FX News Today

European Fixed Income Outlook: 10-year Bund yields are down -1.7 bp at 0.376% in opening trade, Treasury yields have fallen back to just over 3.1% in the wake of the ongoing market rout, while 10-year JGBs are down -1.6 bp at 0.105%. US markets wiped out this year’s gains yesterday, Asian stocks markets are also sharply lower, while US futures are stabilising and UK futures are pointing to further losses in Europe. In this environment Draghi is likely to sound cautious at today’s press conference even as the ECB is set to confirm the phasing out of net asset purchases by the end of the year. The rate guidance will likely remain unchanged, with no hike planned until after the summer of 2019 at the earliest. Norges Bank is also expected to keep rates unchanged today, while data releases including the German Ifo survey and the UK CBI retailing survey come with the risk to the downside.

Asian Market Wrap: US Treasury yields have moved up slightly from lows and are up 0.4 bp on the day at 3.107%, still considerably below recent highs after yesterday’s tech stock driven rout on US markets was followed by further losses in Asia. JGB yields corrected -1.4 bp and are at 0.107%, after the NASDAQ closed down -4.4% yesterday and U.S. stocks wiped out this year’s gains after mixed earnings reports from the likes of AT&T and Texas Instruments. In Asia Topix and Nikkei dropped -2.8% and -3.5% respectively. The Hang Seng lost nearly 2% so far and Shanghai and Shenzhen bourses wiped out -1.385 and -1.92%, while the ASX declined -2.8%. The MSCI Asia Pacific Index was pushed deeper into a bear market. Concerns that the earnings momentum is levelling off and that tighter financial conditions, coupled with ongoing trade tensions are hitting the global growth outlook are prompting investors to rethink lofty equity valuations. There are plenty of geopolitical risks from the Kashoggi fallout to the prospect of a fresh arms race between the US and Russia. US futures are marginally higher, leaving some chance that US markets will at least try to stabilise today.

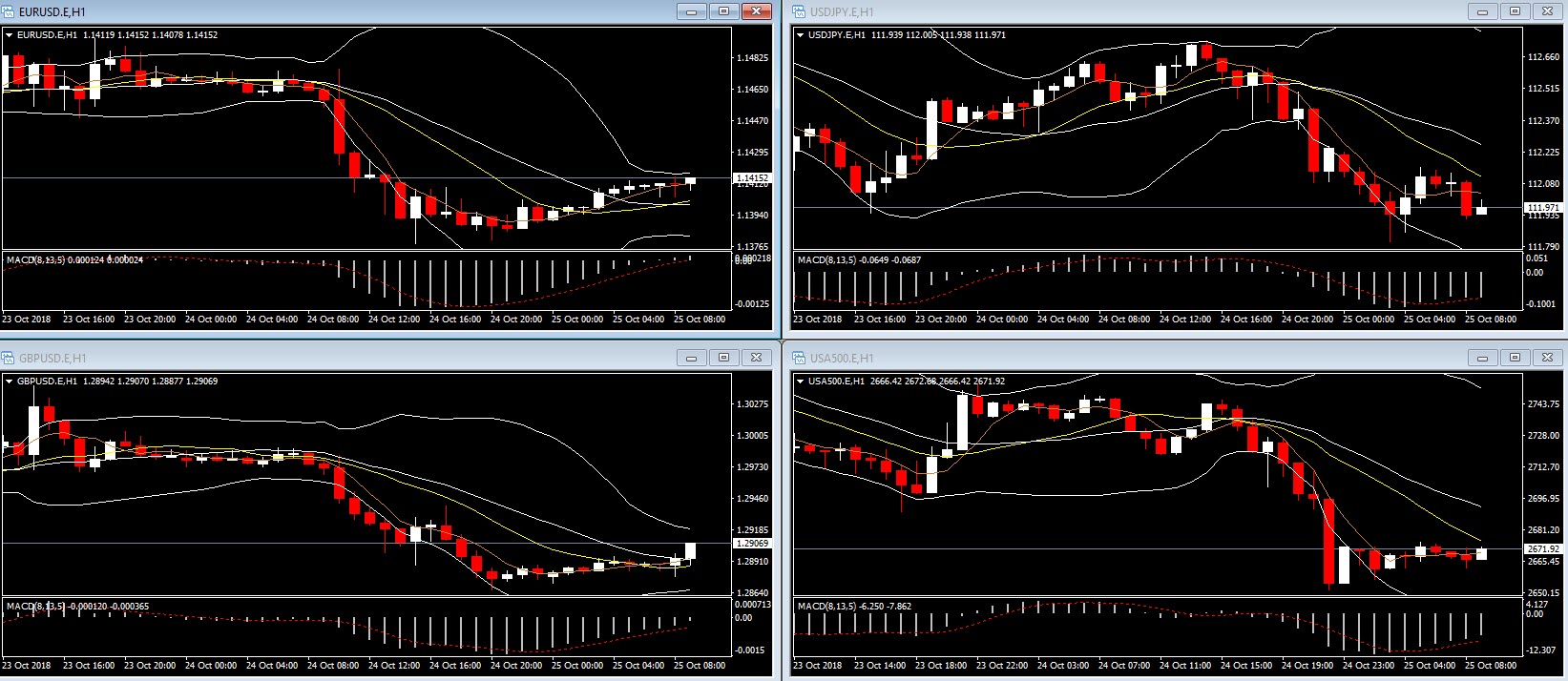

Charts of the Day

Main Macro Events Today

- ECB Interest Rate Decision – Expectations – ECB is not expected to change its interest rate, as per the guidance it has offered in the latest ECB Report.

- US Durable Goods Orders- Expectations – US Durable Goods Orders excl. Transportation are expected to continue their increase by 0.3%, compared to an increase of 0.1% last month.

- Pending Home Sales – Expectations – Pending home sales are expected to have decreased by 0.1% compared to a 1.8% decrease last month.

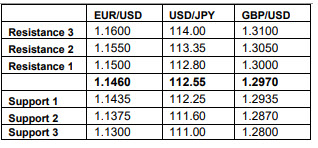

Support and Resistance Levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/10/30 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Dr Nektarios Michail

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.