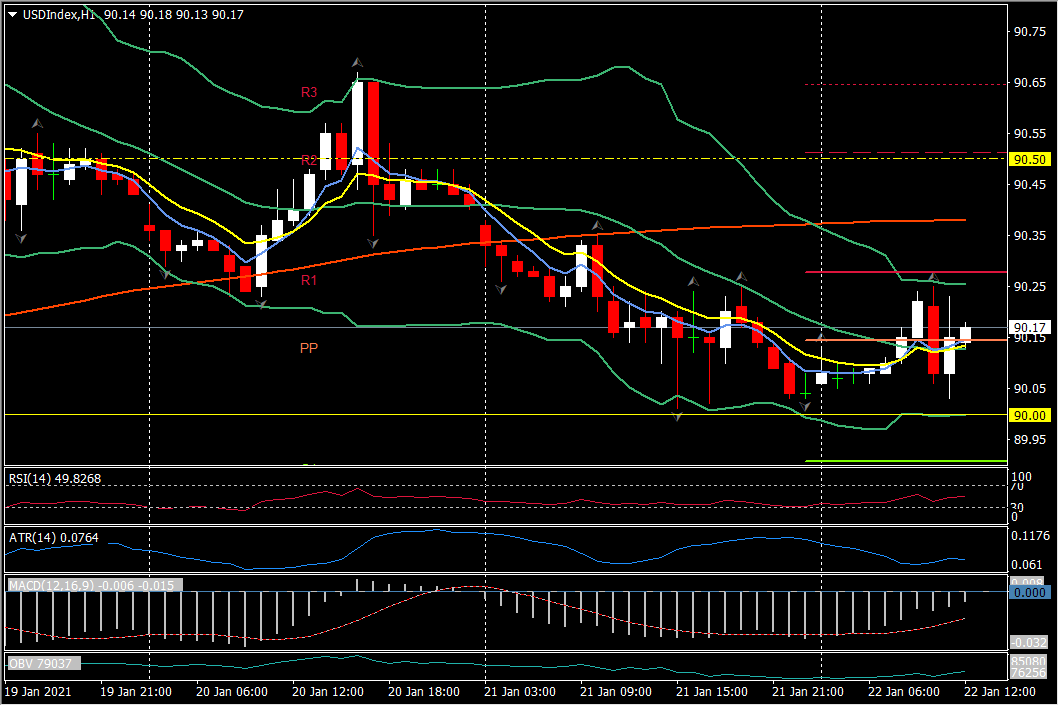

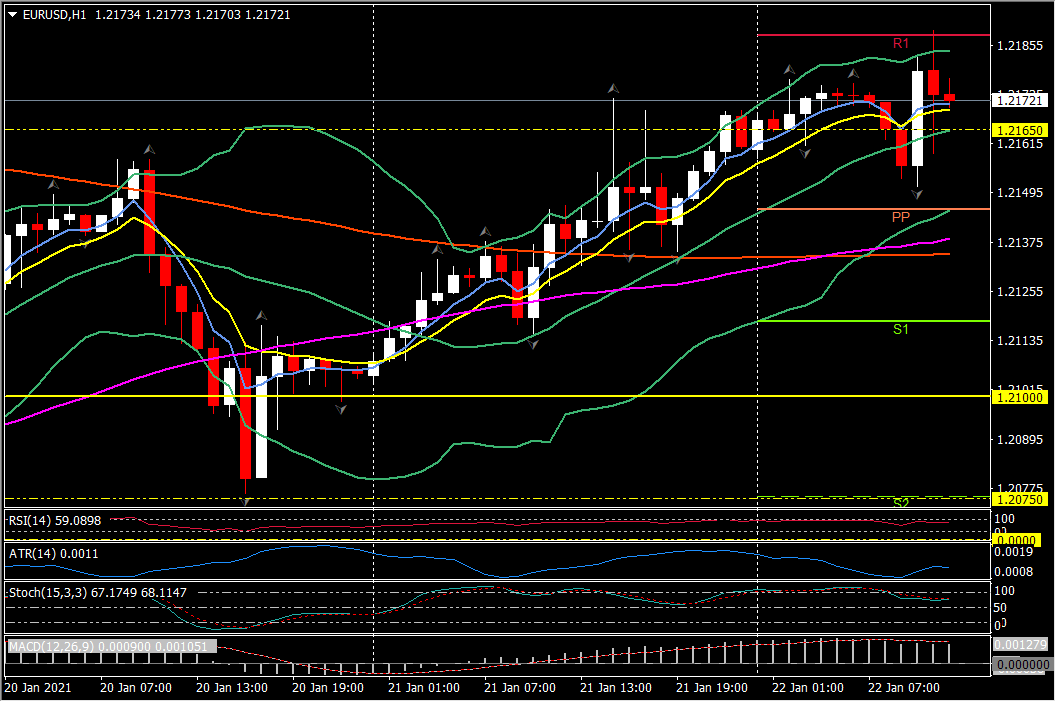

The Dollar has firmed up on a safe haven bid with the reflation trade having come to a firm stop. The USDIndex lifted moderately to a 90.25 high after basing out at a nine-day low at 90.05. The US currency gained only marginally against the Euro and Yen, but racked up gains of around 0.4% to 0.5% against the Pound and dollar bloc currencies. EURUSD ebbed back from an eight-day high at 1.2178, before recovering to 1.2188 following Eurozone PMI data, while USDJPY lifted to a two-day high at 103.70.

