Japan’s BoJ begins its two-day meeting tonight, and will announce policy on Tuesday. No changes are expected, though the Bank is expected to lower its inflation forecasts, largely due to lower cellphone charges, which will keep expectations for ongoing stimulus in place. The markets are closed Thursday for Showa Day.

Growth optimism seems to be heralding a return of reflation trades, as sharply higher services PPI numbers out of Japan just months away from hosting the Olympics added to signs that companies will pass on higher costs as soon as consumer demand bounces back. The Tokyo motor show was cancelled. In data, Japan March inflation numbers, released last Friday, showed core CPI lifting to a y/y rate of -0.1% from -0.4%. In the meantime investors are wary given lofty valuations and with considerable corporate earnings improvement in the year ahead having already been priced in, but rising input costs and the prospect of higher corporate tax rates in the US are clouding the outlook on this front. The tsunami wave of new Covid cases in India is also a concern. Oil prices have turned nearly 2% low today, with commentaries citing an expected decline in demand from India.

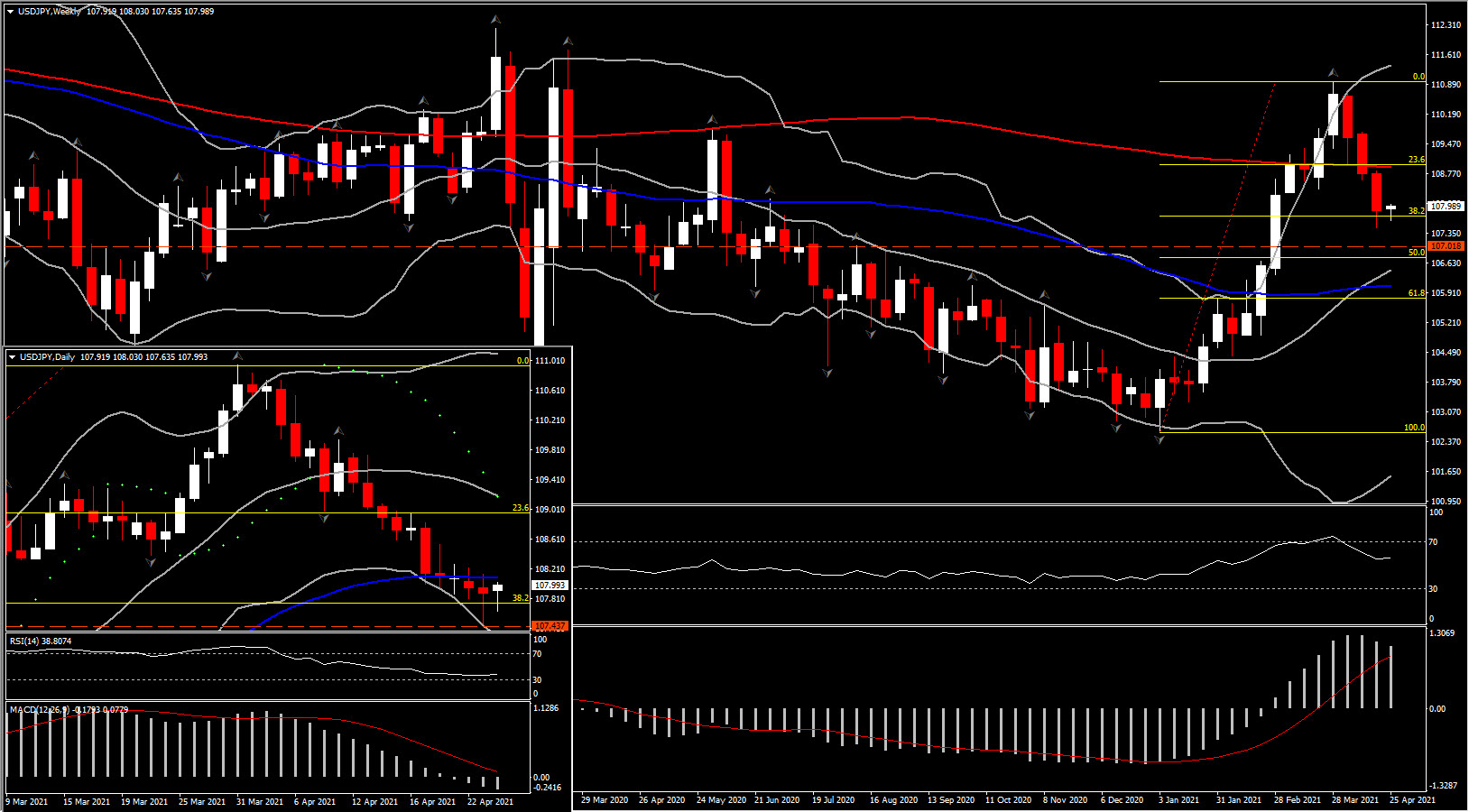

That said, Yen found ground on the US Dollar slump and USDJPY printed a low at 107.65, but remained above Friday’s near eight-week low at 107.47. The pair has been tracking the narrowing in the US 10-year yield advantage relative to the 10-year JGB yield, which has been in play for three weeks now. The solid demand that was seen at the 20-year US bond auction last week suggests that, for now, longer-dated yields are likely to remain without upside impetus, though we are still anticipating strong data over the coming months that will likely re-inspire bond markets to price in contingency risk that the Fed may be forced into withdrawing monetary stimulus sooner than it is currently signalling.

According to Reuters, many Japanese life insurers, major investors in global bonds, plan to increase their holdings of Yen bonds as their yields have recovered from lows while some of them are more cautious about foreign bonds.

As for USDJPY, the prevailing bias looks likely to remain to the downside for now, though the bigger picture remains bullish, anticipating a renewed phase of rising US yields in the months ahead.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.