Around the time of yesterday’s US market close, rumours spread that the Biden administration is considering new restrictions on exports of AI chips to China, as concerns rise over the power of the technology in the hands of US rivals. The news was reported by the WSJ, citing sources. This morning there was new confirmation from the DJ who claim that the US commerce department could move as early as next month to stop shipments of chips made by Nvidia (NVDA).

The fact is that semiconductors, chips, the beating heart of our computerised and ultra-technological world, are as important as oil today and geo-political friction arises over them. You all know about the US-China confrontation over Taiwan but you may not know about the treasure hidden in the Asian island, the Taiwan Semiconductor Manufacturing Company (TSMC), a company that holds over 56% Global Market Share of the Semiconductor Industry. Semiconductor ICs manufactured by TSMC are used by almost all Top Semiconductor Companies in the World including – AMD, Apple, ARM, Broadcom, Marvell, MediaTek, and Nvidia itself.

NVDA is a company founded in 1993 and initially focused on computer graphics and the production of GPUs: driving high-resolution graphics for PC games requires particular mathematical calculations, which are more efficiently run using a “parallel” system; in such a system, multiple processors simultaneously run smaller calculations. Nvidia specializes in these high-performance processors and was in the right place at the right time. In recent years, the need for complex calculations has spread to every area of our lives and to the most cutting-edge sectors: autonomous driving, robotics, crypto currencies mining and – more lately – machine learning and Artificial intelligence, including YouTube algorithms and ChatGPT.

NVDA is in a privileged and leading position in all these segments. Not surprisingly, it is the real leader of this year’s market rally with a performance of 186.55% YTD. But with yesterday’s closing price of $418.71, questions arise: What are its multiples? Aren’t the valuations a bit of a stretch? Or do the future prospects justify them?

Net margins are totally in line with the sector (16.19% vs 16.52%), ROE somewhat lower than average (17.93% vs 19.52%), debt rather higher (debt/equity 49.56% vs 29.50%).

