It was a jittery opening for US markets with Treasuries and stocks retreating from Friday’s gains. The 10- and 30-year yields are up 3.5 bps and 4.5 bps, respectively, at 1.496% and 2.072%. US equity futures are pointing to a lower opening with the USA30 off -3%, the USA500 -0.4% lower, and the USA100 down -0.57%. European stock markets have essentially moved sideways as yields nudged higher. China bourses will remain closed through to Thursday for the Golden Week holidays.

Fiscal policy uncertainties, and especially the debt limit and worries over default, are keeping buyers sidelined, ahead of key US jobs data later in the week. Concerns over Evergrande, where shares were halted, and China’s property market in general are weighing. Talk of stagflation is adding to the tensions. The demise in the viability of ‘perma QE’ is also in the mix, reflected by recent hawkish pivots at many central banks. These considerations have offset news that pharmaceutical company Merck’s experimental oral antiviral can significantly reduce hospitalisation and death risk for Covid cases. Massive US fiscal stimulus is also in the works.

Stagflation fears continue to linger and hopes that OPEC+ will help to ease the global energy squeeze by agreeing an additional boost to output at today’s meeting seem to be fading.

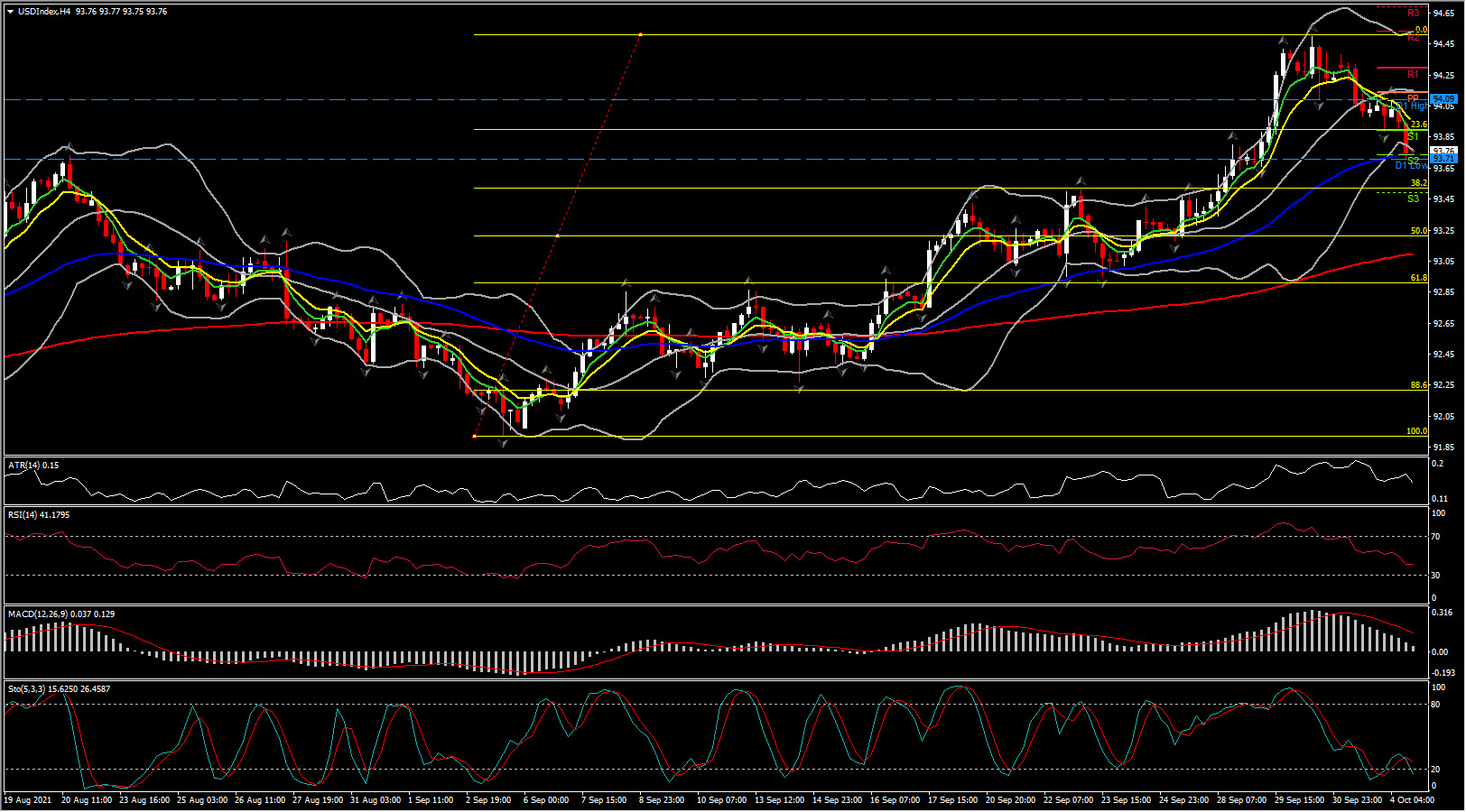

The US Dollar has drifted lower against most currencies today. The 10-year Treasury yield remains a driving force, and while lifting back towards 1.50% from 10-day lows near 1.46%, remained comfortably below last week’s highs near 1.55%. The USDindex posted its lowest level seen since last Wednesday, at 93.71, extending the correction from the 1-year high that was seen on Thursday at 94.50.

