Powell reiterates Hawkishness, First case of Omicron confirmed in US – Stocks tank again under key technical levels, Yields slip again, USD mixed. Erdogan sacks Fin Min – TRY new all-time lows, Apple iPhone 13 demand weakens, GSK anti-viral drug remains active vs. Omicron

- USD (USDIndex 96.08) rotates through 96.00 due to lack of firm data regarding Omicron, markets reamin on edge. Stocks fell significantly with USA100 down over -1.83% USA500 -1.18% (-54pts) 4513 (opened the day +1.1%) and broke 50-day MA first time since October 14 & USA30 off 461 pts and under 200-day MA first time since July 13 2020.

- US Yields 10-year rates were down over 7 bps to 1.40% before recovering to 1.434% now.

- Asian Markets – Asian markets have traded mixed. Topix and Nikkei are down -0.5% and -0.7% respectively. The ASX lost -0.1%, but Hang Seng and CSI 300 are up 0.2% and 0.3%. Shenzen and Shanghai Comp are slightly lower though as officials seem eager to close a loophole used by tech firms to list abroad.

- USOil – continues under pressure, down to $64.50 yesterday – recovered to test $66.35 today – awaiting OPEC+ meeting later.

- Gold Up day yesterday but remains pressured testing $1775 now

- FX markets – Yen rallied USDJPY dipped to 112.70, back to 113.31 now, EURUSD now 1.1312 & Cable pressured 1.3192 low yesterday – 1.3275 now.

European Open – The 10-year Bund future is up 30 ticks, outperforming versus Treasuries, which remain pressured by the hawkish turn at the Fed. The 10-year Treasury yield has lifted 3.0 bp overnight, but at 1.43% remains far below the levels seen ahead of the Omicron scare, which the WHO seemed to try and play down somewhat. DAX and FTSE 100 down -1.1% and -0.9% respectively in catch up trade with the slide on Wall Street yesterday, while US futures have found a footing and are posting gains of around 0.6-0.8%.

Today – EZ Unemployment Rate, US Weekly Claims, Fed’s Bostic, Quarles, Daly, ECB’s Panetta, JMMC/OPEC+ meetings.

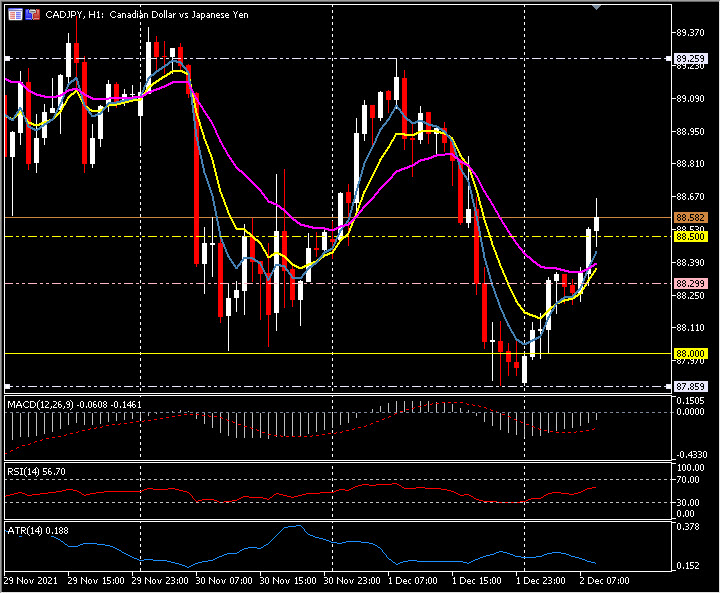

Biggest FX Mover @ (07:30 GMT) CADJPY (+0.77%) Risk-sensitive currencies remain volatile, from a slide to 87.85 yesterday, today a rally to 88.60. Currently MAs aligned higher, MACD signal line & histogram under 0 but rising, RSI 56 & rising, OB. H1 ATR 0.188, Daily 0.98.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.