Global equity indices corrected from record highs in the cases of the main US indices and the MSCI Asia-Pacific Index. Base metals are also markedly lower. Lofty valuations and an increasing level of concern about the Covid situation have warranted increasing investor caution. Covid restrictions have been implemented across northern China, and the new highly transmittable variant of the SARS-Cov2 coronavirus — aka the British variant, where it was first detected — has shown up as far afield as Beijing and Australia. The EU looks set ban travel to the UK, while the UK has already imposed much tougher international travel restrictions. The rollout of the Covid vaccinations globally has also been proving to be bumpy.

Elsewhere, cryptocurrencies dropped sharply again, which will only add to their reputation for being too volatile for serious institutional investors to touch. Reports that the Biden administration has tighter regulations for cryptocurrencies on its ‘to do’ list have been driving cryptos lower. Bitcoin was showing an 11% loss on the day, as of the early London morning, at $30,860 — which is nearly 26% below the record high seen earlier in the month. The virtual coin earlier traded below $29,000 for the first time since January 1.

Eurozone Flash PMI readings declined as lockdowns were strengthened and/or extended. The last minute Brexit deal may have helped to prevent a worse number for the manufacturing sector at least, and the decline in the Eurozone manufacturing reading to 54.7 from 55.2 was actually less pronounced than feared with the number still pointing to a solid pace of expansion. Services meanwhile are clearly suffering. The Eurozone services PMI dropped back to 45.0 from 46.4, driven largely by a sharp deterioration in the French reading, which fell to 46.5 from 49.1. The German index held up better than feared and dipped only slightly – to 46.8 from 47.0. The overall composite for the Eurozone came in at 47.5, down from 49.1 at the end of last year and supporting expectations for a technical recession over the Q4 and Q1 period.

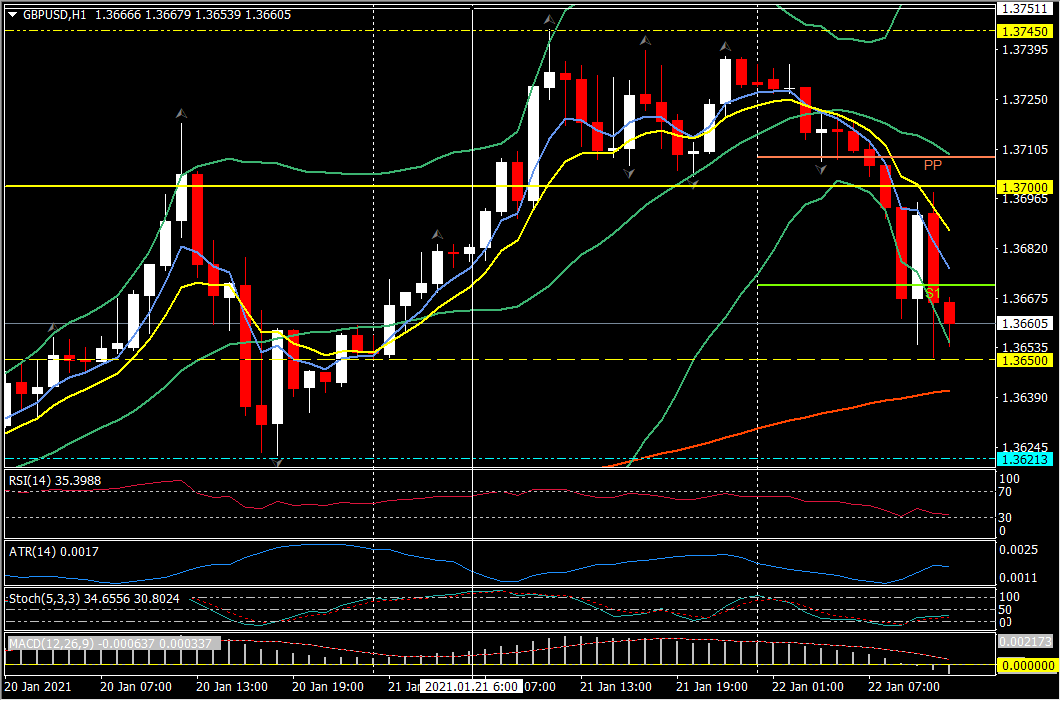

Across the Channel UK PMI data showed a woeful record for Services and came in much weaker than expected. The headline composite PMI plunged to 40.6 from 50.4 in December. The median forecast had been for a 45.5 reading. Pronounced weakness in the service sector drove the composite lower, with services bearing the brunt of the lockdown across the UK nations, which has been the most severe since last year’s ‘mother’ lockdown. The prelim services PMI headline dove to 38.8 from 49.4. The prelim manufacturing PMI fell to a headline reading of 52.9 from 57.5, which was near the median forecast for 53.0. Much of the manufacturing sector remains open, despite the lockdown. The drop in the composite reading, while sharp, is still less much less severe than was seen during early spring last year. There are hopes that the UK’s world-leading vaccination programme will start to see restrictions lifted from as early as mid February, by which time all the most vulnerable groups should have been vaccinated.

Cable trades down to test 1.3650, down from yesterday’s high at 1.3745 and today’s open at 1.3729.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.