Stocks stabilised and indexes came up from yesterday’s lows, as markets digest the still fluid developments in Ukraine and the standoff between the West and Russia. Haven demand eased and yields backed up. President Biden announced sanctions on Russia, including financial restrictions. Earlier Germany halted Nord Stream 2. UK will stop Russia selling sovereign debt in London. The RBNZ lifted its policy rate by 25 bp to 1.00%, adding to signs that central banks are moving out of crisis mode and are set on policy normalisation. Governor Bowman opened the door for a 50 bp liftoff next month. Gold below $1900, Oil settled at $90.50. Treasury yields cheapened with the front end underperforming on worries over aggressive rate hikes to help contain inflation.

- USD down (USDIndex 95.11) as risk appetite has stabilised.

- US Yields 10-year yield richened to 1.844% overnight before climbing to 1.958% then settling at 1.925%.

- Equities – GER30 and UK100 futures are up 0.6% and 0.1% respectively, while a 0.7% rise in the USA100 is leading US futures higher.

- USOil – Steady at $90.50 as neither sanction appears as harsh as it could have been.

- Gold – dipped as haven demand ebbed – below $1900.

- Bitcoin broke higher to trade at $38,388.

- FX markets – NZDUSD jumped to 0.6776, EURUSD at 1.1340, USDJPY steady at 115.00. Cable breaches 1.3600.

European Open – German consumer confidence unexpectedly dropped to -8.1 in the advance reading for March. The March 10-year Bund future is down -4 ticks, Treasury futures are outperforming slightly, although the German 30-year future also seems to be benefiting from the prospect of reduced ECB support as surveys signal a swift rebound from the latest virus wave, but also mounting inflation pressures. Risk appetite has stabilised somewhat, although markets will keep a wary eye on Ukraine and the standoff between the West and Russia. For now though the focus seems back on central banks and the Fed’s tightening schedule.

Today – Today’s local calendar includes the final Eurozone HICP number, which will highlight once again that inflation is staying higher for much longer than initially expected. That in turn is putting pressure on the ECB to rein in stimulus. The UK has the latest retailing survey, which should register the easing of virus restrictions.

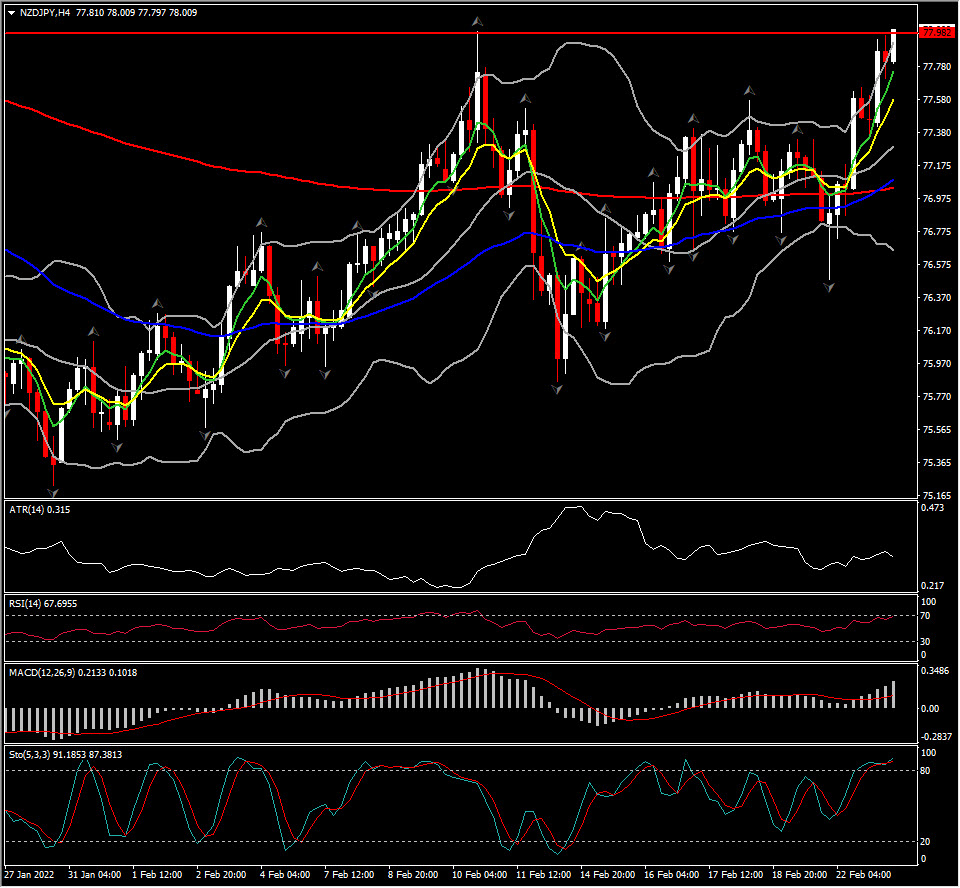

Biggest FX Mover @ (07:30 GMT) NZDJPY (+0.74%) Spiked to 78 highs earlier. MAs now aligned higher, MACD signal line & histogram significantly above 0 line, RSI 72.66 & rising. H1 ATR 0.155, Daily ATR 0.781.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.