FX News Today

European Market Outlook: German 10-year Bund yields are holding above the 0.4% mark in early trade, despite the weaker than expected French GDP number ahead of the open, but underpinned by a sharp acceleration in German import price inflation to 4.8% y/y. Peripherals are slightly outperforming this morning after Draghi’s dovish leaning take on rates, which counterbalance rising confidence at the central bank that underlying inflation will gradually move towards targets. European Stock futures are mostly higher, in tandem with US futures amid hopes of strong US growth and an easing of trade tensions.Chinese bonds outperformed as local Stock Indices headed south and amid signs that the People Bank of China is endorsing policies to underpin growth as China readies for a protracted trade conflict with the US. Hopes for stronger US growth and a NAFTA deal underpinned sentiment and helped markets to move past yesterday’s tech sell off in the US and Dow Jones (USA30), USA500 and NASDAQ futures are all moving higher. Oil prices are little changed on the day and trading at USD 69.61 per barrel.The calendar still has French consumer confidence numbers but markets will focus on US GDP numbers in the PM session.

FX Update: The Dollar has been trading with a firming bias as markets anticipate a strong advance US GDP report for Q2, which will be released later today (and which President Trump and members of his administration have been flagging), though trading ranges have remained narrow thus far today. EURUSD edged out a 1-week low of 1.1637, and Cable and AUDUSD respective 3-day lows, of 1.3100 and 0.7372. USDJPY, meanwhile, remained below yesterday’s high at 111.25, though recovered back above 111.0 after a short-lived dip to 110.92. The low in USDJPY was seen as the 10-year JGB yield popped above 0.1% before a special yield-curve control buying operation by BoJ pushed it back below 0.1%. Japanese Tokyo CPI for July rose to 0.9% y/y from 0.6% y/y, above the 0.8% y/y figure expected. The PBoC set the USDCNY reference rate at 6.7942, up from yesterday’s 6.7662 rate.

Charts of the Day

Main Macro Events Today

- US GDP & Revised UoM Consumer Sentiment – Expectations – expected to rise at a 4.1% rate in Q2, double the 2.0% pace in Q1, while final Michigan sentiment may remain at 97.1 in July, a 6-month low, compared to a 14-year high of 101.4 in March.

- US PCE – Expectations – The core y/y PCE core prices expected to stick beyond the Fed’s 2.0% objective for a 3rd month in July, at 2.2%

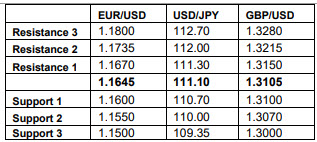

Support and Resistance Levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/07/31 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.