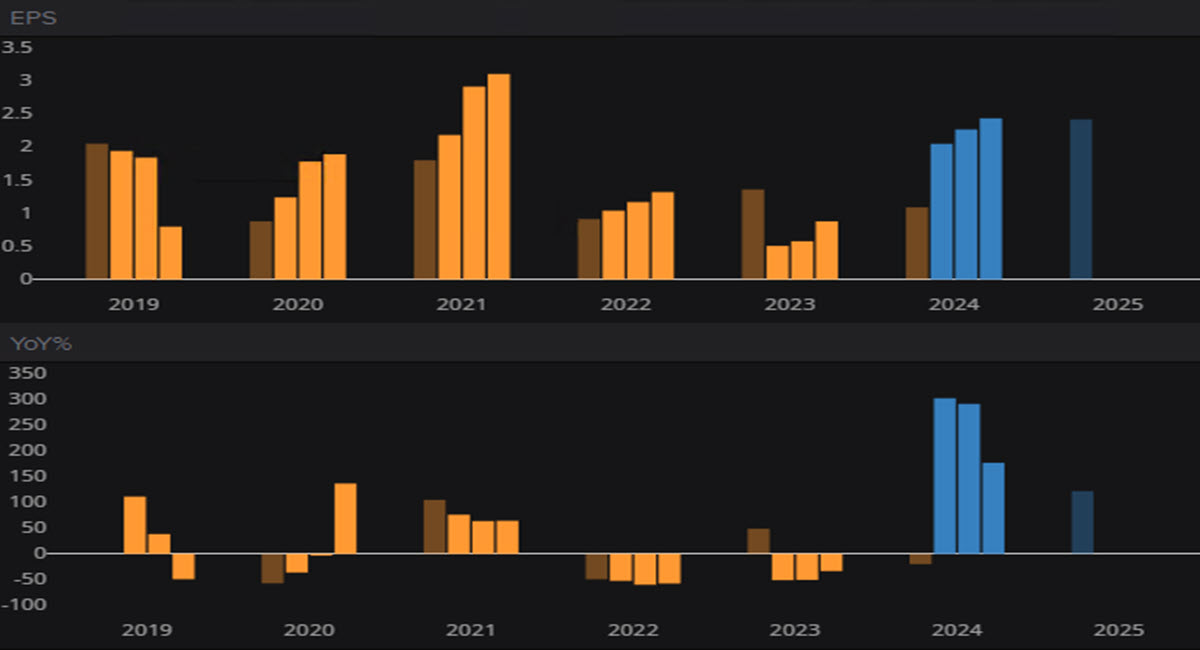

NVDA, EPS growth

The multiples, however, are eye-watering: PE 240.35 against a sector average of 43.33, Fwd PE 54.41 (14.69 average), P/ Sales 38.35 (sector at 7.30). The market cap of 1.03T is equivalent to all sales in the next 38.35 years, assuming they remain stable as in 2022. What is interesting, however, is that EPS and Dividend Yield are well below the industry average (1.74 vs 5.61 and 0.04% vs 1.44% respectively).

Fundamental analysts likely consider NVDA very, very expensive: it’s a momentum trade (despite the excellent outlook).

TECHNICAL ANALYSYS

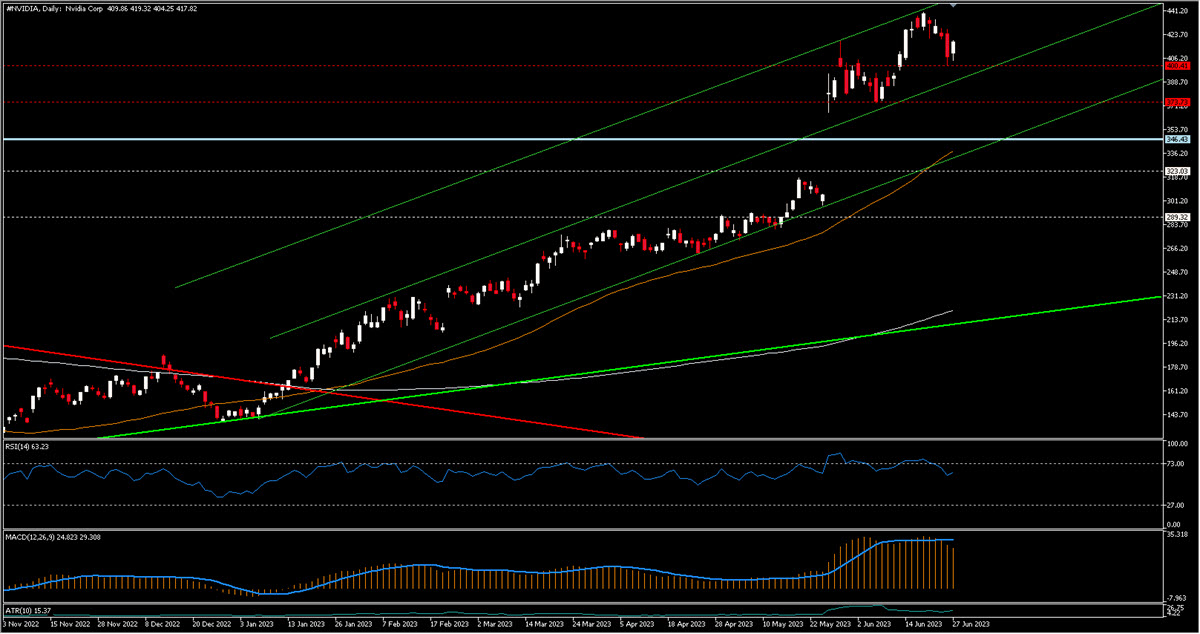

$345.95 was the previous ATH marked in November 2021 and was pulverised after the last company earnings releases. The movement is clearly exaggerated but can be framed within an rising channel, of which NVDA has tested the upper part twice recently (first at $419 and then at $439, a new ATH).

NVDA, Daily

The RSI is diverging downwards and the MACD histogram has also crossed downwards. What we expect is a return towards the MA 50 and the lower bound of the channel. First, there will be the important static supports at $400 and $373.73 ($366 interesting). If they are broken to the downside, the targets would be the previous ATH at $346 and then the GAP close ($305). As mentioned, MA50 and rising channel would work like obstacles (supports) in this type of movement.

Should momentum be stronger than any prudent consideration, the $440 area will come into play for both long and short traders.

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.