Wall Street was narrowly mixed again overnight, as investors sat on their hands ahead of the upcoming June jobs report. Data on ISM manufacturing, jobless claims, and construction spending was ignored in favor of the more crucial employment numbers on the horizon.

Also yesterday, according to FT, the world’s leading economies have signed up to a plan to force multinational companies to pay a global minimum corporate tax rate of at least 15% following intense negotiations in Paris at the OECD. The historic agreement among 130 countries will ensure the largest companies, including Big Tech, pay at least $100bn a year more in taxes, with more of that money going to the countries where they do most of their business.

The USA500 did manage another record high, with the USA30 in the green too as value shares were favored. The USA100 was largely flat. Stock markets in Japan and Australia managed to move slightly higher, though, while China bourses sold off with some commentators suggesting that the conclusion of the centennial celebrations for the Communist Party meant increased risks for markets.

In Europe, core exchanges rose, with the UK100 adding 1.25%, and the GER30 rallying 0.47%. Comments from ECB’s Lagarde suggesting that the current cap on dividends and share buybacks for banks could be lifted at the end of September helped underpin sentiment. Also:

- Fed’s Harker (non-voter) backs tapering.

- ECB’s Weidmann backs symmetrical inflation target for the ECB.

Dovish comments from BoE’s Bailey, who stuck to the view that inflation will be transitory, added support, although they didn’t prevent Gilts from underperforming versus Bunds, with the former up 1.4 bps to 0.728%, and the latter 0.7 bps higher at -0.203%. Hopes that the impact of the rapidly spreading Delta variant won’t prevent the projected re-opening of holiday travel, while also keeping central banks in supportive mode, helped peripheral stock and bond markets.

Forex Market: USDIndex edged up to 92.60, and USDJPY is at 111.65, while the USOIL future is at $75.22per barrel. The Australian and NZ Dollars hold at Q4 2020 lows, while the EUR slipped to 1.1834 from 1.1888. Gold sustains gains at the 1779 area.

As Soc Gen accurately notes, US 2y rates are driving the Dollar. “The challenge for the FX market is that with no rate on the cards for over 12 months, expectations about what the Fed will do are bound to move around with each and every major economic statistic. All eyes, then, are on payroll data and if they come in strong, the dollar bears are going to get squeezed.”

Today’s Calendar – ECB’s Lagarde is scheduled to speak today, but likely to repeat the familiar line that the crisis is not over and support is still necessary. At the same time we will see US labor market data.

US nonfarm payrolls preview: nonfarm payrolls are expected to rise 550k in June following increases of 559k in May and 278k in April as there continues to be a big gap between the strength in the recovery and the record high in job openings against the relatively slow return of workers amid various headwinds. We’re also forecasting a 35k jump in factory jobs. The work-week should hold steady at 34.9 while hours worked picks up 0.4%. The unemployment rate is seen dipping to 5.6%. Average hourly earnings are projected rising 0.2% as minimum wage workers have been slow to come back. However, the y/y wage gain should surge to 3.5% from 2.0%, with a big boost from base effects.

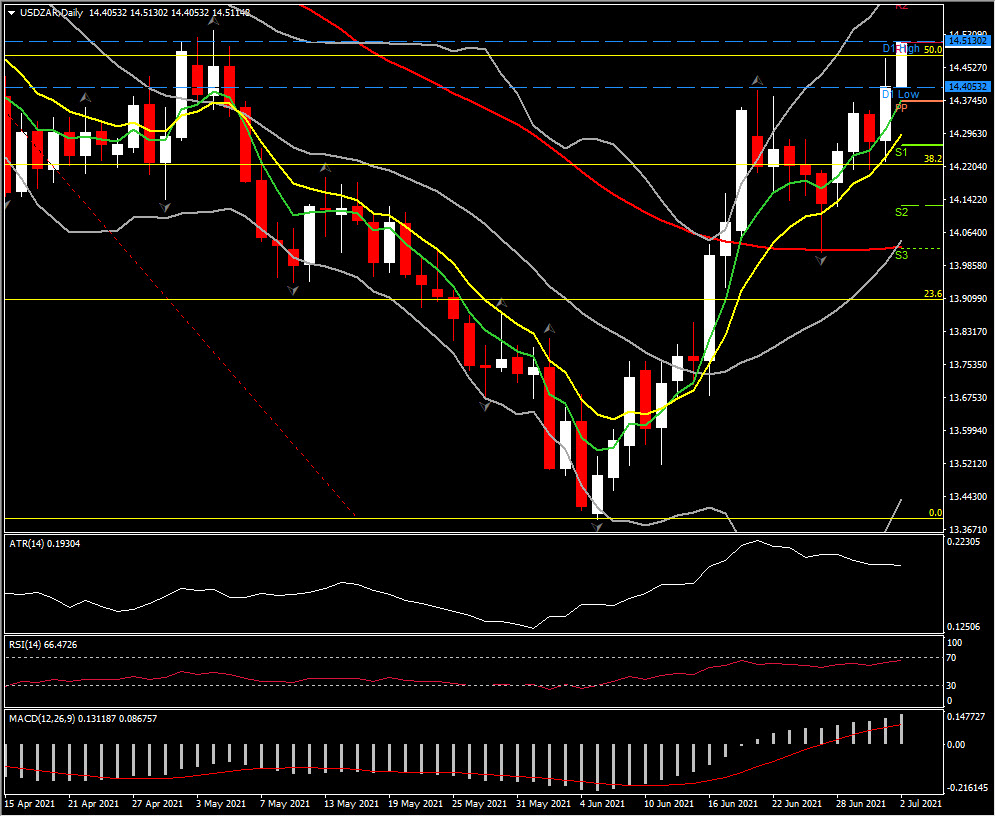

Significant FX Mover @ (06:30 GMT) USDZAR(+0.54%) extending highs for 2 days in a row, above the June high and the 50% retracement level since the February downleg. MACD lines and RSI are positively configured.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.