FX News Today

Asian Market Wrap: 10-year Treasury yields are down -0.2 bp at 3.061% and 10-year JGB yields are up 0.1 bp at 0.110%. Yields have come quite a way over the past week and Treasury yields are still holding above the 3% mark, but the stock market rally started to stutter during the Asian session with indices turning mixed. The Dow Jones still managed a solid gain yesterday, but the NASDAQ closed slightly lower and in Asia stocks drifted. Japanese indices traded near three-month highs, but at these levels it seems investors are getting cautious as trade concerns continue to cloud over the outlook. Nikkei and Topix are down -0.045 and -0.12% respectively. It would not be the first time that Chinese indices rebound late in session, but it seems for now markets are consolidating and waiting for further news. US futures are also narrowly mixed, oil prices are higher and the WTI future is trading at USD 71.63 per barrel.

FX Action: USDJPY has drifted lower, posting a two-day low at 112.07 in a moderate move driven by a softer Dollar. Risk appetite has continued to hold up with Asian stock markets gaining, albeit modestly, for the most part, and the main Chinese indexes lifting out of negative territory in the first hour of trading after the lunch break. Japanese PM Abe won a leadership challenge by a landslide, as expected, which puts him on track to becoming Japan’s longest serving prime minister. In the bigger view, USDJPY is currently trading in the upper reaches of a broadly sideways range that’s been unfolding for some 10 weeks now. Great odds have been placed for a sustained move downward rather than a sustained move upward as China looks to be digging for trade war escalation (at least until after the midterm elections in the US), which could lead to an increased safe haven premium being put on the Yen. USDJPY has resistance at 112.44-45, and support at 111.77-80.

Charts of the Day

Main Macro Events Today

- SNB Rate & Monetary Policy – Expectations – The SNB is widely expected to maintain its expansionary policy, with the deposit rate to be left -0.75% and the 3-month Libor range Libor at -1.25% to -0.25%. The central bank is also expected to reiterate that it will “remain active in the foreign exchange market as necessary while taking the overall currency situation into consideration”.

- UK Retail Sales – Expectations – The Retail sales are anticipated a 0.2% m/m contraction in August, correcting after rising 0.7% m/m in the month prior.

- US Philly Fed Manufacturing Index – Expectations – The Philly Fed index should rise to 19.0 in September, from a 2-year low of 11.9.

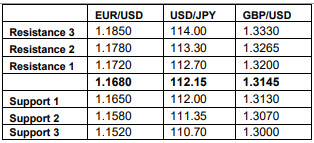

Support and Resistance Levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/09/20 15:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.