- USD (USDIndex firmed at 96.25) as caution dominated. Profit taking knocked stocks a little lower after recent gains as concerns over Omicron and the renewed restrictions in the UK and in other areas weighed on the more optimistic growth outlooks into 2022.

- Asian stock markets have sold off across the board, with Topix and Nikkei currently down -0.8% and -1.0% respectively.

- China Evergrande Group and Kaisa Group Holdings Ltd officially defaulted on their dollar debt.

- China’s central bank meanwhile took further steps to limit the Yuan’s strength by setting the weakest reference rate relative to estimates since 2018, – according to Bloomberg. The bank already raised the foreign currency reserve requirement yesterday for a second time this year.

- German HICP inflation was confirmed at 6.0% y/y, the national CPI rate at 5.2% y/y. The final readings for November were no surprise and the breakdown confirmed that higher energy prices were a key factor.

- UK GDP weaker than expected in November – More arguments then for the BoE to sit out yet another meeting next week and push the rate hike debate into 2022.

- US Yields: 10-year Treasury yield is up 0.5 bp at 1.50% – Treasury yields richened, in part on the risk off in stocks and on short covering as some of the recent selling pressures were overdone

- USOil – dip to $70.16 – biggest weekly gain since late August! Brent & WTI both on >6% rise this week. – RISK: China’s domestic air traffic recovery faltering due to zero-COVID policy, that has led to tighter travel rules in Beijing and weaker consumer confidence after repeated small outbreaks.

- FX markets – US Dollar firmed at 96.25, Chinese Yuan got a boost, EURUSD settled below 1.1300 on ECB’s debate news, Cable at 1.3214. Yen generally steady to lower against most currencies.

European Open – The March 10-year Bund future is down -15 ticks, slightly underperforming versus US futures, while in cash markets the 10-year Treasury yield is up 0.5 bp at 1.50%, after the paper erased overnight gains. GER30 and UK100 futures are down -0.5% and -0.4% respectively, after a broad sell off across Asian markets.

In Europe, expectations for a BoE rate hike have been pushed back as the UK ramps up virus restrictions. The ECB is set to confirm the end of PEPP, but seems to be still debating if and how to soften the blow with a strengthened APP program. In any case, net asset purchases will continue even when the emergency PEPP program has ended.

Today – Data releases today focus on ECB’s Lagarde speech, US inflation and Michigan index.

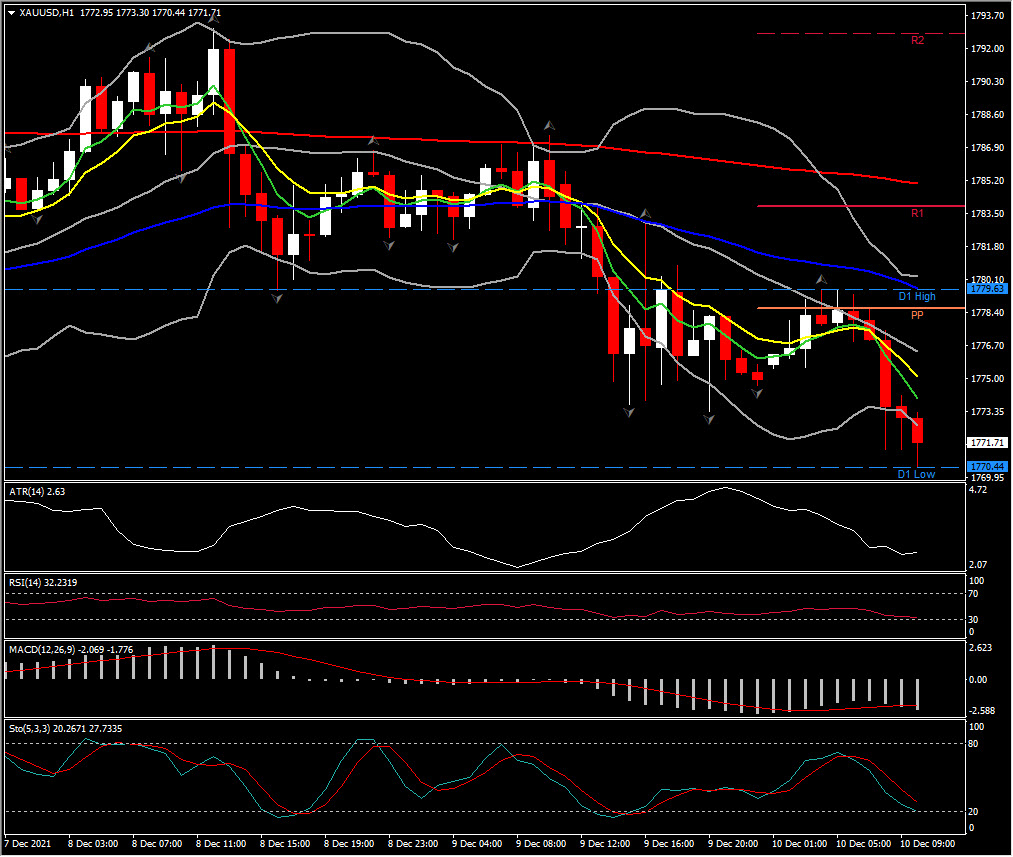

Biggest FX Mover @ (07:30 GMT) XAUUSD (-0.20%)Currently MAs are aligned lower with the asset below PP. MACD signal line & histogram are moving southwards below 0 and RSI is retesting OS barrier, with Stochastic declines suggesting further pressure.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.