- USDIndex – steady at 112.90 following US inflation which reinforced bets of a 90.9% chance of a 75 basis point rate hike, and a 9.1% chance of a 100 bp increase in the Fed’s next meeting. Yields down, 10-year Treasury rate is down -4.1 bp at 3.977% and the German Bund future has corrected -6.3 bp, after the JGB rate corrected -0.3 bp to 0.24%.

- GBP – Sterling rallied to 1.1300 on calls for PM Truss to resign and ahead of UK Chancellor announcement for tax and spending measures, 2 weeks earlier than scheduled, as he tries to stem a loss of confidence in the government’s fiscal plans. Truss said on Friday that corporation tax will rise to 25% from April 2023 instead of remaining it at 19% as part of her government’s initial “mini-budget”. Medium-term fiscal plan remains as scheduled on Oct. 31.

- Daily Mail reported that: “British lawmakers will try to oust Truss this week despite Downing Street’s warning that it could trigger a general election.”

- EUR – slightly up to 0.9735.

- JPY – pinned to 32-year (1990) highs at 148.79 as markets await signs of intervention from Japanese authorities.

- Stocks – Stock markets have remained under pressure overnight, after a weak close on Wall Street Friday, after inflation concerns were rekindled by a US survey showing the first rise in inflation expectations in a while. Still, US futures are higher and with a nearly 1% rise in the NASDAQ leading the way.

- China and Hong Kong stocks fell after Chinese President Xi talked up national security, while dashing hopes of any changes in growth-hitting zero-COVID policies and property sector curbs. Xi called for accelerating the building of a world-class military, while touting the fight against COVID-19 as he kicked off the Communist Party Congress on Sunday by focusing on security and reiterating policy priorities. Greater emphasis on national security comes amid heightened geopolitical tensions. The biggest applause came when Xi restated opposition to Taiwan independence.

- USOil – holds support at $85.

- Gold – $1650.

- BTC – down for the day to $19214.

Today – US Monthly Budget, BOC Outlook Survey. All eyes remain on UK though and the speech of Chancellor Hunt.

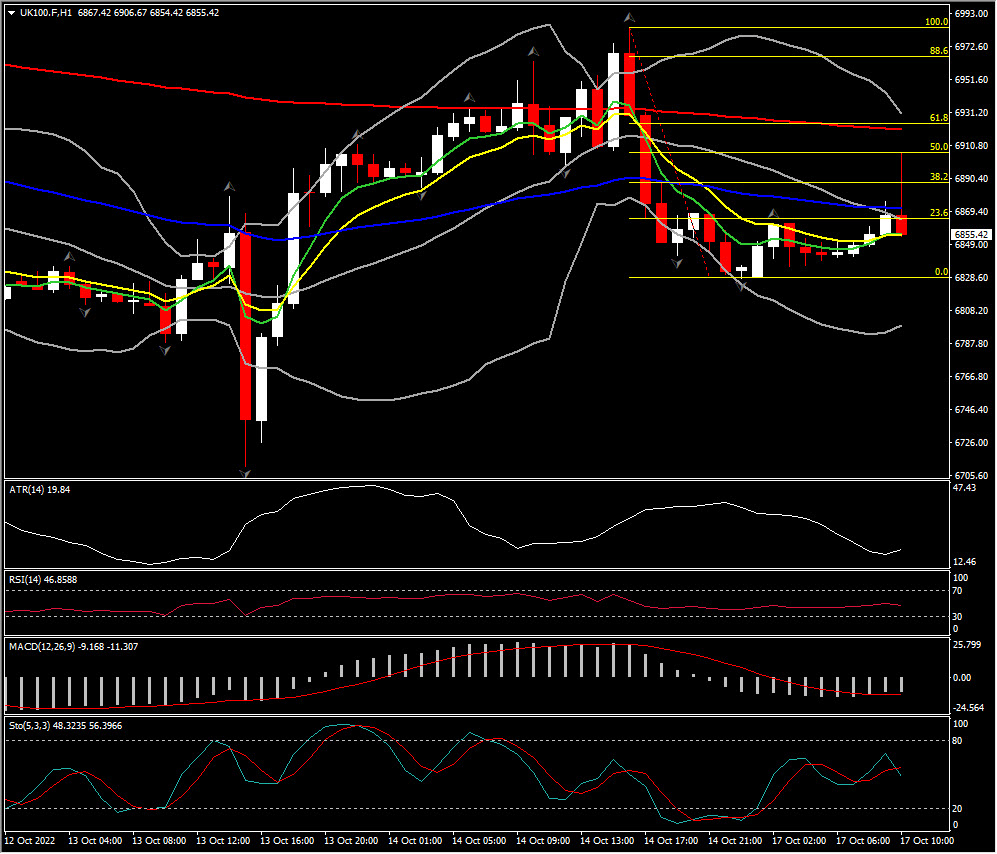

Biggest FX Mover @ (06:30 GMT) UK100 (+0.23%) rallied at EU open to 6907 but pulled back asap. MAs flattened, MACD histogram & signal line hold below 0, RSI 46 & falling, H1 ATR 19.84, Daily ATR 142.87.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.