After September PMI data showed a stall in overall activity for the second consecutive month, the USDIndex lost some of its gains after reaching 105.43 in Friday’s trading [22/09]. The USDIndex gained +0.19% on carryover support from Wednesday, when the FOMC signalled one more +25 bp rate hike this year and projected that next year’s rate will be +50 bp higher than June’s rate.

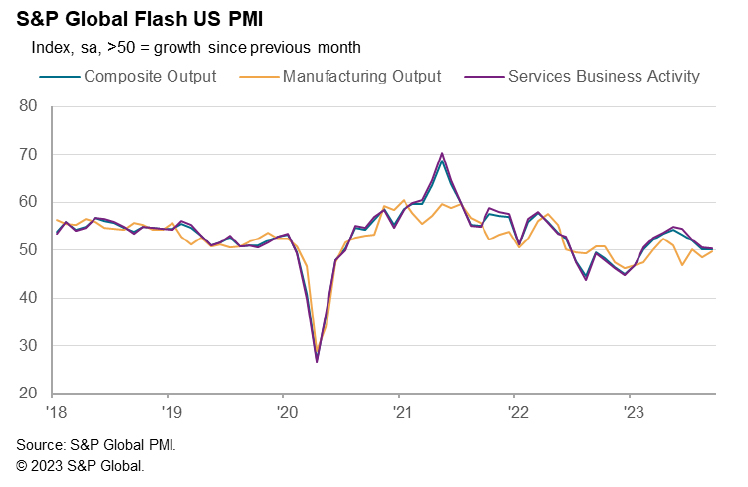

US Manufacturing PMI rose from 47.9 to 48.9 in September. Services PMI fell from 50.5 to 50.2, the lowest in 8 months. The Composite PMI fell from 50.2 to 50.1, the lowest in 7 months.

Due to the prospect of higher and longer interest rates and continued inflationary pressures, service sector growth slowed to its worst level in eight months and manufacturing output continued to decline. Indications from the Federal Reserve, that an interest rate hike may still be possible, kept the USDIndex on a strengthening path for ten consecutive weeks.

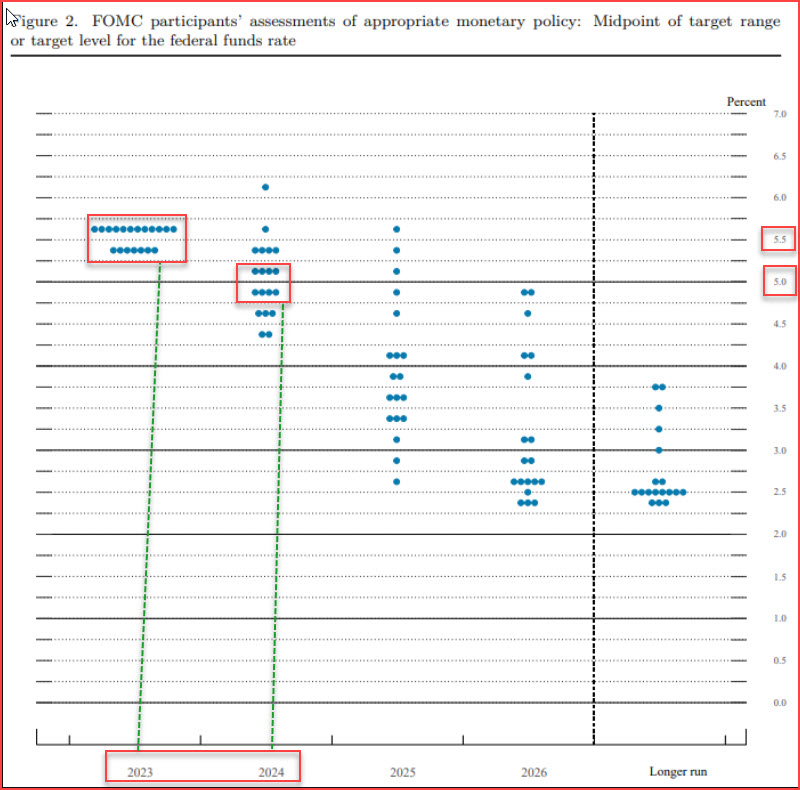

The Fed kept the funds rate target range at 5.25%-5.5%, but dot-plot predictions suggest that there is a possibility of one more hike this year. Friday’s hawkish comments from several policymakers gave the Dollar a boost.

- San Francisco Fed President Daly: not ready to declare victory in the fight against inflation and said it is unlikely that inflation will reach the Fed’s target of 2% by 2024.

- Fed Governor Bowman: predicted that further rate hikes may be needed to return inflation to 2% in a timely manner.

- Boston Fed President Collins: interest rates may have to remain higher, and for longer, than previously projected and further tightening is not yet possible.

All attention will be focused on the US personal expenditure and income reports, with particular anticipation surrounding the release of the PCE price index. It is forecast that core PCE prices will increase by 0.2% in August, similar to the pace in July; whilst the annualised inflation rate, considered the Federal Reserve’s preferred measure of inflation, is expected to fall to 3.8%, marking the lowest point since June 2021. The report is also poised to reveal a 0.5% increase in consumer spending and a 0.4% rise in the same period. In addition, investors will closely monitor durable goods orders in August, as well as the final readings of second quarter GDP growth and Michigan consumer sentiment in September. Related Article: /732190/

Markets will also be watching the UAW strike closely, and the possibility of a government shutdown looms large. It will also be a busy week filled with central bank talks.

