With markets in Europe and North America closed today and only a few Asian markets open there was little direction on very limited volume. Weak PMI and Housing data from China on Saturday and a poor global outlook from the IMF yesterday start the New Year in the same down-beat way 2022 concluded. The Yen is the biggest gainer today.

China’s official Services PMI cratered -5.1 points to 41.6 in December after falling -2.0 ticks to 48.7 in November. This is a sixth consecutive monthly decline, a third straight month in contraction, and the lowest level since February 2020. It was at 52.7 a year ago. The December manufacturing index slid -1 point to 47.0 after falling -1.2 points to 48.0 previously. It too is a third month below the 50 expansion-contraction mark, and is the eighth month in 2022 below 50. It is also the weakest since February 2020s 35.7.

2023 is going to be a tough year as the main engines of global growth – the United States, Europe and China – all experience weakening activity. – IMF “tougher than the year we leave behind…China’s chaotic reopening is proving problematic”.

- The USD Index down at 103.00 levels, but in 2022 the USD was King once again.

- EUR – rotates back to 1.0700 levels today but tested 1.1500 highs and 0.9530 lows in 2022.

- JPY – the strongest today and trades at 131.00 and 10-day lows, 2022 saw a breach of 150.00 form 113.00 lows.

- GBP – Sterling traded over 1.4200 and under 1.0400 in a volatile (3 x Prime Minister, 5 x Finance Minister) 2022 for the UK. Today Cable holds over the key 1.2000 level at 1.2060.

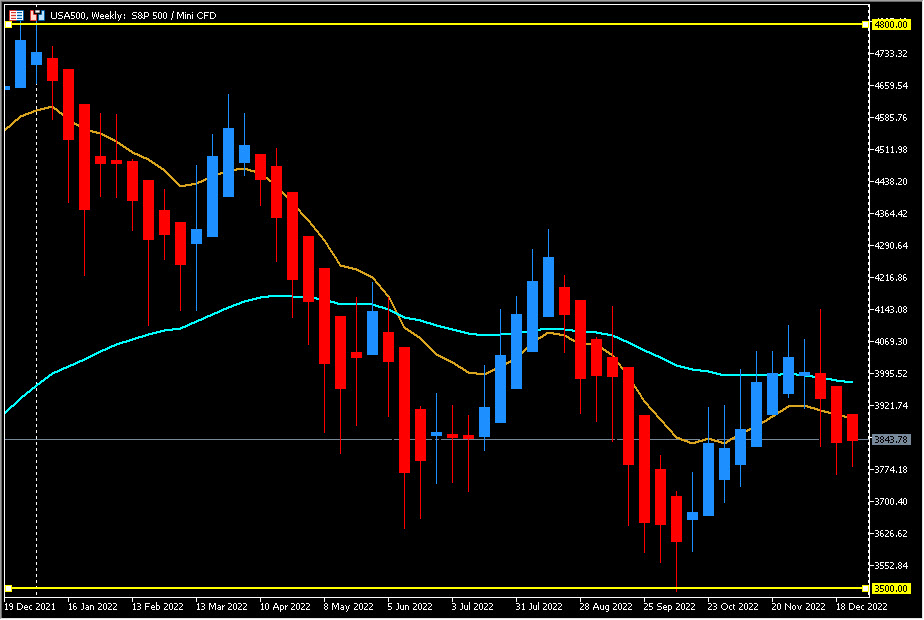

- Stocks – Wall Street collapsed during 2022 into Bear market territory once more (NASDAQ -33.10%) and the US500 lost over 900 points (-19.44%) its worst year since 2008. The MSCI Global equity index lost 18.7%.

- USOil – Trades over $80.00, to start 2023. Russia’s invasion of Ukraine caused a spike to over $123.00 in February before falling to test $70.00 in December on weak global demand expectations.

- Gold – Trades at $1830 levels today. Rising Inflation and interest rates in 2022 had a rather muted impact on the precious metal. The war-inspired February spike to $2070 was followed during the rest of the year to October lows under $1620, before recovering $1800 in December.

- BTC – Sentiment woes continue. The biggest coin trades at $16,700 today after a tumultuous year which saw prices collapse from the $50,000 to the $15,000 level as the FTX saga broke.

Today – No Economic data due

Biggest FX Mover @ (07:30 GMT) NZDJPY (-0.40%) muted moves in low volume FX markets. Continues to decline from last week’s rejection of 85.00, trades at 82.85 now, resistance at 83.00 and support at 82.50. MAs aligned lower, MACD histogram & signal line negative and falling. RSI 38.33 & falling, H1 ATR 0.173, Daily ATR 0.935.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.