USD continues to hold onto recent gains, Stocks crashed (NASDAQ -4.17% Friday to close a miserable April and register its biggest daily loss since September and a weekly loss of -3.9%), Asian markets weaker (many closed due to Eid holidays) and European FUTS down over 1.5%. (UK closed today). Yields jumped higher and VIX soared over 7% to 31.30. Oil & Gold both rallied and then gave up all their gains. Weekend data – Chinese Manu & Services PMI’s (47.4 vs 49.5 & 41.9 vs. 48.4) the worst in 2 yrs as lockdowns grip the economy. Berkshire Hathaway invested over $51bn in Q1 inc. Chevron (over $21bn), Occidental ($10bn), HP ($4.2bn) & Alleghany ($11.6bn). US House speaker, Pelosi visited Ukraine promising support ‘until fight is done’.

- USDIndex cooled to under 103.00 on Friday, closed at 103.18, and is back to 103.45, now. April opened at 98.29, a near 5% gain.

- Equities – USA500 -155.57 (-3.63%) at 4131. – US500FUTS at 4145 now. AMZN -14.05%, INTEL -6.94% MSFT & NFLX -4%, APPL -3.66%. Nasdaq lost -13% in April (worst since 2008 Fin. Crisis) S&P500 has lost -13% in 2022 (the worst Jan-April since 1939). 50% of S&P500 companies have reported this Earnings season and 81% have exceeded expectations (average 66%). But outlooks (partic. from AZMN & APPL) have weighed. Volatility is back too, Jan-April there were 33 days with +/- 2% daily moves, in all of 2021 there were just 24.

- Yields moved significantly higher 10-yr closed at 2.887%. Up 1.96% today, at 2.942

- Oil & Gold both had a volatile session moved higher and then reversed to trade lower today. USOil tested to $108.00 on Friday but trades at $103.85 now. Gold tested $1920 zone Friday and trades at $1885 now, below key $1900 handle.

- Bitcoin declined from $40k on Friday to sub $38k to test $39k now.

- FX markets – EURUSD down to 1.0525, USDJPY up from 129.40 to 133.30 now and Cable recovered to 1.2550 now from 1.2410 lows on Friday.

Overnight – JPY – Consumer Confidence missed 33 vs 34.9 and Final Manu PMI in line at 53.5.

Week Ahead – The focus remains on inflation and the much anticipated response from the FOMC, RBA and BOE this week, while the markets price in action from the ECB down the road. The advent of month-end, a holiday in Japan on Friday, and the UK shut today accelerated some profit taking on Wall Street after the early rally. It looks as though many are sidelined into the weekend and ahead of the FOMC where there is a lot of uncertainty over the aggressiveness of the Fed’s normalization path, and the BOE’s ambiguity. Hiking rates too much too quickly would only increase the risk of a stagflation scenario and the BOE’s current policy is already much closer to neutral than the ECB’s. The week also sees NFP, and employment data from Canada, Europe and New Zealand.

Today – German Retail Sales, US ISM Manufacturing, EU Energy Ministers meeting, (Hungary would veto sanctions on Russian energy) Earnings from Italgas, Holidays in UK, China and many Asian countries.

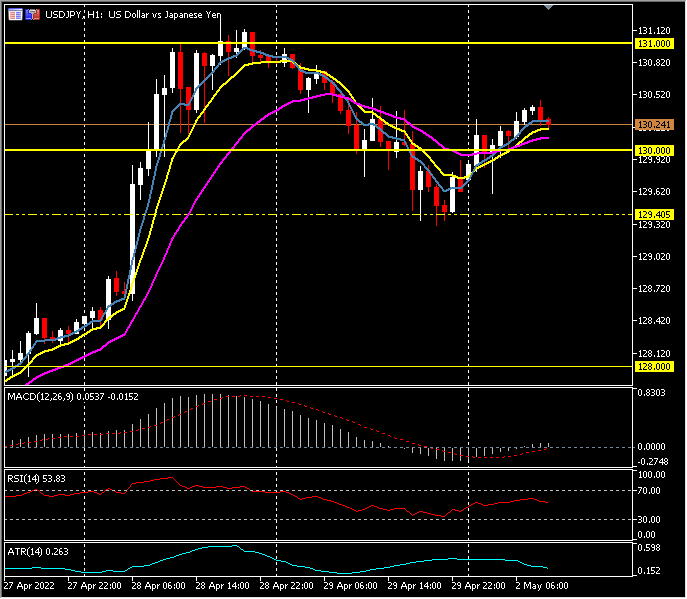

Biggest FX Mover @ (06:30 GMT) USDJPY (+0.49%) Rallied from lows under 1129.40 Friday to 130.45 highs today. Next resistance 130.50 MAs aligned higher, MACD signal line & histogram moving higher, RSI 54 & rising, H1 ATR 0.263, Daily ATR 1.38.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.