Yesterday, was a day with plenty of unexpected events. The Norwegian Norges and the British BOE have displaced investors by surprising to the upside (50 bps hikes instead of the expected 25); the Turkish CBRT has done the same but heavily to the downside (650 bps to a 15% rate instead of the expected 21% – and the TRY has traded down almost 4% both against the USD and the EUR).

At least the Swiss SNB was more suitable for the faint-hearted: +25 bps to 1.75%, as expected. This brings the total amount of rate hikes since the beginning of the cycle to 200 bps, well below the ECB (400 bps) or the FED (500 bps).

A few more indications came from the press conference following the announcement of the decision: inflation remains above the SNB’s inflation target of between 0 and 2% – although it has fallen sharply. Headline number is steady at 2.2% (down from 3.4) and core sits at 1.9%: despite what may seem like a good result, the SNB is still concerned about the second round effects and has revised up its inflation forecasts for the next few years, now expected to remain at 2.2% in 2024 as well.

This may signal growing concerns about the long-term outlook for inflation or maybe an attempt to sound hawkish: after all, this second hypothesis has somehow been confirmed by President Jordan’s statements, which seem to hint to a new hike in September.

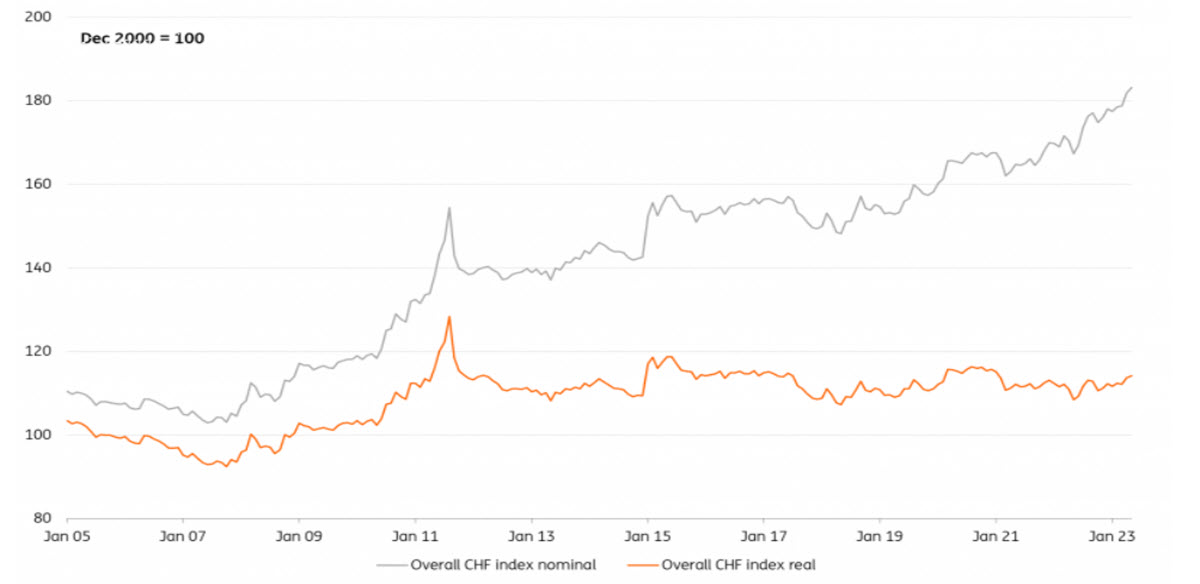

CHF real and nominal appreciation, Index

The SNB has admitted that it has extensively sold its FX reserves in recent months so as to keep the real Swiss franc stable to fight inflation (”In the current environment, the focus is on selling foreign currency”): actually it has managed to get a 2% nominal appreciation of the trade-weighted Swiss franc over the last quarter, something it will probably not have to continue to do as the inflation differential with other economies should narrow.

Finally, GDP growth: it was strong in Q1 but is expected to remain modest until the end of the year, settling close to +1%.

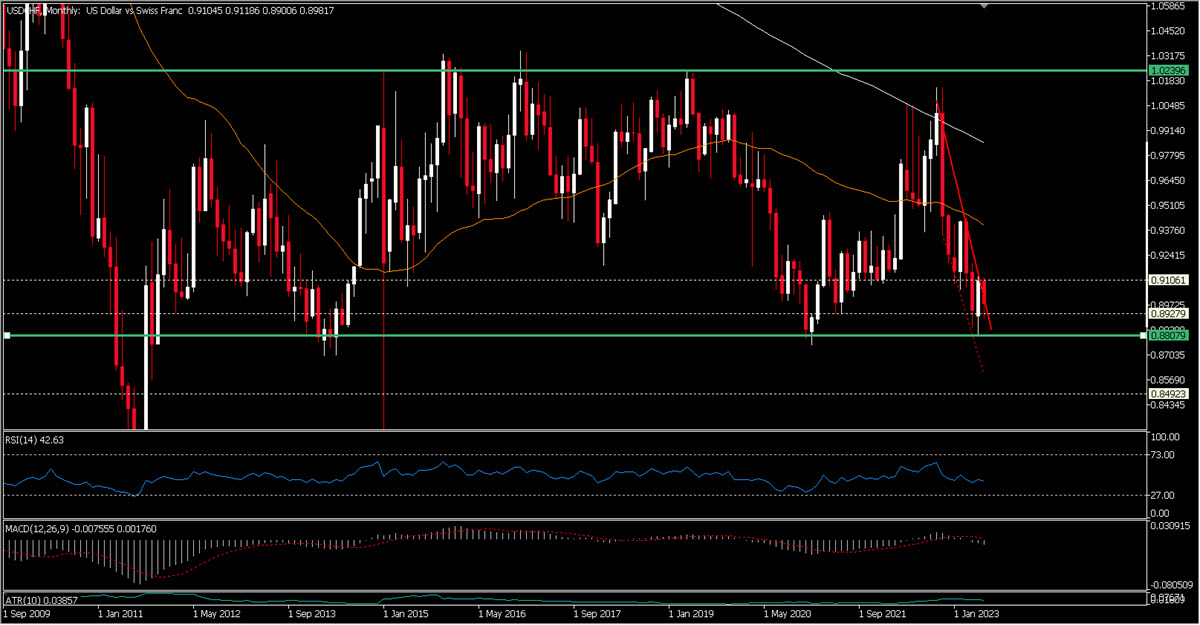

TECHINCAL ANALYSIS

USDCHF, Monthly

In light of all this, we believe that the time of a steadily descending USDCHF, as it has been since November 2022, is coming to an end. The area of 0.88, tested in May, has been an important support zone since 2011 and has almost always established a long-term low. The bearish trend since November 2022 seems to have been broken a few weeks ago and is being retested these days – right here in the 0.89 area. If this holds, we would also have rising lows on the daily chart and the highs were already slightly retouched upwards at 0.9147, exactly when the downtrend was broken on 31 May 2023. RSI is positive and so is the MACD. Above the MA50 (0.8975) there is further positivity with a reasonable target in the 0.91 area. It is obviously not impossible to see new weakness leading the price towards 0.89 or even to retest 0.8830, but this would not change our long-term view that does not exclude seeing USDCHF close to 0.92 within a few weeks.

USDCHF, Daily

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.