- Trade is likely to be thinned this week by Thanksgiving in the United States, but the virus’ resurgence has traders once again monitoring COVID-19 cases and governments’ responses.

- USDIndex at 16-month highs above 96.00.

- Yields: 10-year Treasury rate is up 1.4 bp at 1.57%, while across the Asia Pacific region bonds are mostly higher, despite the prospect of a rate hike from the RBNZ. The 2s, 5s, and 7s also richened measurably ahead of the upcoming auctions and as hawkish comments from Fed VC Clarida and Governor Waller saw gains pared, but the move was short lived.

- China’s PBOC kept the loan prime rate unchanged once again and Covid jitters in Europe weighed on sentiment.

- Equities: Stock markets have traded narrowly mixed, with Topix and JPN225 down -0.08% and up 0.09% respectively. The Hang Seng lost -0.7%, while the CSI 300 lifted 0.5%. US stocks stalled due to mix of earnings news, albeit from record highs, with the USA30 tumbling -0.75%, hitting 35600 lows. The USA500 stabilised at 4713 while the USA100 rallied to 16632.

- USOil dipped to $74.06 lows as countries continue to debate the release of strategic reserves. Reuters report that: “Japanese officials are working on ways to get around restrictions on releasing national reserves of crude oil in tandem with other major economies to dampen prices”.

- Gold down to 1838.55 (S1).

- FX markets – Yen sell off continues with the CHF a notable exception. EUR and GBP weakened. EURUSD at 1.1262, GBPUSD steady below PP at 1.3426.

European Market Update: The 10-year Bund future is down -23 ticks, slightly underperforming versus Treasury futures, while in cash markets the US 10-year rate has lifted 1.2 bp to 1.56%. Stock futures are mostly higher, with the GER30 and UK100 posting gains of 0.1% and 0.2% respectively and US futures slightly outperforming.

The Covid situation in some parts of Europe is escalating again, mainly in those areas with a strong anti-vaccine movement and a low vaccine uptake and protests against nationwide curbs dominated the headlines over the weekend. With little on the data calendar today, Covid developments will likely remain in focus, as they will also play a part in upcoming central bank decisions.

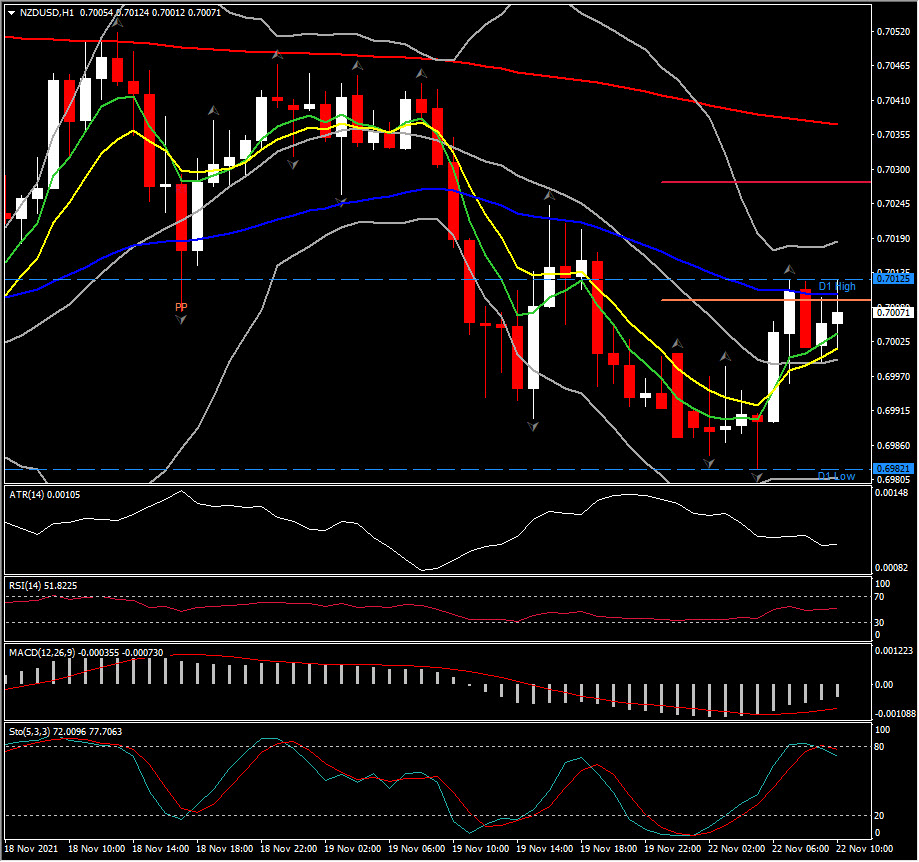

Biggest FX Mover @ (07:30 GMT) NZDUSD (+0.74%) retested the 0.7000 area. Faster MAs are currently aligned on the right hand side indicating consolidation, MACD lines hold negative, while RSI is at 51 and Stochastic started falling, suggesting lack of further boost for now. H1 ATR 0.00105, Daily ATR 0.00610.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.