Canada’s job market is expected to show another modest increase to start the year, after the 78.4k surge in November gave way to a 7.8k rise in December. Canada employment should expand 10.0k in January.

The unemployment rate on the other hand, is expected to nudge higher to 5.7% in January, from the 43-year low 5.6% in November and December. Earnings growth is expected to remain subdued, adding to the softening inflation backdrop, well below the 3.9% pace in May of 2018, at 0.4% m/m in January.

The risk for today’s data is to the downside, as January’s data so far has showed a constrained Canadian economy to begin 2019, based on consumer and factory sentiment. The forecast for Canada’s employment report has a rather sparse set of supporting indicators, which were mostly weaker. Dealer reported lower vehicle sales and household sentiment remains down, while these along with the factory sector and the slump in Canadian Consumer confidence shed further optimism in January. The Bloomberg Nanos Canadian Confidence Index was 54.2 at the end of January, similar to the figures seen since late November that have been near two year lows.

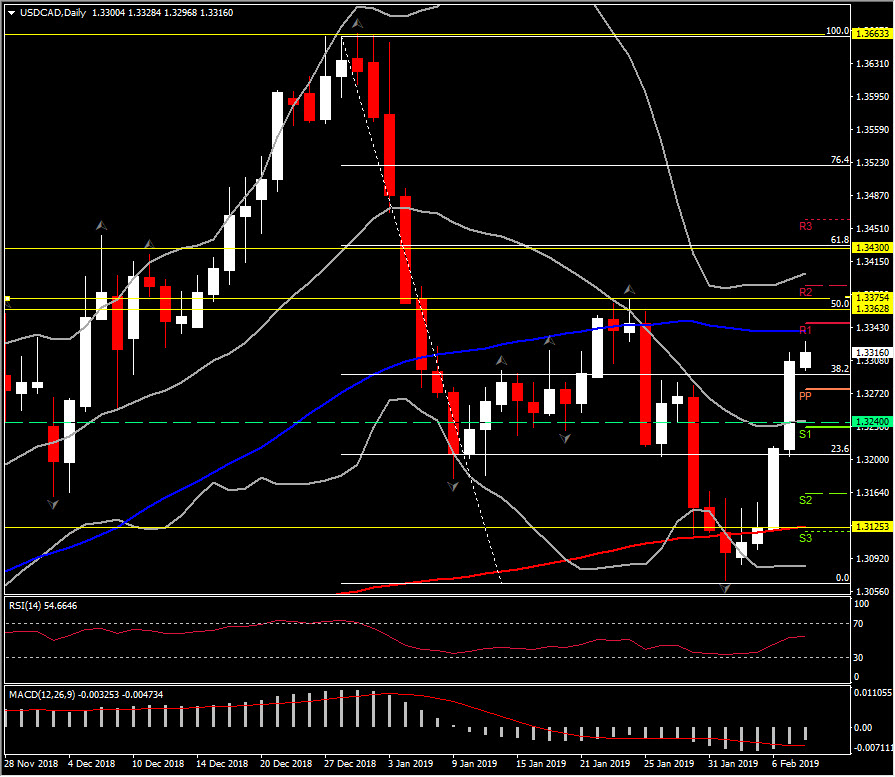

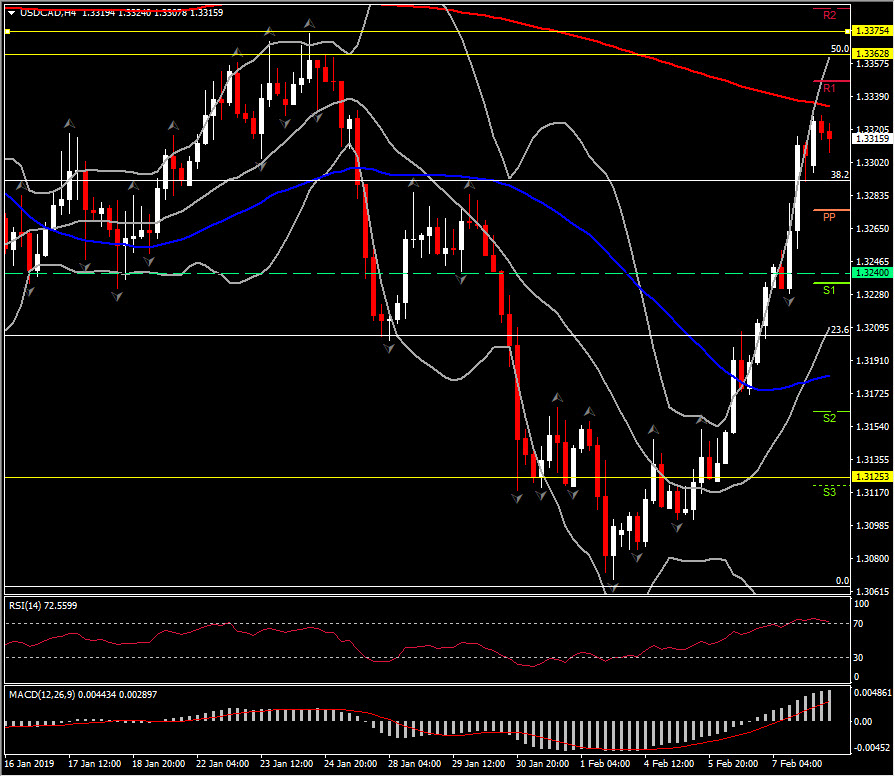

As the risk is for a negative print for total jobs to begin 2019, the Canadian Dollar could continue to depreciate. USDCAD is up for a fifth consecutive day, today printing a 13-day high at 1.3328, extending a recovery from last Friday’s 3-month low. The up phased has been concomitant with a down phased in oil prices, while sustained gains in crude prices are a boon to Canada’s terms of trade, and vice versa.

Overall, USDCAD is strongly supported by 200-day SMA since April. Hence long term Support holds at 1.3126 (200-day SMA), while the 20-day SMA and PP of the day provide immediate Support levels at 1.3240 and 1.3275 respectively.

Resistance holds at 1.3363-1.3375 area, presenting the area between the 50% retracement on the decline seen since 1.3660 high and January’s peak. In the scenario of disappointing jobs data today, the pair could be seen reaching this area. Further gains, could lead to the 61.8% Fib. level at 1.3430 level. At this level we could face a correction lower.

From the market perspective, a damp jobs report could underpin expectations that the BoC is stuck on the sidelines until 2020. However, BoC’s view that the current (and Q4) slowing is temporary has been supported by the recent data, as opposed to the data showing a more pronounced slowing in growth than the Bank anticipated.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.