Omicron remains in focus and warnings that it will leave current vaccines far less effective and that it will take time to modify and produce new ones has seen markets adjusting growth forecasts and central bank projections.

- USD (USDIndex 96.00 up from 95.92 low) saw a fresh wave of risk aversion as Treasuries sold off, but cautiously with only a modest back up in yields, & Stocks bounced significantly with the USA100 jumping over 2% intraday with IT a big winner. It closed with a 1.88% gain, with the USA500 1.3% firmer, and the USA30 up 0.68%.

- Wall Street stocks closed higher as investors were hopeful that the Omicron coronavirus variant would not lead to lockdowns after reassurance from US President Joe Biden.

- Moderna’s CEO told the FT that existing vaccines will be less effective and that it may take months before modified vaccines are available at scale. #Moderna +12.73% yesterday.

- US Yields 10- and 30-year rates were up just over 3 bps to 1.51% and 1.859%, respectively, with the 2-year 1bps higher at 0.508% The 10-year is currently corrected -3.9 bp to 1.46%, but it is still in negative territory, at -1.05% on Tuesday, keeping gold’s opportunity cost low.

- Equities – Topix and Nikkei are down -1.0% and -1.6% respectively, Hang Seng lost -2.3%, the CSI 300 -0.6%, while the ASX outperformed with a modest gain of 0.2%.

- USOil – down by 2%, drifted to $66.73 – after FT cast doubt on the efficacy of COVID-19 vaccines against the Omicron – expectations are growing that OPEC+, will put on hold plans to add 400,000 barrels per day (bpd) of supply in January.

- Gold spiked to $1795 – World Health Organization said on Monday carried a very high risk of infection surges.

- #TWTR was UP 12% pre-market on news Dorsey was leaving as CEO – it closed DOWN 2.74%. The USA100 rose+1.88%.

- FX markets – Yen rallied (a new flight to safety), Aussie and kiwi slide. USDJPY at 112.94, EURUSD now 1.1326 & Cable steadied to 1.3300-1.3330.

European Open – The December 10-year Bund future is up 46 ticks, Treasury futures are outperforming and in cash markets the US 10-year rate has corrected -3.9 bp to 1.46% amid a fresh wave of risk aversion. DAX and FTSE 100 futures are down -1.5% and -1.1% respectively, while a -1.1% drop in the Dow Jones is leading US futures lower. In FX markets both EUR and GBP gained against the Dollar. EGB yields had moved higher against the background of improving risk appetite and a jump in German inflation yesterday, but while Eurozone HICP today is likely to exceed forecasts, central bankers have already been out in force to play down the importance of the number for the central bank outlook and rate expectations. Virus developments will also help to take the sting out of the number.

Today – German labour market data, EU Inflation, Canadian GDP and US Consumer confidence are due today. Fed Chair Jerome Powell and Treasury Secretary Janet Yellen are due to testify before the US Senate Banking Committee at 15:00 GMT.

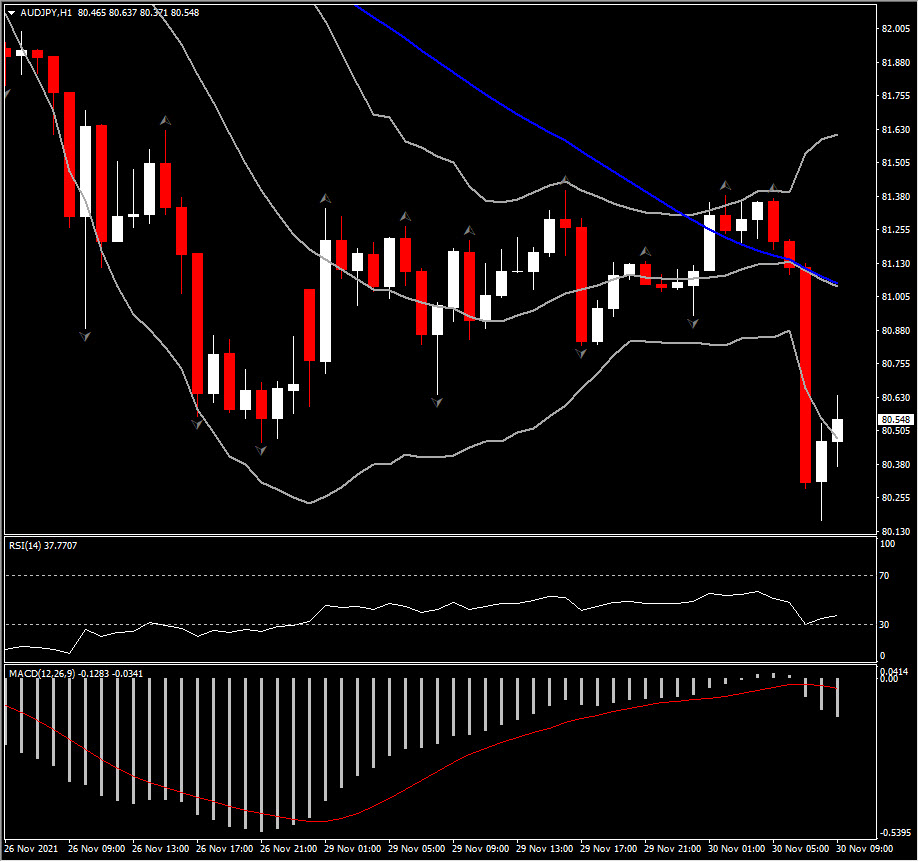

Biggest FX Mover @ (07:30 GMT) AUDJPY (-0.68%) Risk-sensitive currencies slid and safe havens gained. AUDJPY dropped to 80 lows (S2). Currently MAs point rightwards, MACD signal line & histogram below 0, RSI rising above 30 but Stochastic OS. Hence a mixed picture intraday.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.