FX News Today

FX Update: The Dollar has lifted after five straight down sessions. The USD index (DXY) is showing a 0.3% gain heading into the London open, at 95.41, rising above yesterday’s high but remains well below the 14-month high seen last week at 96.98. EURUSD has concurrently sunk to a two-day low of 1.1542, putting in some distance from yesterday’s two-week peak at 1.1623. USDJPY has also been on the up, printing an eight-day high of 110.93, and extending the rebound from Monday’s eight-week low at 109.77. Wall Street finished moderately yesterday, and US500 futures are presently flat, while US Treasury yields are lower. Fed funds futures are showing 50-50 odds for a 25 bp hike in December. There is conjecture among Fed watchers that Chairman Powell will retain a hawkish tone in his keynote speech on Friday, despite President Trump’s calls for looser policy. Elsewhere, the Australian Dollar has taken a tumble amid political turmoil regarding leadership challenges faced by Prime Minister Malcolm Turnbull. AUDUSD has lost over 0.7% in falling to six-day lows under 0.7300.

FOMC minutes: The most important point in the minutes was that “many participants” believed another hike would be appropriate “soon”, which could be interpreted as an indication for a September tightening. Participants noted that the funds rate was moving closer to the range of estimate of a neutral level, with a number of participants emphasizing uncertainty in estimates of that level, and agreeing that “accommodative” language may no longer be appropriate fairly soon. Participants generally noted the strength of the economy in Q2, as well as favorable factors that were supporting above-trend growth, including financial conditions. But “several” stressed that transitory factors may have played a role, including an outsized increase in exports. All officials viewed trade as an “important source of uncertainty.” There was some discussion regarding firms having greater scope to increase prices due to strong demand or rising input costs. There was also talk over the implications of the flattening yield curve. The minutes indicated that balance sheet discussions would continue in the fall.

Asian Market Wrap: 10-year Treasury yields are down -0.5 bp at 2.813% and 10-year JGBs fell back -0.2 bp to 0.083% amid a wider decline in Asian rates. Australian bonds outperformed as the ASX declined and AUD weakened as Prime Minister Turnbill faces leadership challenges. Elsewhere, stock markets traded mostly mixed, with mainland China and Hang Seng underperforming. Topix and Nikkei posted marginal gains of 0.02% and 0.18%, while Hang Seng and CSI were down -0.83% and -0.59% respectively as of 05:18GMT. The additional US and China tariffs come into effect in the middle of ongoing trade talks and China said it will lodge a complaint with the WTO. US stock futures are heading south after a mixed close yesterday and with the Fed minutes confirming that further rate hikes remain on the cards, but also showing some concern about the impact of possible prolonged trade battles. Markets are also looking ahead to the Jackson Hole meeting amid political risks for Trump from the legal battles of his former advisors.

Charts of the Day

Main Macro Events Today

- Jackson Hole Symposium – The annual Jackson Hole Symposium is hosted by the Federal Reserve Bank of Kansas City and is a forum for the top central bankers, policy experts and academics of the world who come together to discuss policy issues. Comments and speeches from central bankers and other influential officials can create significant market volatility. This year’s topic relates to the changing market structure and its implications for monetary policy. Most awaited speech is by Fed Chairman Jerome Powell.

- ECB Monetary Policy Meeting Accounts – The accounts, similar to the FOMC minutes, aim to provide an overview of financial, economic and monetary developments aimed to provide the rationale behind policy decisions. Currency response depends on the accounts’ content.

- US Jobless Claims – Consensus forecasts expect that claims will increase slightly compared to last week.

- New Zealand Trade Balance – Trade balance expected to deteriorate in July, registering a $0.5bln decline.

- Japan Consumer Price Index – CPI expected to decline and stand at about 0.4% YoY, compared to 0.7% last month.

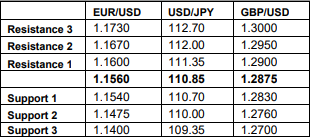

Support and Resistance Levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/08/23 15:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Dr Nektarios Michail

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.