The RBA did not adjust its monetary policy settings in January. The cash rate target, as well as the Australian Government Securities (AGS) 3-year bond, remained unchanged at 10 basis points, while it was decided that the A$275 billion bond purchase program will end after February 10. The RBA was in line with December’s largest retail decline since April 2020 of -4.4% from a 7.3% gain in November as a result of an outbreak of the omicron variant causing consumers to slow down their spending on goods and services.

Although the RBA flagged the possibility of a rate hike this year, RBA Governor Lowe highlighted that the decision to end bond buying isn’t a signal that rate hikes will follow soon, stressing that the bank has more time than others as inflation concerns are not quite as pressing. Still, Lowe stressed that “there are a lot of uncertainties both on the supply side and the labour market dynamics and because inflation’s not that high at the moment we can wait to see how those uncertainties resolve”. A rate hike this year is a “plausible” scenario, but not the only way. If uncertainties “resolve in one way, then we will be raising rates, if they resolve in another way, it is still quite plausible that the first increase in interest rates will be a year or longer away.”

So the bank is not quite ready to commit to rate hikes yet, although that the turning point on policy has been reached is clear and already confirmed by the end to bond buying.

Reserve Bank of Australia Governor Philip Lowe said that they will patiently monitor factors affecting inflation in the country, such as price pressures, consumption, and wages. He said that based on the evidence they had, it was too early to conclude that inflation was sustained within the target range. “In terms of underlying inflation, we have just reached the midpoint of our target range for the first time in more than seven years,” he said. The governor noted that the central bank is committed to doing what is necessary to achieve its inflation target. “We don’t want to see inflation too low or too high,” he concluded. He stressed that Australia’s inflation remained much lower than the US, UK and New Zealand, so the RBA would not need to move its policy along with other central banks.

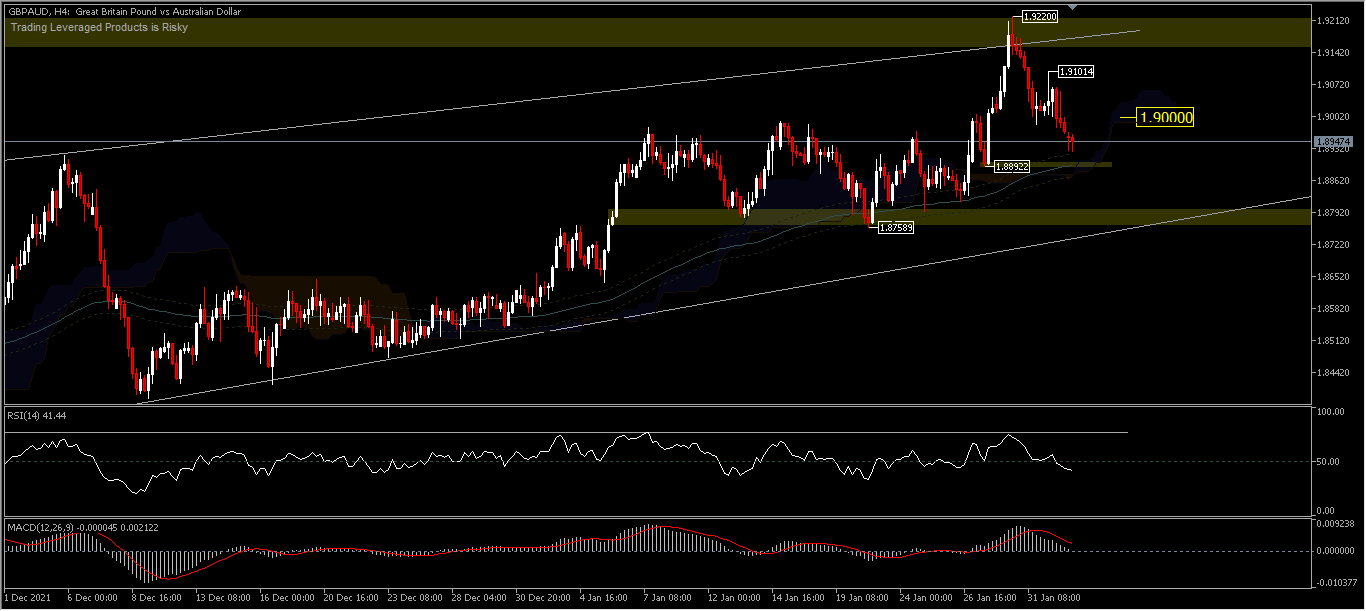

The Sterling exchange rate against the Australian Dollar has rebounded to an 18-month high and is currently holding below the 1.9000 level after the RBA effectively scrapped market speculation by saying it will patiently watch Australia’s wage package growth and other inflation-related developments, before raising interest rates.

GBPAUD, H4 – The pair formed a double top at a high of 1.9220 last week, and since then the price has corrected -1.5% to date. A move below the support at 1.8758 would confirm the start of a correction wave to the downside. As long as the support level at 1.8758 holds, the movement tends to the upside according to market expectations of a possible hawkish monetary policy change at the BoE meeting on Thursday (03/02). Any move to the upside would be limited by the 1.9220 resistance and a break of this level would extend the rally from the 1.8125 rebound, targeting 1.9533 (61.8% FR from the drawdown to the 2.0844 peak and the 1.7414 valley.) For the record, double_top positions are located at the 50.0% retracement.

AUDJPY, H4

Meanwhile, in Japan December unemployment figures fell back to 2.7% from 2.8% in November. This indicated a recovery from the impact of the latest round of omicron outbreaks. The revised January manufacturing PMI rose from an initial reading of 54.6 to 55.4 and above the previous month’s 54.3. This was the strongest growth in factory activity since February 2014. With the movements of the RBA and the improvement in global market sentiment this week, the AUDJPY pair has moved up from the low zone of the year to make a new weekly high near the 82.00 key resistance, which if it can break up there will be the next important resistance at the MA200 line at 82.40. Conversely, if the price moves back down there will be important support at the MA50 line at 81.40 and the next support at the original low at 80.40.

Click here to view the economic calendar

Ady Phangestu & Chayut Vachirathanakit

Market Analyst – HF Educational Office – Indonesia & Thailand

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.