Market News Today – USD grinds higher awaiting jobs data. USDIndex spiked to 90.20 yesterday back to 90.00 now. Equity markets edged out gains (USA500 +6 to 4208). AMC rallied 95% after Tuesday’s +22% after $250m investment. Asian markets higher, ASX200 at ATH, USOil over $69.00 following OPEC+ deal. Overnight Chinese Services PMI miss, AUD Retail Sales in line and Harker talked of “low rates for longer”, Beige Book “moderate pace of expansion”. Suga to hold snap election after Olympics, Biden progresses Infra talks with Republicans & offers incentives to boost vaccination rate, UK 75% of adults at least one vaccination. EUR 1.2186, JPY 109.80, GBP 1.4150. GOLD dipped from $1909 earlier to under $1895 now

This week – Heavy dose of global data – top of the shop is US NFP, Eurozone Retail Sales & GDP and monthly PMI data – The data could reveal the acceleration in annual inflation growth for major economies.

European Open – The June 10-year Bund future is little changed, as are Treasury futures, while in cash markets the US 10-year rate is now up 0.3 bp at 1.59%, after the paper pared earlier gains. DAX and FTSE 100 futures are up 0.2%, while U.S. futures are narrowly mixed, with overall trading still sluggish and muted as investors wait for another trigger, with the focus now on US payroll numbers tomorrow. Tapering musings seem to be getting louder and while ECB’s Lagarde stressed late on Wednesday that the central bank will maintain favourable financing conditions through the crisis, that would undoubtedly still be the case if monthly purchase volumes under PEPP were scaled back to the levels seen early in the year.

Today – EZ, UK and US Services and Composite Final PMIs, US ADP, Weekly Claims, ISM Services PMI, DoEs, ECB’s Elderson, BoE’s Bailey, Fed’s Bostic, Kaplan, Harker, Quarles

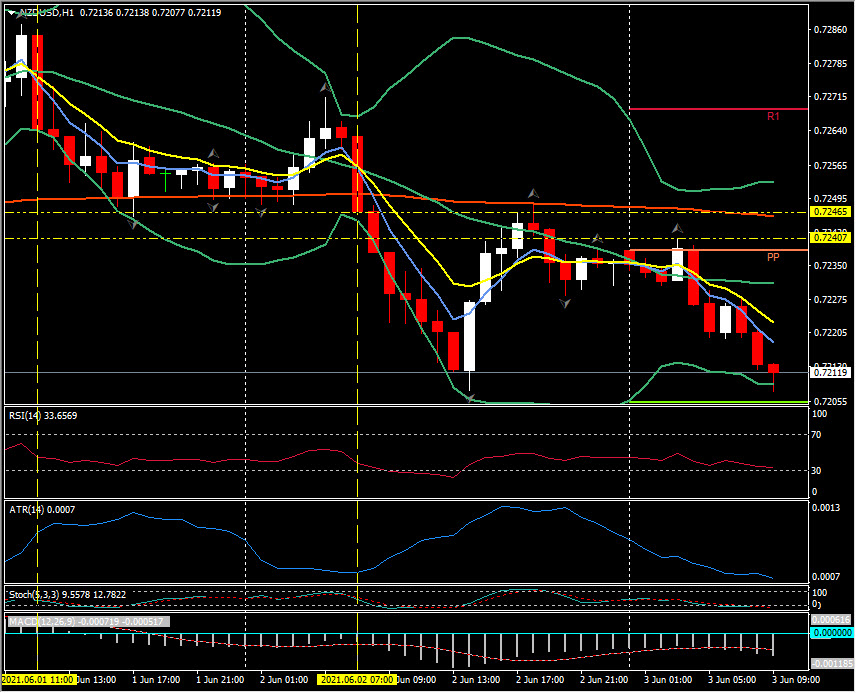

Biggest FX Mover @ (07:30 GMT) NZDUSD (-0.38%) has moved down to test yesterdays lows at 0.7205 (S1) earlier, (last Thursday was trading over 0.7300). faster MAs remain aligned lower, RSI 32.40 and filing heading to OS zone, MACD signal line and histogram falling again and have been below 0 line since Tuesday. Stochs. still moving lower and into OS zone. H1 ATR 0.0007, Daily ATR 0.0063.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.