Risk aversion has hit markets hard amid reports of a full blown attack by Russia on Ukraine, which has also lifted Brent clearly above the $100 per barrel mark. Ukraine declared a 30-day state of emergency, called up reservists and urged its citizens to leave Russia. More cyber attacks on government websites and banks and disinformation campaigns were seen as a prelude to war. Also, US officials said diplomacy with Russia was dead for now. That added to the gloom. Russia suspended movement of commercial vessels in Azov Sea. Von Der Leyen – EU Planning `Massive Sanctions’ on Russia.

Treasuries rallied and stock markets across Asia sold off as the world watches Ukraine. The US Treasury rate is down -12.3 bp at 1.868%, while the Nikkei has lost -1.8%, the ASX nearly 3% and Hang Seng and CSI 300 -3.1% and -2.3% respectively. Brent is trading at $102.19, the front end WTI future at $97.07 per barrel. Gold below $1949. USDRUB at 80.99.

- USD spikes (USDIndex 96.75)

- US Yields 10-year yield down to 1.868%.

- Equities – GER30 and UK100 futures are down more than 3.5% and 2% respectively, while USA500 was down 2.3% and USA100 fell 2.8%, putting the USDIndex on track toward confirming it is in a bear market.

- Reuters: “Closing down at least 20% from its Nov. 19 record high close of 16,057.437 points would confirm the Nasdaq has been in a bear market, according to a widely used definition. That would mark its first bear market since 2020, when the coronavirus outbreak crushed global financial markets.”

- USOil – spiked to $96.46, & UKOIL passed $100 a barrel for the first time since 2014, adding to inflation worries.

- Gold – rallied over 2% as haven demand ebbed – below $1900.

- Bitcoin below $35,000 as, sell-off spread to cryptocurrency markets as well.

- FX markets – Yen benefited, while the Euro and to a lesser extent Sterling struggled. EURUSD at 1.1245, USDJPY drifted to 114.39, Cable breached 1.3485.

European Open – The March 10-year Bund future has gained 182 ticks, outperforming versus US futures, which are up 119 ticks, while in cash markets the US Treasury yield has lifted off overnight lows, but is still down -10.9 bp on the day at 1.882%. Europe in particular is seen as vulnerable to the escalation of the situation because it could also potentially affect energy supplies, although a German economic institute yesterday suggested Germany could get through the winter even if Russia totally cuts off gas supplies. Meanwhile more sanctions on Russia’s economy are underway and for now the situation remains fluid, which will keep markets in defensive mode and heading for safety.

Today – Today’s data calendar includes US GDP, Jobless claims, PCE and speeches from ECB members and Fed Members.

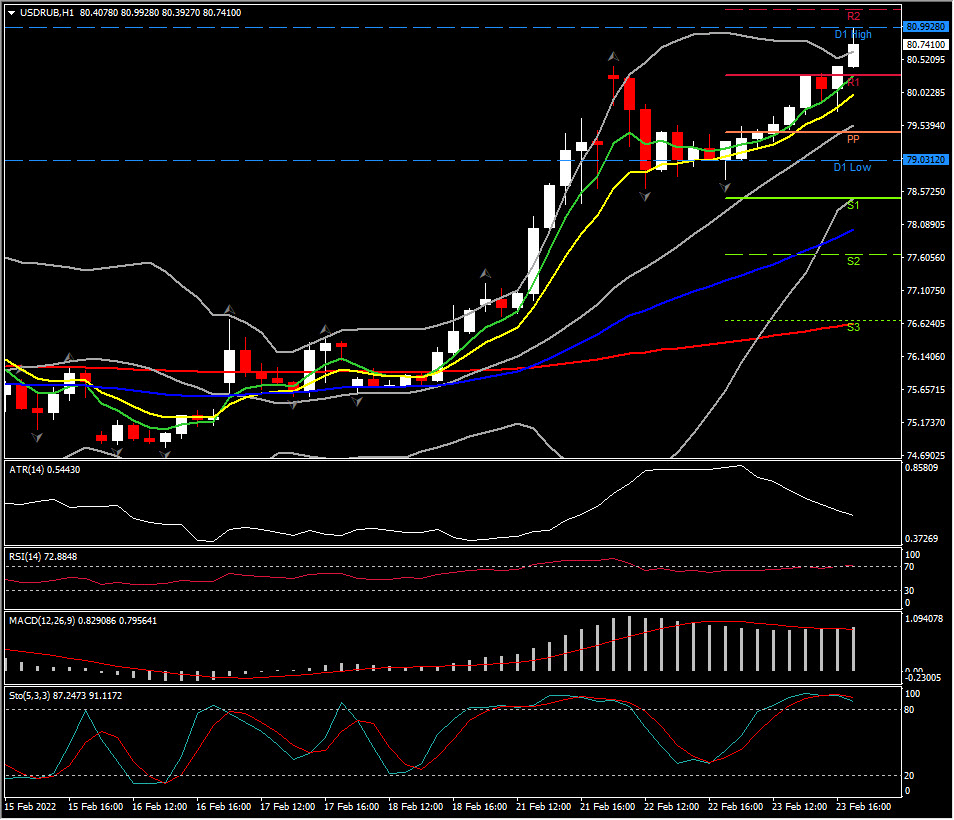

Biggest FX Mover @ (07:30 GMT) USDRUB (+6.42%) Spiked to 80.99 high. MAs now aligned higher, MACD signal line & histogram significantly above 0 line, RSI 72.88 & rising. H1 ATR 0.54430, Daily ATR 1.32211.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.