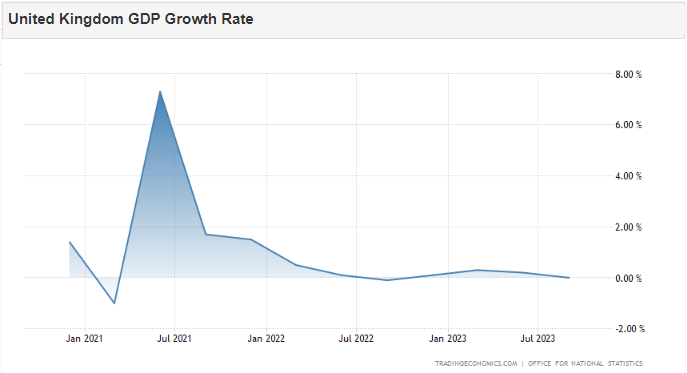

Sterling remained relatively stable, trading above the $1.22 level last week, as UK economic growth levelled off in Q3 2023, surpassing expectations of a contraction and potentially averting a recession this year. Q3 GDP was unchanged at 0% q/q, better than the -0.1% forecast, resulting in growth of 0.6% y/y in Q3, higher than the 0.5% figure expected by the market. According to the ONS, growth in September was 0.2% m/m, higher than the projected flat result.

Sterling did not receive much support and is likely to remain under pressure in the coming days, as markets continue to strengthen their expectations of a BOE rate hike in 2024. The BOE recently kept interest rates at their highest level in 15 years, reaffirming its commitment to tackling inflation. UK Finance Minister Jeremy Hunt emphasised sticking to the economic plan to combat inflation for sustainable growth.

UK inflation data will be released on Wednesday [15/11]. The headline CPI rate is expected to fall to 4.9% y/y from 6.7%, and the core rate to fall to 5.6% y/y from 6.1%. Nonetheless, according to the PMI, prices charged by companies increased to the highest level in three months in October. The employment report for September on Tuesday [14/11] could also be important, as average weekly earnings could provide a glimpse into the direction of inflation in the coming months. In addition, at the end of the week, data from retail sales m/m will be released.

CPI data showing higher-than-expected inflation could increase the percentage of rate hikes, and even if it doesn’t happen, it could still encourage investors to reduce the few basis points of rate cuts anticipated for next year; not because of a brighter economic outlook but because of concerns that massive cuts to support the economy could result in inflation getting out of control, which in turn could lead to more severe economic losses later on. Nonetheless, if there are no huge upside surprises in the services and wage figures, then the Bank will feel comfortable keeping rates unchanged in December.

Sterling’s decline, following this better-than-expected GDP figure, suggests that markets want to see a significant upside surprise in the data before bidding.

Sterling has been under pressure since August, as markets cut expectations for UK interest rates, reducing the likelihood of further hikes from the current 5.2% and rapidly increasing bets of a rate cut in 2024. Messages coming from the Bank of England suggest, however, that the recent tightening cycle is indeed over, in part because policy makers have now kept interest rates on hold for two consecutive meetings.

Technical Review

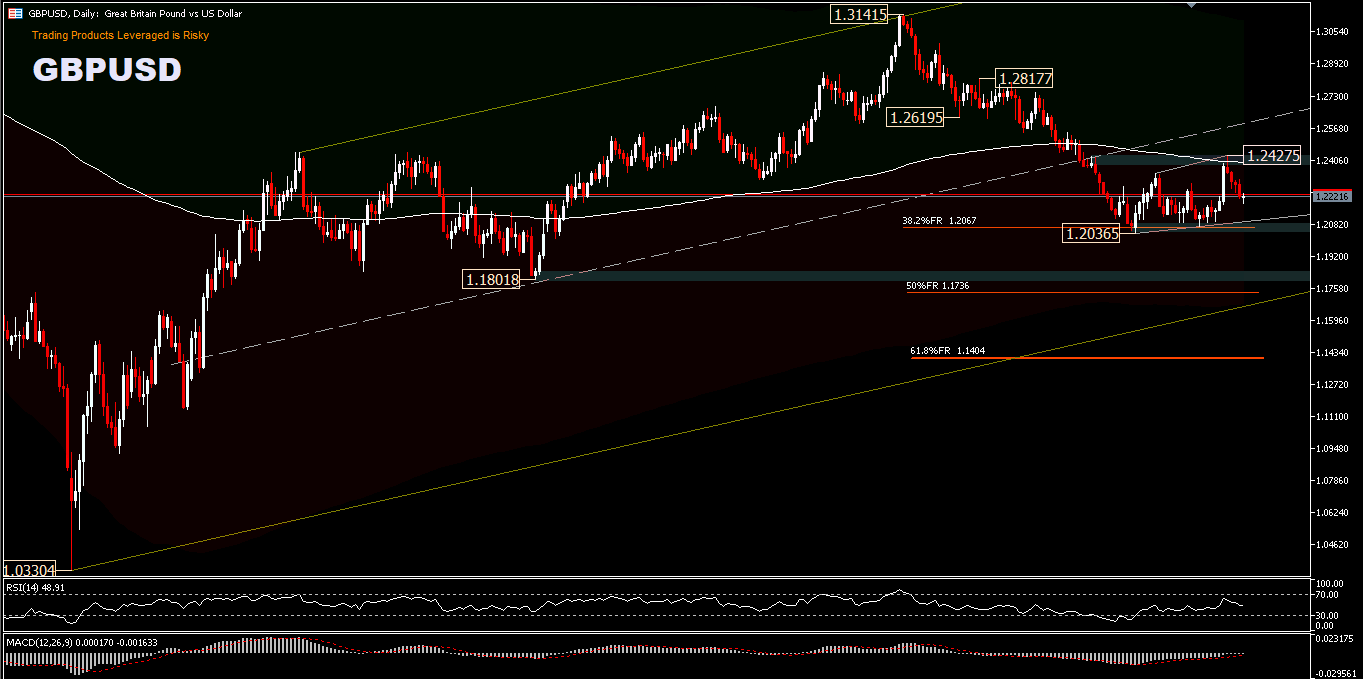

GBPUSD in the big picture: The price movement from the medium-term peak of 1.3141 is seen as a correction to the uptrend from the 2022 low [1.0330]. A strong rebound from the 38.2%FR retracement of 1.2067 [from 1.0330-1.3141 pullback] would suggest that it’s just a sideways pattern below the 200-day EMA. However, a sustained break of 1.2036 would suggest that a deeper correction could test the 50%FR and 61.8%FR levels at 1.1736 and 1.1404, respectively.

Intraday bias [H8] is still on the downside at the moment. The corrective rebound from 1.2036 could have finished at 1.2427 just below the 38.2%FR pullback level of 1.3141-1.2036. A deeper drop would be seen back to retest the 1.2036 support zone first. However, on the upside, a break of the minor resistance at 1.2307 will reduce the bearish probability and turn the intraday bias to neutral first. Currently, the price remains below the 200 EMA, the RSI is trending negative and the MACD is approaching the centre line with its the slope flattening.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.