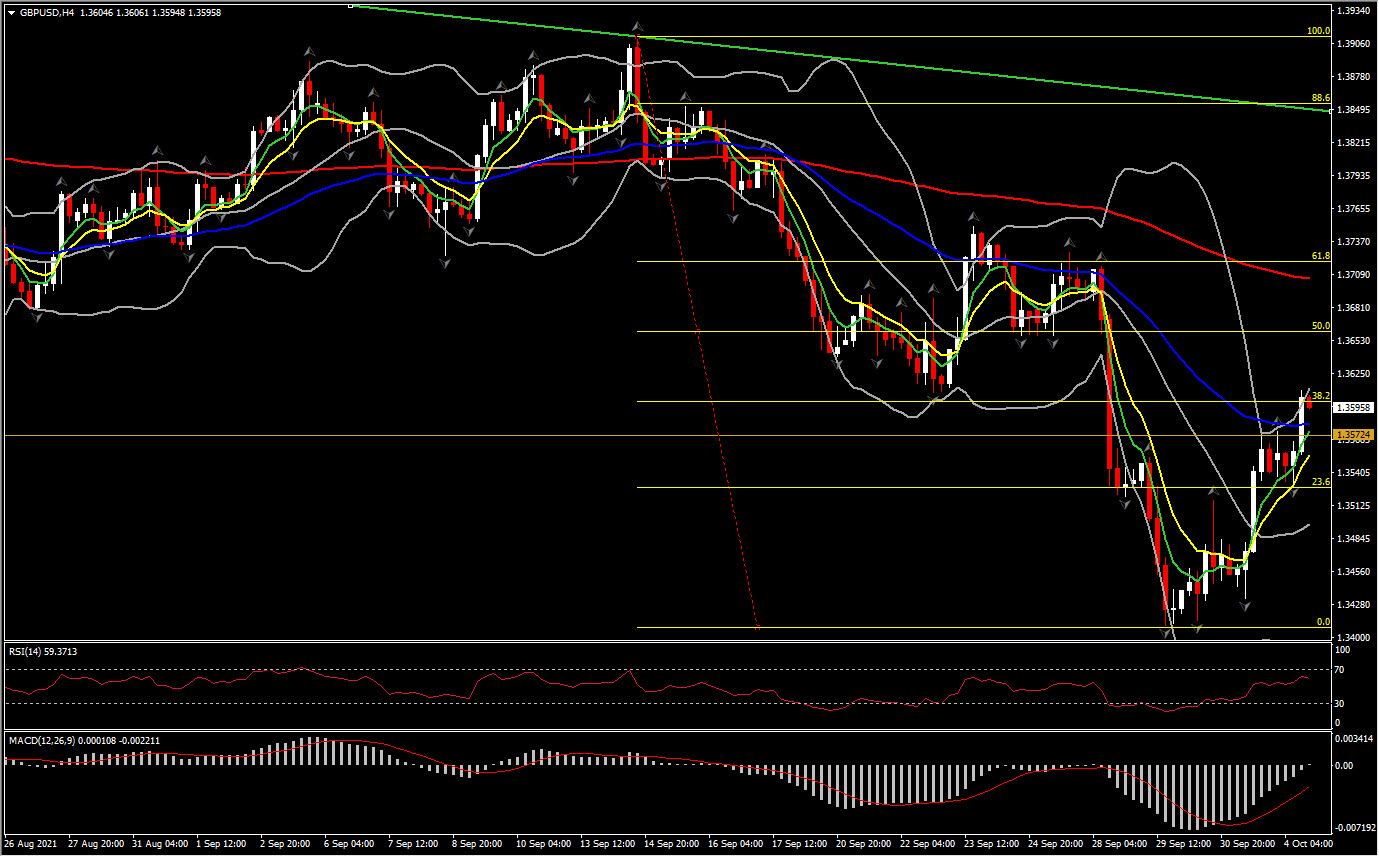

EURUSD concurrently extended its rebound high to 1.1619 after last week printing a 14-month low at 1.1562. Cable has lifted to a 1-week high at 1.3610. Dollar weakness mostly explains the move, while the Pound has seen a modicum of gains versus the Euro and other currencies today after underperforming last week. Recent bouts of risk-aversion in global markets weighed on the UK currency, being a currency of an open, deficit economy.

At the same time, the UK economy is slowing somewhat, while price pressures are rising. BoE Governor Bailey warned last week of “hard yards” ahead” due to persisting supply chain disruptions and the sharp rise in energy prices in the UK. Bailey said that interest rates will have to rise over the medium term to tame inflationary pressures but stressed that the economy is currently too weak to withstand such a move. It is widely anticipated that prevailing sterling gains will sustain.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.