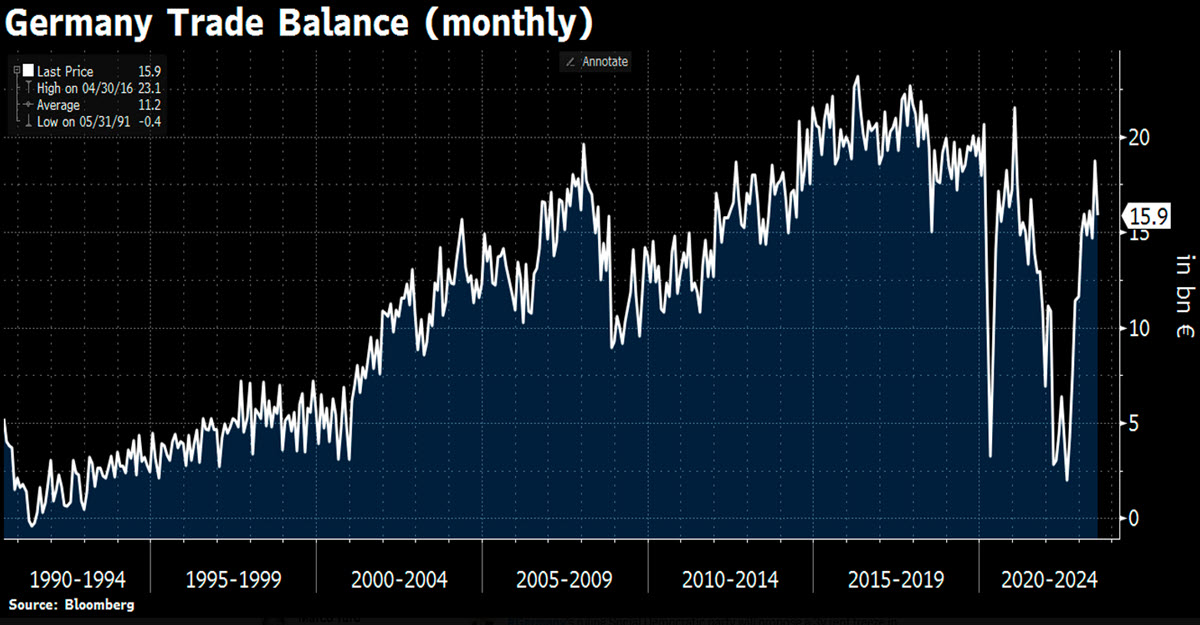

Yesterday was a rather calm day, lacking the US drive, and as the hours passed it partially soured. The European indices all finished slightly in the red, however no more than -0.24% on the FRA40, while the only significant figure from the Eurozone – apart from the Sentix Investor Confidence still nosediving – was the German trade balance’s -15% m/m decline led by the fall in exports, which was however smaller than expected; exports to China are down -16.5% YTD (Eur 57.7 billion). On her part, Lagarde cleverly avoided answering questions about future monetary policy in her speech in London.

A short while ago, the RBA left its cash rate unchanged at 4.1% as expected, the third consecutive month of pause, weighing on AUD’s performance, but it is all the Asian currencies that are weak. The Chinese Caixin Services PMI – while still in expansionary territory – posted its worst reading in nine months (51.8 down from 54.1) and this comes after some other if not certainly good, at least hopeful manufacturing statistics last week. However, the whole of APAC is in the red despite Country Garden managing to avoid its first default. US futures are also -0.1% on average at the moment. UBS expects clear signs of a US economic slowdown in November, bringing an end to the Fed’s tightening cycle.

- FX – USDIndex still strong at 104.19, AUDUSD underperforms (-0.66% at 0.6418), USDJPY faces 147 (146.82 now), USDCNH 7.29, EURUSD -0.11% at 1.0784, Cable -0.07% at 1.2619.

- Stocks – China 50 -0.56, AUS200 -0.25%, GER40 set to open -0.22% at 15789; US Futures: US500 -0.07%, US100 -0.03%, US30-0.10%.

- Commodities – USOil at a 10 month high @ $85.87, UKOil @ $88.88. Copper continues correcting, -0.67% at $382.40.

- Gold – below $1940, at $1937.25. Silver – 0.65% at $23.82.

LATER TODAY: HCOB PMIs Services & Composite in DE, FR, IT, SP, EU, European PPI, US Redbook and Factory orders, Lagarde speech.

INTERESTING MOVER: BTCUSD -0.79% in the last 24h at 25726 keeps hovering around the crucial 25250 area that happens to be also the 200d MA; it has recently lost its 2023 ascending channel and retested from the downside last week, being brutally rejected.

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.