Yields stabilized lower, USD cooled significantly and Stocks bounced back. BOC added 50 bp to their base rate and warned of more to come. USDCAD sank from 1.2675 down to sub 1.2500. USDJPY hit a 20-year high over 126.00. US PPI lifted to all-time highs (11.2%) following 40-yr highs for CPI (8.5%) on Tuesday. All 13 measures of UK Inflation were higher than expected with CPI at 30-yr highs (7.0%) and a strong CORE (ex. Fuel & Food) at 5.7%, RPI 9.0% (important for wage settlements) and PPI 19.2%.

- Stocks higher (NASDAQ +2.0%) Asia markets stronger too (Nikkei +1.18%) & UK & European FUTS also higher

- Yields rally cooled further, 10-yr closed at 2.69% & now at 2.712%.

- USDIndex cooled from 100.50 highs & trades 99.60 now.

- Equities – USA500 +49 (+1.12%) at 4446. – US500 FUTS 4452. Delta Airlines (+6.21%), AAL (+10.62%). JPM (-3.22%) a miss for Trading volumes. Big Tech bounced (AMZN +3.15%)

- Oil & Gold continued to recover and hold over $103 & $1975 respectively.

- Bitcoin recovered from 39k zone on Tuesday to 41k now.

- FX markets – EURUSD recovered from 1.0808 lows (5-wk+ lows) to now 1.0915. USDJPY cooled from 126.30 20-yr high to trade at 125.40 and Cable recovered from 1.2972 lows to 1.3140 now.

Biden announced an additional $800 million in military assistance to Ukraine, (brings total to 2.5bn). Xi says sticking to tough COVID curbs will bring victory. Markets not convinced. PBOC rate cut imminent? Japan Fin Min. says country has not emerged from deflation, & 76% of Japanese business worried about the weak YEN damaging the economy. Finland & Sweden on brink of NATO membership. Sri Lanka about to default on debt, first of many low income nations?

Overnight – More peak inflation news ?? AUD job growth missed (17.9k vs 30.0k & 77.4k last time) & Unemployment rose (4.0% vs 3.9% & 3.9%). CHF PPI missed and UK House Inflation also slipped.

ECB Preview – Record high inflation and hawkish comments from some council members have left markets positioned for at least one rate hike from the ECB later in the year. However, with no sign that the war in Ukraine will be over any time soon and the sanctions against Russia already starting to cloud over the growth outlook, we suspect that chief economist Lane will want to keep a lid on tightening expectations today. Lane already warned against an “overreaction” to the surge in inflation and that the initial inflationary pressure from a supply shock “should decline over time”. He also highlighted the “significant risks to growth” from the war in Ukraine and the sanctions against Russia, while saying that “the best way that monetary policy can navigate this uncertainty is to emphasize the principles of optionality, gradualism and flexibility“. Lane is also keeping a close eye on spreads as the end of the PEPP program last month has kept peripheral vulnerable to bouts of risk aversion and even suggested that the PEPP program could be revived if necessary. Judging by ECB data released yesterday, the ECB has already blown much of the monthly APP purchases over the first two weeks of the month, clearly also in an attempt to keep a lid on yields and Lane will likely be arguing against an overly hawkish signal today that would further fuel rate hike speculation. That means the event risk is a more balanced statement than markets currently expect. – Action Economics

Today – US Weekly Claims, Retail Sales, Business Inventories & UoM Sentiment, ECB & CBRT Policy Announcements, ECB’s Lagarde, Fed’s Harker & Mester, Earnings from Morgan Stanley, Goldman Sachs and UnitedHealth.

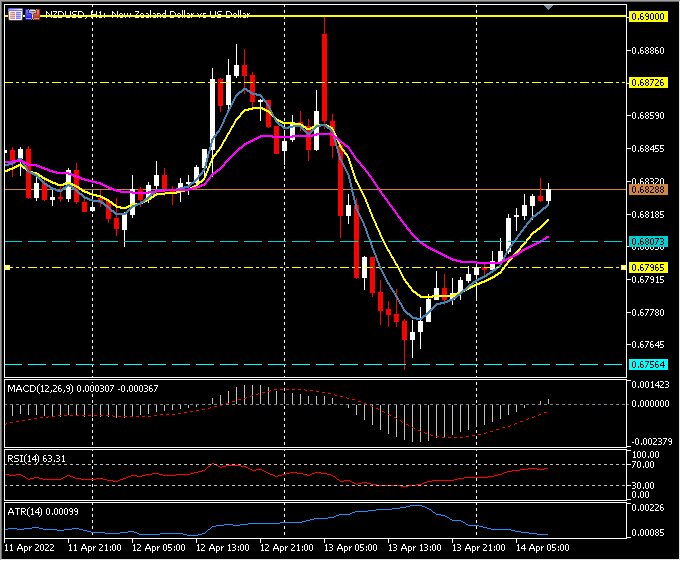

Biggest FX Mover @ (07:30 GMT) NZDUSD (+0.50%) Recovered from 0.6756 lows following RBNZ announcement, to close at 0.6796, testing 0.6830 now. Next resistance 0.6850 & 0.6875. MAs aligned higher, MACD signal line & histogram moving higher & over 0, RSI 64 & rising, H1 ATR 0.00099, Daily ATR 0.00703.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.