APAC stocks traded mixed as the disappointment from China’s decision on its Loan Prime Rates overshadowed its recent support efforts; Hong Kong underperformed. PBOC opted for a narrower-than-expected cut to the 1-year LPR alongside a surprise hold on the 5-year LPR, which is the reference rate for mortgages. PBOC and regulators met with bank executives and told lenders to boost loans to support the economic recovery instead. Meanwhile Country Garden has been delisted from the Hang Seng as the real estate sector in China crumbles before our eyes.

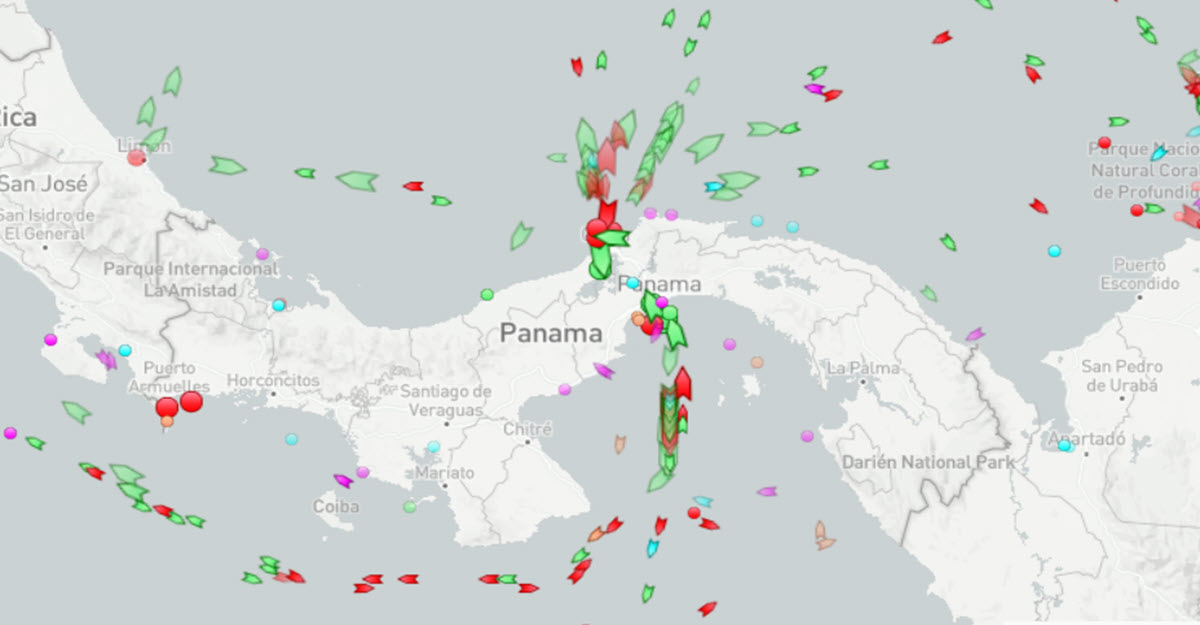

US500 futures were little changed on Sunday night after another losing week for the major averages: US100 closed the week lower about 2.6%, down for a third straight week for the first time since December. Meanwhile, the Dow closed the week lower by 2.2%, its worst streak since March. And the S&P 500 dropped 2.1% and posted its third consecutive losing week, which hadn’t happened since February. German PPI are just out, showing another consistent decline, but Unions at Woodside Energy’s North West Shelf offshore gas platforms on Sunday announced plans to strike as early as September 2nd, sending EU Natural Gas +18% this morning. On the inflation side we also have Japan, which is set to increase minimum pay by a record amount as inflation takes hold and 200 cargo ships are stuck waiting to cross the Panama Canal Water as shortages caused by the worst drought in 100 years have forced the canal operators to reduce the flow of traffic, which could have consequences for the global supply chain also as a result of what appears to be a still strong American consumer market.

Panama channel congestion real time

- FX – USDIndex is steady above 103 (103.32 now) and well above its 50-200 MAs; USDJPY found support above 145 (145.45 now), USDCNH heading north (7.33). NZDUSD keeps drifting lower (as does AUDUSD) after the Trade Balance data. Cable flat and lateral (1.2690 – 1.2765).

- Stocks – US and EU Futures are flat, Hong Kong slides again (-1.60% at 17631) despite Country Garden delisting.

- Commodities – USOil keeps recovering some ground, currently +0.61% at $81.88, the same for Copper steady at $371.20 after rebounding from the trendline last week.

- Gold – flat at $1,889 as is Silver ($22.75).

Today: No more relevant data after PBOC rate decision and German PPI earlier this morning.

Interesting Mover: VIX (-0.27%) @ 18.45, is pulling back after having tested its 200MA on Friday (Opex day); It’s finally back above the area that has been support after 2020 and should consolidate here. A move to the upside would have the 20.50-22 area as the next target.

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.