It has been a decent week so far for Treasuries, with relative stability helping underpin equities until a late -2% drop in the USA100 erased the gains in the USA30 and USA500. There wasn’t much new to really drive the markets. Concerns over a third wave of the virus and tighter restrictions kept a bid in bonds. Wall Street overall remains mixed with modest reflation gains supporting the indices on strength in materials and industrials as the Biden administration muses about a $3 tln infrastructure bill.

Headlines:

- China bourses swinging between gains and losses. US regulators revived threats to remove China’s largest corporations from their bourses and fears of a revival of serious US-China tensions weighed on sentiment.

- Vaccines remain scarce and against that background there are some countries in the EU demanding export bans, a topic that will be high on the agenda at the EU summit that starts today, although maybe the threat alone will help to ensure that the EU finally gets the doses promised and paid for.

- Nothing new from Powell or Yellen in their testimonies to the House Financial Services Committee.

- Both underscored the importance of the Treasury’s and Fed’s quick and large actions a year ago in response to the unprecedented impacts from the pandemic. The worst was avoided, said Powell. But despite the massive stimulus, both believe that a full recovery is still a long way off, next year at the earliest.

- Fedspeak from Powell and others continued to assure a lower-for-longer policy stance with little concern over a pop in inflation.

- EU and UK made a joint announcement to try to ease tensions over a potential vaccine trade war, with the parties looking for a “win-win” solution. Attention will be on the EU leaders summit Thursday.

- Oil prices jumped on the problems in the Suez Canal after a container ship ran aground , slowing Mid-East oil exports

- Intel was weaker despite announcing plans for new chip factories.

- BoE’s Haldane expects a “rip roaring” recovery, even if consumers only spend part of the savings accumulated during the pandemic.

- BoJ Gov Kuroda says no plans to end ETF buying, or sell any BoJ holdings.

- Former Glencore Oil trader pleads guilty to manipulating prices – Trader is cooperating in ongoing investigation into the manipulation.

Forex Market

USDIndex – moved about 92.50, turning to November 2020 highs.

JPY – lifted to 109, holding 2-week Support at 108.30.

EUR – below 200-day SMA, as concern of a return of serious US-China trade tensions weighed on sentiment, and in Europe, the return of virus restrictions is clouding over the outlook.

GBP – decline continues with Cable at 1.3675.

AUD and NZD strengthened.

CAD – rallied to 2-week highs of 1.2609 in early North American trade, supported by the sharp selloff in oil prices, and a generally firmer USD.

GOLD – at 1733, a small correction after the sharp dip at the beginning of the week.

USOil – recovered to over $61.00 after falling to $57.25 on Tuesday.

Bitcoin – down at 52.8k after Fed’s Evans says cryptocurrencies are too volatile to be a store of value.

Today: Data releases today include German Ifo business confidence, which after yesterday’s extremely strong round of PMI readings could well surprise on the upside. The SNB publishes its quarterly policy review and is likely to stick with the current settings as the outlook remains clouded over by virus developments. Key central bankers set to speak in a panel discussion later today. US GDP, Jobless claims and PCE also on tab.

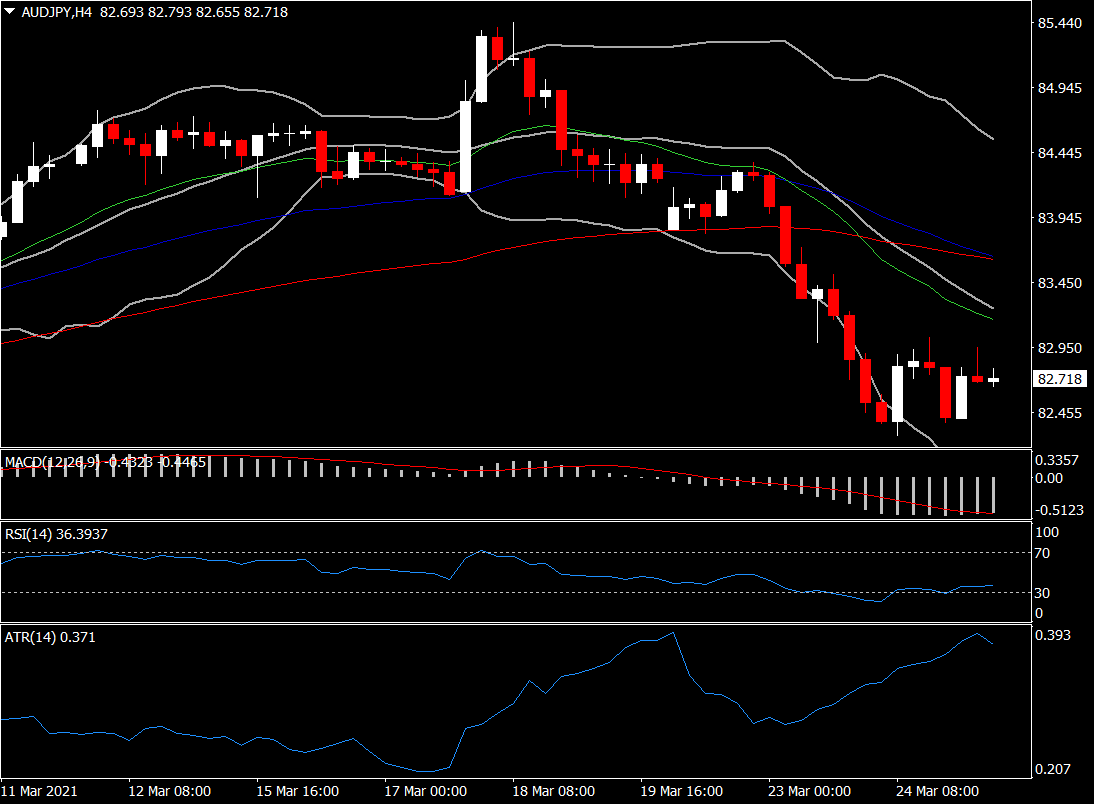

Biggest mover – AUDJPY(+0.45% as of 07:30 GMT) – Reversed yesterday’s losses, rebounding from 50-day SMA. Overall outlook remains neutral as it holds within 2-month territory. Intraday turns neutral as well with price action at 20-hour SMA, as MACD and RSI turned close to neutral zone. H1 ATR is at 0.146 and Daily ATR 0.735.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.