FX News Today

European Fixed Income Outlook: Risk aversion intensified during the Asian session, which gave a fresh boost to global bond markets. 10-year Bund yields fell to a low of 0.4619% in opening trade and is currently down -0.7 bp, versus a -2.2 bp decline in 10-year Treasury yields and a -0.3 bp dip in 10-year JGB yields. Stock markets sold off in Asia, led by mainland Chinese bourses, US stock futures are also heading south and, for now, trade jitters have moved firmly back to the forefront as the earnings season continues. The Fed did the expected yesterday and left rates on hold, while laying the ground for a September move. The focus now turns to BoE, which is expected to hike the repo rate by a further 25 bp today. The calendar also has Eurozone PPI, the UK Construction PMI as well as bond sales in France and Spain.

FX Update: The Dollar has traded firmer against most currencies and more than reversed initial declines that were seen after the largely as-expected Fed policy announcement yesterday. The upgrade in the Fed’s assessment of the economy to “strong” — from merely “solid” in the June statement — provided reason to buy the Greenback on dips. The USDIndex posted a 3-day higher, while EURUSD concurrent pushed lower, to a 4-day low of 1.1640. USDJPY was once again an exception to the broader Dollar theme, with the pair settling in a narrow range centred around 111.60 so far today, holding well within the bounds of yesterday’s range, though EUR-JPY and most other Yen crosses ebbed to 2- or 3-day lows, reflecting an underlying bid for the Japanese currency. This came concomitantly with the 10-year JGB yield rising to an 18-month high near 0.15%, pushing towards BoJ’s new 0.2% upside limit to its yield-curve control policy, though these moves stalled after BoJ member Amamiya in a speech today, reminded markets that the central bank will buy JGBs if yields rise rapidly, and that “powerful easing” remains appropriate as it will take time for the 2% inflation target to be achieved. Another incentive to buy Yen has been a fresh wobble in global stock markets, with the Trump administration confirming reports from late Tuesday that it is considering rising tariffs on $200 bln worth of Chinese imports, seen as a bargaining ploy by Trump ahead of Washington and Beijing’s return to the negotiations table, though China has returned fire by accusing the US of blackmailing.

Charts of the Day

Main Macro Events Today

- UK Construction PMI – Expectations – Is projected to fall to 52.8 in July, from June’s 53.1.

- BoE Monetary Policy & Rate Decision – Expectations – BoE expected to hike the repo rate by a further 25 bp to 0.75%.

- BoE Inflation Report – BoE should leave the QE total at GBP 435 bln for government bond purchases and GBP 10 bln for corporate bond purchases

- BoE Gov. Carney Speech at 11:30 GMT

- US Unemployment Claims – Expectations – a 220k increase in unemployment claims is expected.

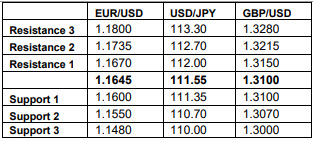

Support and Resistance levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/08/02 15:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.