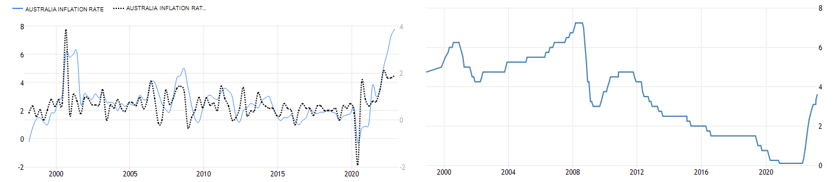

In today’s Asian trading session, the RBA announced a 25 basis point rate hike to 3.60%, the highest level since May 2012. The central bank has raised rates 10 times since April last year, for a total of 350 basis points. While the RBA has indicated that it will still further tighten monetary policy (the extent of rate hikes will depend on the performance of economic data), recent data has also shown signs that Australian inflation is showing signs of peaking – largely due to weaker demand for goods in the short term (but demand for services remains strong and prices are likely to remain high). The labour market remains tight and the unemployment rate remains at a near 50-year low. The RBA expects inflation to decline this year and next, and to reach around 3% by mid-2025. Market bets on peak interest rates were lowered to 4% from just above 4.1%. The central bank’s growth expectations for the next two years are “below trend”.

Figure 1: Australian inflation (left) and interest rates (right):Trading Economics

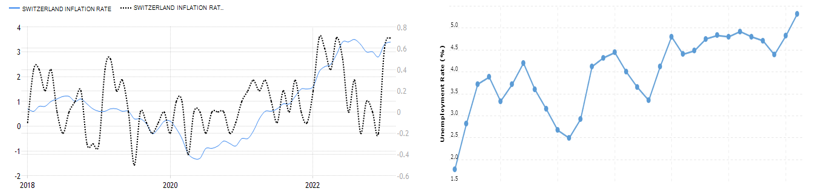

On the other hand, Swiss CPI posted 3.4% year-on-year in February, above market expectations of 3.1% and the previous 3.3%, and at a new high since August last year. On a month-on-month basis, the figure recorded 0.7%, reaching last May’s level and the previous value of 0.6%. The sub-data showed further cost increases in some categories, including food and non-alcoholic beverages (6.5% vs. 5.6% previously), restaurants and hotels (3.5% vs. 2.6% previously) and entertainment and culture (2.8% vs. 1.9% previously). The other categories with slower cost growth were housing and energy (4.7% compared to 5.1% previously), household maintenance (4.5% compared to 5.2% previously) and transport (3.9% compared to 4.7% previously).

Figure 2: Swiss inflation rate (left) and unemployment rate (right):Trading Economics, Macrotrends

Subsequently, Switzerland also released its unemployment rate for February. The figure was recorded at 1.9% on a quarterly basis, in line with market expectations and the previous value. The current reading is at the lowest level in over 30 years of record keeping, and only slightly higher than in 1991 (1.78%). On the 23rd of this month, the Swiss central bank will announce its interest rate resolution. At present, the market largely believes that the central bank has a more than 90% probability of raising interest rates by 50 basis points to 1.50%.

Technical Analysis:

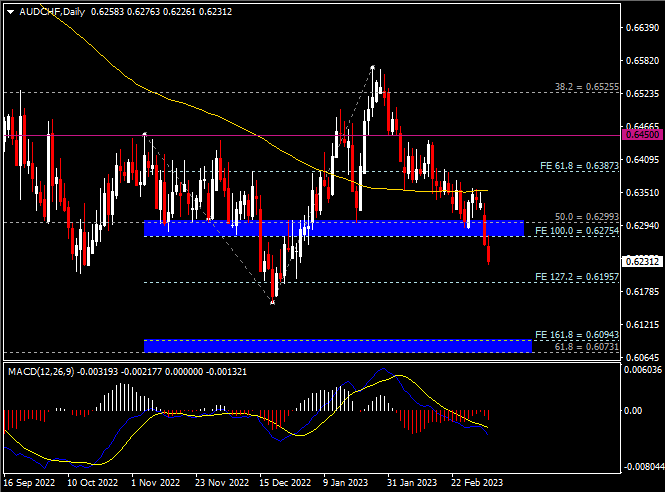

AUDCHF (Daily Chart): The pair has come under further pressure following the RBA’s interest rate decision and the above series of economic data releases, and currently remains below the 0.6275-0.63 resistance area. The 100-day SMA above further elaborates on the continuation of the short momentum. As long as these two key points are not effectively broken, the trend remains biased to the downside with support at 0.6195, last year’s full-year low of 0.6159 and the 0.6075–0.6095 area. As for the indicators, the MACD double line is below the 0 line but the signal line has resumed gaining momentum.

Click here to access our Economic Calendar

Larince Zhang

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.