Technical Review

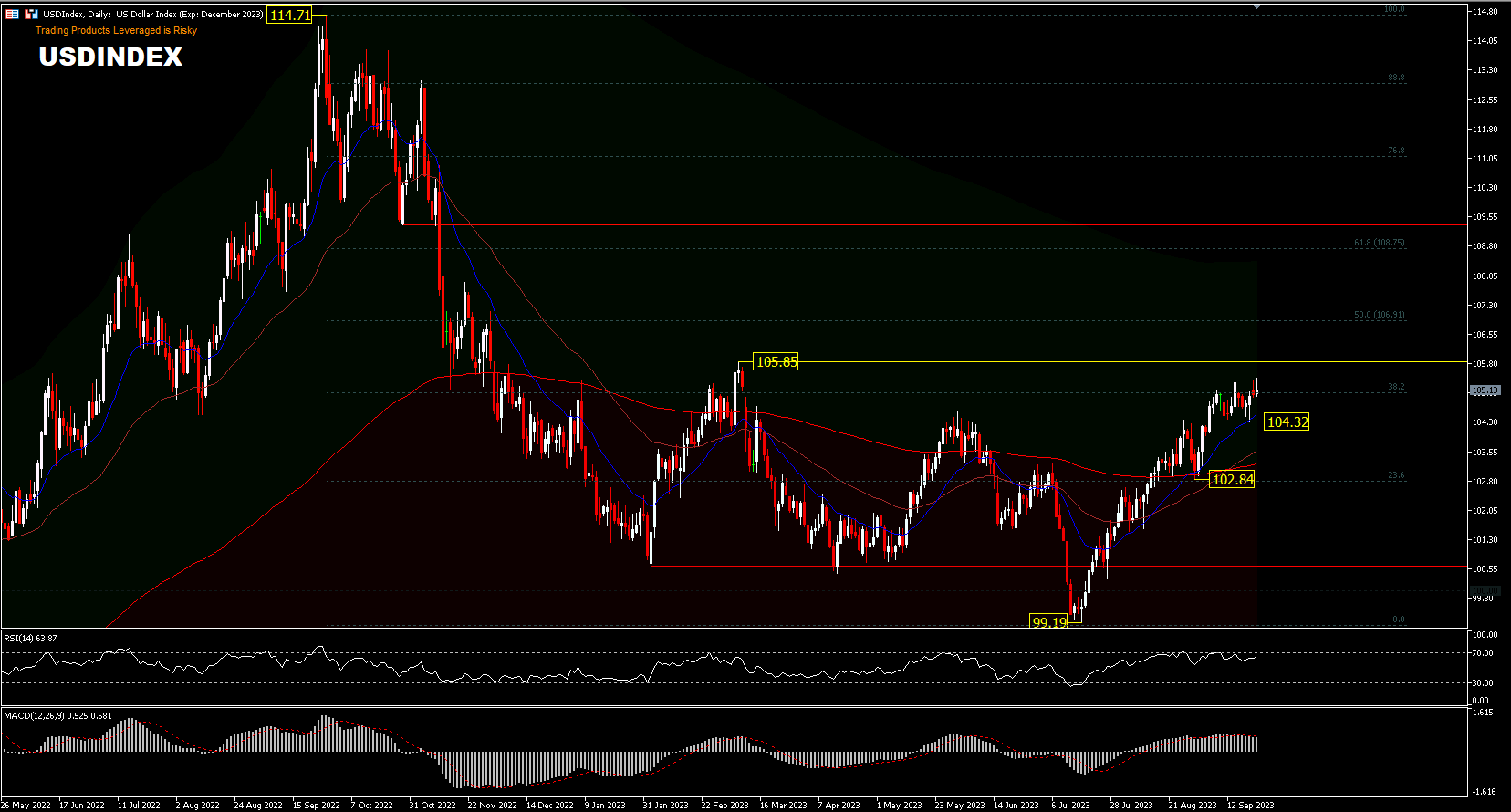

USDIndex, D1 reached a 10-week peak of 105.43 last week with the high price of the year recorded at 105.85 in March serving as resistance. Last week’s index price closed at 105.13 [38.2%FR] with the appearance of 2 different coloured daily shooting star candles. Given that the price is still trading above the 20-day exponential moving average, the potential to equate higher is still open.

A move above 105.85 will confirm the resumption of the uptrend with a possible test of the 50%FR level (+/- 107.00). However, as long as 105.85 holds, then a move to the downside would provide 2 supports to test, at 104.32 and 102.84 respectively. Some recent price-gap gaps at interim highs may be signalling something.

With the Federal Reserve’s hawkish stance, a potential US government shutdown and international central bank activity, investors should remain vigilant. The US Dollar is likely to remain strong, but global uncertainties may affect market dynamics. Given current economic indicators, the short-term market outlook is likely to be bullish for the US Dollar.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.