Market News Today – Treasuries are closing the quarter pretty much as they began, with the belly and long end of the market losing ground. The improving outlooks on growth, fostering a hefty reflation trade, have been boosting yields. The market has also been pricing in inflationary pressures. The 10-year was 1.7 bps cheaper at 1.72%, though rates were off early highs of 1.774% and 1.433% respectively on short covering and positioning into month- and quarter-end.

Currently they are posting fractional gains as markets await more details on stimulus from US President Biden, who is set to speak on infrastructure today. Elsewhere the details on the fallout from Archegos’ collapse weighed on sentiment overnight, and after European markets closed broadly higher yesterday, we are likely to see a more cautious tone, ahead of key data.

In FX markets the Yen weakened and USDJPY lifted to 110.85, although the Dollar strengthened against most other currencies, with USDIndex hitting 93.45. AUD and NZD steadied at March lows. The EUR rebounded on EU open at 1.1725 but remains off 1.1800. Cable dropped to 1.3755 (200-hour SMA). Oil prices remain supported on expectations OPEC+ will keep a lid on output, above 50-DMA for a 4th day. Gold remains low at 1,676.

Today – Data releases today include German jobless numbers and preliminary Eurozone inflation data. The former is likely to show a decline in the sa jobless reading, as parts of the economy re-opened, while the latter is seen jumping sharply higher on the back of base effects, although the headline should remain firmly below the ECB’s implicit target of 2%. The final reading for UK Q4 GDP numbers and US ADP are due today, and President Biden is also due to speak.

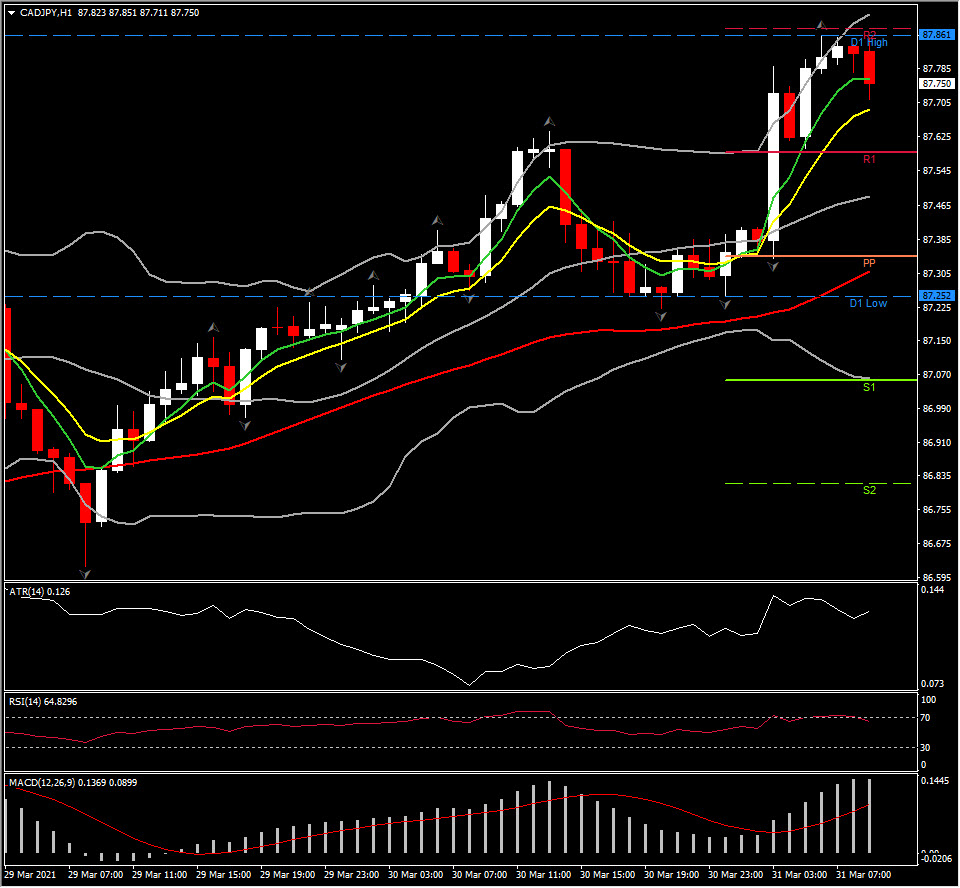

Biggest (FX) Mover @ (07:30 GMT) CADJPY (+0.54%) The asset prices spiked at 87.86 reaching R2 , extending the 6 day rally and recovering nearly all March losses. Fast MAs remain are flattened for now, with RSI turning lower below 70, however MACD histogram & signal line are bullishly crossed. These suggest near term consolidation or even pullback with the overall outlook holding positive. H1 ATR 0.126, Daily ATR 0.65.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.