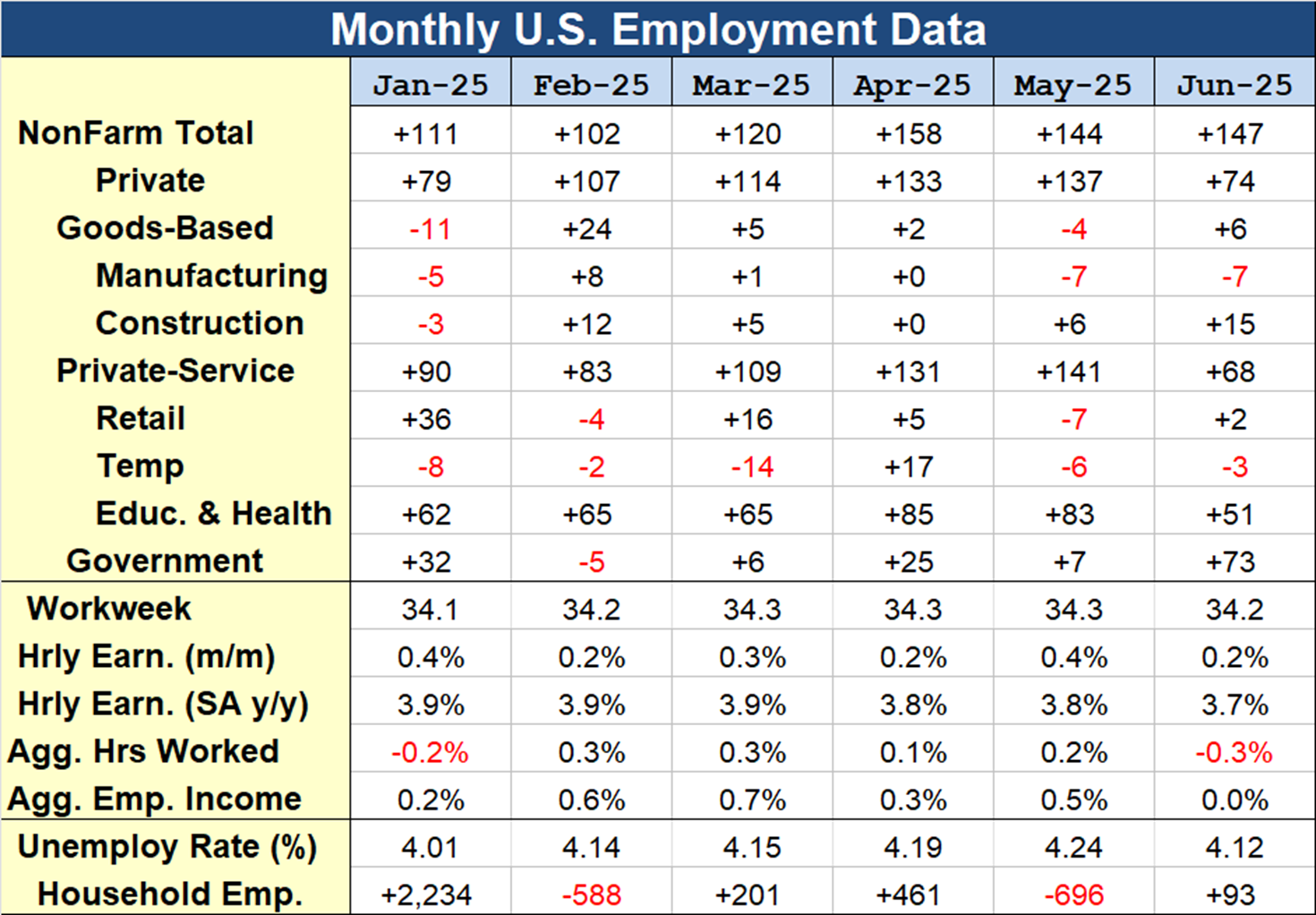

The Nonfarm Payroll for May is expected at 360k following a 428k rise in both April and March. The workweek should remain steady at 34.6, leaving a 0.3% hours-worked rise, while a 0.4% hourly earnings gain should be seen and a steady jobless rate at 3.6%. Consumer confidence and vehicle sales eased through May, and initial claims drifted higher while continuing claims continued to tighten and producer sentiment extended its pullback from a November peak. Job growth has outpaced the GDP path into 2022, and the risk is that job growth could correct lower.

The 360k nonfarm payroll forecast assumes a 330k private jobs increase (i.e. private service jobs increase of 250k in May, after gains of 340k in April, and 357k in March). The goods based employment increase is pegged at 80k, after gains of 66k in April and 67k in March. Construction employment is seen rising 30k after 2k in April and 20k in March, with factory jobs rising 45k after a 55k April gain.

Seasonal Trends and Weather

The graph below shows the two-year average NSA payroll change for each month, pre-2020. The seasonal impact through the year on payroll changes is mostly positive, but tends to be negative in December, January and July. Distortions of last year’s COVID-19 would have produced negative averages for March and April as well. The ’18/’19 NSA average fell to 804k in May, from 1,020k in April and 689k in March. The red bars show each month’s variance. After a first-half peak in February, variance decreases over the spring before reaching a second-half peak in September.

For disruptions to employment from weather as gauged in the household survey, the biggest disruptions occur in the winter months generally, with the average peaking in February. There is an additional climb through the late-summer months due to disruptive hurricanes in some years. The ten-year average number of people not working as a result of weather fell to 45k in May, from 72k in April, 146k in March, and 351k in February.

Hourly Earnings

The average hourly earnings is expected to rise by 0.4% in  May versus 0.3% in April and 0.5% in March. The y/y wage growth should edge down to 5.4% from 5.5% in April, 5.6% in March, and 5.2% in February. The trend remains solid. Prior to the pandemic, growth in hourly earnings was gradually climbing from the 2% trough area between 2010 and 2014 to the 3%+ area until the pandemic-induced spike.

May versus 0.3% in April and 0.5% in March. The y/y wage growth should edge down to 5.4% from 5.5% in April, 5.6% in March, and 5.2% in February. The trend remains solid. Prior to the pandemic, growth in hourly earnings was gradually climbing from the 2% trough area between 2010 and 2014 to the 3%+ area until the pandemic-induced spike.

ADP Survey

We expect a 330k May ADP climb that tracks our 330k private BLS payroll estimate with a 360k total BLS payroll gain, after a likely boost in the 247k April gain that would narrow the gap to the 406k BLS private payroll rise in that month. We expect a solid 80k gain for the goods sector, and a 250k rise for private service jobs led by the leisure sector. By company size, we expect a continued skewing of gains toward large companies that extends the pattern evident since Q3 of 2021.

The May payroll forecast is for a 360k increase after a 428k April rise, with the workweek to hold steady at 34.6, a 0.3% hours-worked rise, and a 0.4% gain for hourly earnings. The jobless rate should hold steady at the new cycle-low 3.6% for a third month. The impressive pace for job growth through April outpaced GDP, which posted a -1.5% Q1 contraction rate. The risk is for a payroll under-performance in May. Consumer confidence and vehicle sales extended declines in May, producer sentiment is shedding some of the strength seen since November, and we’ve seen divergent claims paths, with an up-tilt for initial claims but further declines for continuing claims.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.