")

Risk appetite surged as optimism over earnings more than overshadowed concerns over the 8% pop in the y/y GDP price gauge and the -1.4% print on Q1 GDP. The contraction in growth was seen as a one-off, however, due to trade disruptions limiting supply alongside a surge in demand following the pandemic, with inventory drawdowns contributing negatively too. Stock markets remained supported overnight, with hopes of support measures in China helping to underpin sentiment, after China vowed to underpin the health of so-called platform firms. Meanwhile, the pick-up in core PCE inflation to a 5.2% y/y pace from 5.0% y/y was also seen on the light side and hence supported notions that prices may be topping out.

European Fixed Income Outlook: Bund yields are down -2.5 bp at 0.87% in early trade, with Eurozone bonds paring some of yesterday’s losses and yields coming down as the unexpected stagnation in French GDP at the start of the year highlighted that there are still reasons for the ECB to remain cautious even as inflation is going through the roof. German import price inflation jumped to 31.2% y/y in March, from 26.3% y/y in the previous month.

- Yields are coming down from yesterday’s highs. The 2-year yield rose over 5 bps to test 2.68% and the 10-year challenged 2.90% before drifting back to 2.63% and 2.85%, respectively.

- Stocks – GER40 and UK100 futures are up around 1.0%, USA100 soared 3.06% on the day, with the USA500 2.47% higher, while the USA30 climbed 1.85%, but all off of late peaks. Japan is closed for a holiday, the ASX up 1.1% at the close.

- Earnings – Meta shares surge after Facebook ekes out user growth; Qualcomm rises after it forecasts upbeat revenue; Apple Inc, the world’s most valuable company, and e-commerce giant Amazon.com Inc rallied more than 4% ahead of their quarterly reports later in the day.

- USDIndex lost some of its recent gains, currently at 103.15.

- Oil at $106.42. Oil prices meanwhile moved higher as overall confidence improved and fears over China’s Covid measures eased somewhat.

- Gold back above $1900.

- FX markets – EUR and Sterling also found some buyers, but while EURUSD and Cable are up from yesterday’s lows, they are still looking pretty weak at currently 1.0548 and 1.2530 respectively. USDJPY still held above the 130.

Today – German and Eurozone GDP are still to come and Eurozone inflation data are also due, while in the US session eyes are on PCE and Canadian GDP. Exxon and Chevron earnings on tap.

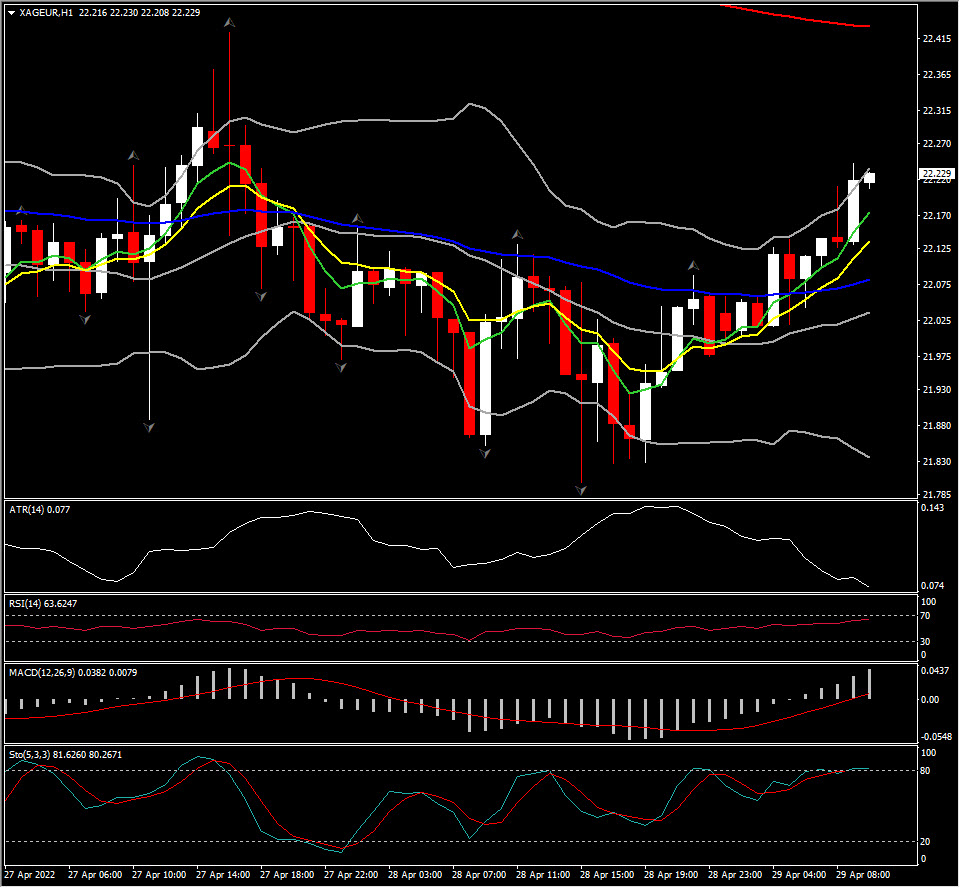

Biggest FX Mover @ (07:30 GMT) XAGEUR (+1.27%) breached 22.20. MAs pointing higher, MACD signal line & histogram turned positive, RSI at 62, all signalling further boost in the near term. H1 ATR 0.077, Daily ATR 0.509.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.